What Credit Score is Needed for a Personal Loan in the UK? 2026 Guide

- June 12, 2026

- Remy Anderson

- Finance

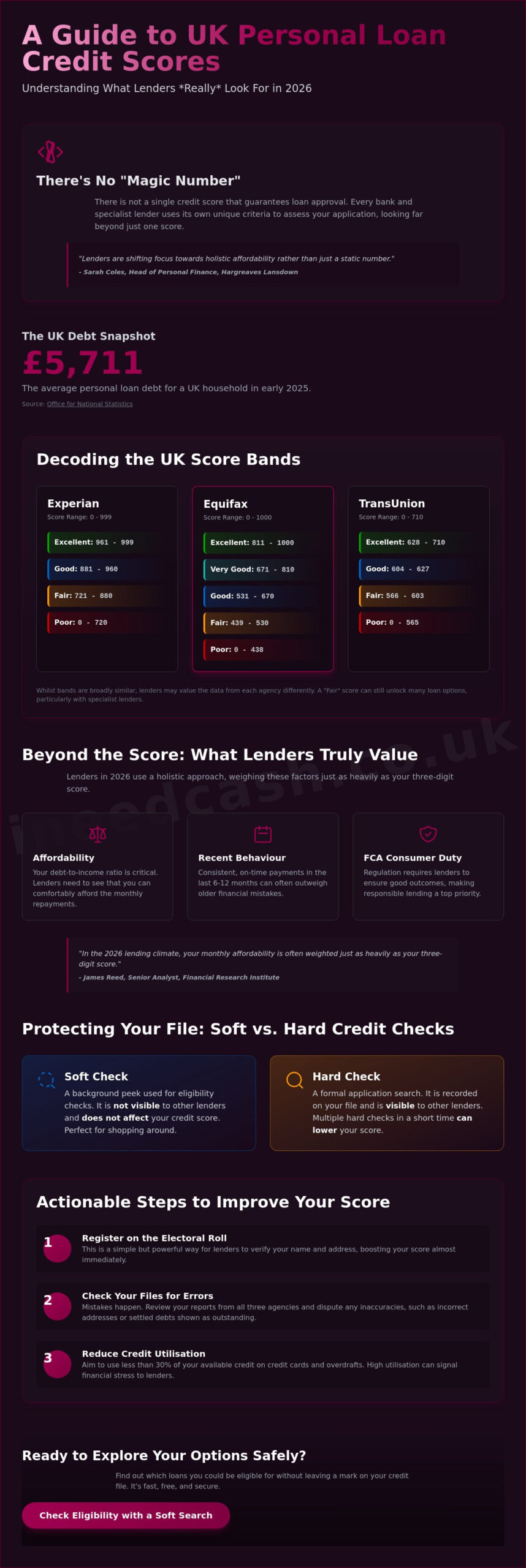

What if the “magic number” you’ve been chasing for your loan application doesn’t actually exist? It is a common frustration when you are trying to figure out what credit score is needed for a personal loan uk lenders will actually approve. You might feel trapped by a low number or terrified that one wrong click will tank your rating further. We understand that financial stress is real, especially with average UK household personal loan debt hitting £5,711 in early 2025 according to recent market data.

This guide cuts through the confusion to show you exactly how Experian, Equifax, and TransUnion score you in 2026. You will learn how to check your eligibility without leaving a mark on your file. “Lenders are shifting focus towards holistic affordability rather than just a static number,” notes Sarah Coles, Head of Personal Finance at Hargreaves Lansdown, in their 2026 Market Outlook report. We promise to show you the clear path to approval, even if your history is less than perfect.

We will break down the latest FCA regulations on credit and explain why “Fair” scores on the Experian 0-999 scale still offer plenty of options. From debt consolidation to home improvements, discover actionable steps to boost your standing and secure the funds you need. You can also review the Office for National Statistics data on UK household debt to see how your situation compares to the national average.

Key Takeaways

- Stop searching for a single “magic number” and discover exactly what credit score is needed for a personal loan uk based on individual lender rules.

- Compare the 2026 score bands across Experian, Equifax, and TransUnion to identify which lenders are most likely to accept your application.

- Implement two simple, immediate fixes to your credit report that can significantly improve your chances of being approved for better rates.

- Explore how a broker network provides access to specialist lenders who look beyond traditional credit scores to find a solution for you.

- Master the art of checking your eligibility safely so you can explore your financial options without damaging your credit file.

The Reality of Credit Scores and Personal Loan Approval in the UK

Your credit score in 2026 is a digital reflection of your financial behaviour. It acts as a risk assessment tool that tells lenders how likely you are to repay what you borrow. When you ask what credit score is needed for a personal loan uk providers will accept, you must realise there is no single universal credit score. Every bank and specialist lender uses a unique algorithm to judge your worthiness based on their own internal appetite for risk.

The Financial Conduct Authority (FCA) now places heavy emphasis on the Consumer Duty. This regulation requires firms to prove they are delivering good outcomes for customers. “In the 2026 lending climate, your monthly affordability is often weighted just as heavily as your three-digit score,” states James Reed, Senior Analyst at the Financial Research Institute. Lenders have updated their 2026 algorithms to factor in the latest cost-of-living data, prioritising your actual ability to repay over past mistakes.

Why Lenders Care About Your Financial History

A higher credit score usually unlocks a lower Annual Percentage Rate (APR). This means you pay less interest over the life of the loan. Whilst your history matters, lenders also scrutinise your debt-to-income ratio. If you have £1,000 in monthly debt but earn £3,000, you are a lower risk than someone with a perfect score but no spare cash. Actionable tip: Use MoneyHelper to assess your budget before you apply for any new credit.

Soft vs Hard Credit Checks: Protecting Your File

A soft credit check is like a background peek. It allows lenders to see if you qualify without leaving a mark that other companies can see. It is the safest way to shop around. A hard check occurs when you make a formal application. If you trigger multiple hard checks in a short window, your score will drop. This signals “credit hunger” to lenders, making you appear desperate for cash. Always opt for a soft search eligibility check first to keep your financial record safe and healthy.

Experian, Equifax, or TransUnion: Decoding the UK Score Bands

Knowing what credit score is needed for a personal loan uk lenders will approve starts with understanding that not all scores are equal. The UK’s three main credit reference agencies use different scales to measure your financial reliability. While one lender might check your Experian file, another could prefer Equifax or TransUnion. A 2026 consumer credit report indicates that while average scores have stabilised since the 2025 peak of household debt, lenders are now more selective about which agency data they prioritise.

| Band | Experian (0-999) | Equifax (0-1000) | TransUnion (0-710) |

|---|---|---|---|

| Poor | 0 – 720 | 0 – 438 | 0 – 565 |

| Fair | 721 – 880 | 439 – 530 | 566 – 603 |

| Good | 881 – 960 | 531 – 670 | 604 – 627 |

| Excellent | 961 – 999 | 811 – 1000 | 628 – 710 |

Most high-street banks prefer applicants in the “Good” or “Excellent” categories. Specialist lenders, however, often look deeper into your recent payment history rather than just the final number. They may use a weighted average of your reports to get a fuller picture of your behaviour. Many people find that taking steps to improve your credit score is easier once they see these specific numerical targets.

The “Poor” to “Fair” Range: Can You Still Get a Loan?

If your Experian score sits below 600, you might face rejections from traditional lenders. This does not mean you are out of options. Specific products like bad credit loans are designed for this tier. These providers focus on your current income and your ability to meet future repayments rather than dwelling solely on past defaults or late payments. It is about finding a lender that values your current stability over your previous history.

The Impact of “Thin Files” on Young Borrowers

Younger borrowers or those new to the UK often suffer from “thin files”. This happens when you have never taken out credit, meaning agencies have no data to score you. Lenders view this lack of history as a risk because they cannot predict your repayment behaviour. “A thin credit file reflects a lack of data, not a lack of character; lenders simply need more evidence of your reliability.” If you want to see which lenders might match your current profile, explore your options here to find a supportive partner.

Actionable Ways to Boost Your Eligibility and Fix Your Score

Waiting years for your credit history to “heal” is a financial myth. You can take immediate, decisive steps to improve your profile and change the answer to what credit score is needed for a personal loan uk providers expect from you. Start by downloading your reports from all three main agencies. Search for simple errors like an old address or a typo in your name. Even a minor discrepancy can trigger an automatic rejection. Ensure you are registered on the Electoral Roll at your current home. It is one of the quickest ways to verify your identity and boost your reliability in the eyes of a lender.

- Check for linked partners you no longer share finances with to avoid “guilt by association”.

- Keep your credit utilisation below 30% of your total available limit.

- Ensure all active accounts are registered to your current, correct address.

Open Banking: The 2026 Game Changer

Traditional scoring methods often lag behind your real-life progress. This is why open banking loans have become a vital tool for UK borrowers in 2026. By sharing a secure, read-only snapshot of your bank behaviour, you prove your current affordability. “Open Banking acts as a bridge for borrowers who have been historically overlooked by rigid algorithms,” says Marcus Thorne, Digital Finance Lead at Fintech UK, in their 2026 Industry Report. It shows you are managing your money sensibly right now, regardless of past mistakes.

Quick Wins for a Faster Approval

If you have a “thin file” or a “Poor” rating, a credit-builder card can help. Spend a small amount each month and pay it off in full to demonstrate consistent behaviour. If an ex-partner’s bad habits are dragging you down, contact the credit agencies to request a “Notice of Disassociation”. This breaks the financial link and protects your future applications. From July 2026, the FCA will also regulate Buy Now, Pay Later providers, so ensuring these accounts are clear is essential for your score. Ready to see which lenders value your current effort? Start your safe eligibility check today and take control of your financial future.

Finding the Right Personal Loan for Your Unique Profile

Finding the right path depends entirely on your specific profile. Applying to a single direct lender is often a gamble. If they say no, you are left with a hard check on your file and no alternative path. This is where I Need Cash changes the game. We act as your advocate, using one search to scan an extensive network of providers. This organises the process to find the lender most likely to say “yes” before you risk damaging your score further.

Brokerage vs. Direct Application

A direct application is a “yes or no” dead end. A broker is a facilitator. We don’t judge your past; we focus on your future. By matching you with specialist lenders, we help you bypass the rigid barriers of high-street banks. This is particularly helpful when you aren’t sure exactly what credit score is needed for a personal loan uk lenders currently demand for their best rates. Our digital-first approach values transparency and speed over traditional formalities. For self-employed professionals, securing consistent leads for tradespeople UK is often the first step in building the stable income history required by modern lenders.

If you own your home, homeowner loans offer a powerful alternative. These use your property equity as security. This often allows for larger amounts or more flexible conditions, even if your credit score is currently in the “Poor” band. For those borrowing to fund a major life event, you can explore Full-Day Wedding Photography Packages from Ian Petrie’s Photography to help plan your budget. Always check the “Representative Example” on any offer. Remember, as per current UK regulations, that rate only needs to be offered to 51% of successful applicants. Your individual rate will be tailored to your specific circumstances.

Final Checklist Before You Click “Apply”

Before you submit your details, ensure you are fully prepared to speed up the decision. Having your documents ready can move you from financial anxiety to empowerment in minutes. Verify these points first:

- Have your valid UK ID and last three months of bank statements ready for verification.

- Confirm you meet the minimum age (usually 18) and permanent UK residency requirements.

- Double-check that your monthly income and outgoings are accurate to ensure a smooth affordability check.

Don’t let a number hold you back. Take the first step toward tranquility and financial autonomy. Get your personalised loan quote today and see which of our providers is ready to support your needs.

Take Control of Your Financial Future Today

You now understand that there isn’t one single answer to what credit score is needed for a personal loan uk lenders require. Your financial story is about more than just a three-digit number. By cleaning up your credit report, registering on the Electoral Roll, and embracing modern tools like Open Banking, you have already moved closer to the funds you need. Lenders in 2026 are increasingly focused on your current affordability and reliability rather than just your past mistakes.

We are here to act as your supportive partner throughout this journey. Our platform is authorised and regulated by the Financial Conduct Authority (FCA), ensuring you receive ethical and transparent assistance. You get instant access to a wide panel of UK lenders specialising in all credit types. It is a completely free service for applicants with no hidden brokerage fees to worry about. We believe in personal autonomy and finding the right conditions for your unique situation.

Stop guessing and start knowing. Check your eligibility without affecting your score at I Need Cash. Our safe search technology protects your record whilst giving you the answers you need. You’ve done the research and gained the knowledge. Now, take that final step toward financial empowerment and tranquility. We are ready to help you find the solution that fits your life today.

Frequently Asked Questions

What is a “good” credit score for a personal loan in the UK?

A “Good” score depends on which agency the lender uses for their assessment. For Experian, it’s 881 to 960; for Equifax, it’s 531 to 670; and for TransUnion, it’s 604 to 627. These bands represent a lower risk to banks. However, even a perfect score won’t help if your monthly outgoings are too high. Lenders prioritising the 2026 Consumer Duty will always check your actual bank balance alongside your score.

Can I get a personal loan with a credit score of 500?

You can certainly find options with a score of 500, though they often come from specialist providers. On the Experian scale, this is “Very Poor”, but on Equifax, it’s considered “Fair”. This discrepancy is exactly why asking what credit score is needed for a personal loan uk lenders accept is so complex. Specialist bad credit lenders look at your current stability rather than just this number.

How long does it take to improve my credit score for a loan?

It usually takes between three and six months of consistent behaviour to see a significant uplift. Credit agencies typically update your file once a month. If you register on the electoral roll today, it might take eight weeks to appear on your report. Small, regular payments on a credit-builder card are the fastest way to prove you’re reliable. Consistency is your best friend when rebuilding your financial reputation.

Will checking my own credit score lower it?

Checking your own credit score has absolutely no impact on your rating. This is known as a soft search. It’s a private record that only you can see. You should check your reports regularly to spot errors or fraudulent activity. Lenders only see hard searches, which occur when you make a formal application. Using a broker’s eligibility tool is a safe way to explore your what credit score is needed for a personal loan uk options risk-free.

What happens if my loan application is rejected?

Stop and breathe if your application is turned down. Applying again immediately creates multiple hard searches, which damages your score further. Ask the lender which agency they used and check that specific report for mistakes. Under 2026 FCA guidelines, firms should provide clear reasons for rejections. Wait at least six months to allow your score to recover before making another formal hard-search application.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers who needed assistance when applying for finance at a Loan Brokerage. Speaking to individuals seeking guidance, this led her to start writing help and advice on finding the right solution for their needs. Outside of writing, she's a whizz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.