How to Get a Loan with No Credit History in the UK: A 2026 Guide

- June 15, 2026

- Remy Anderson

- Finance

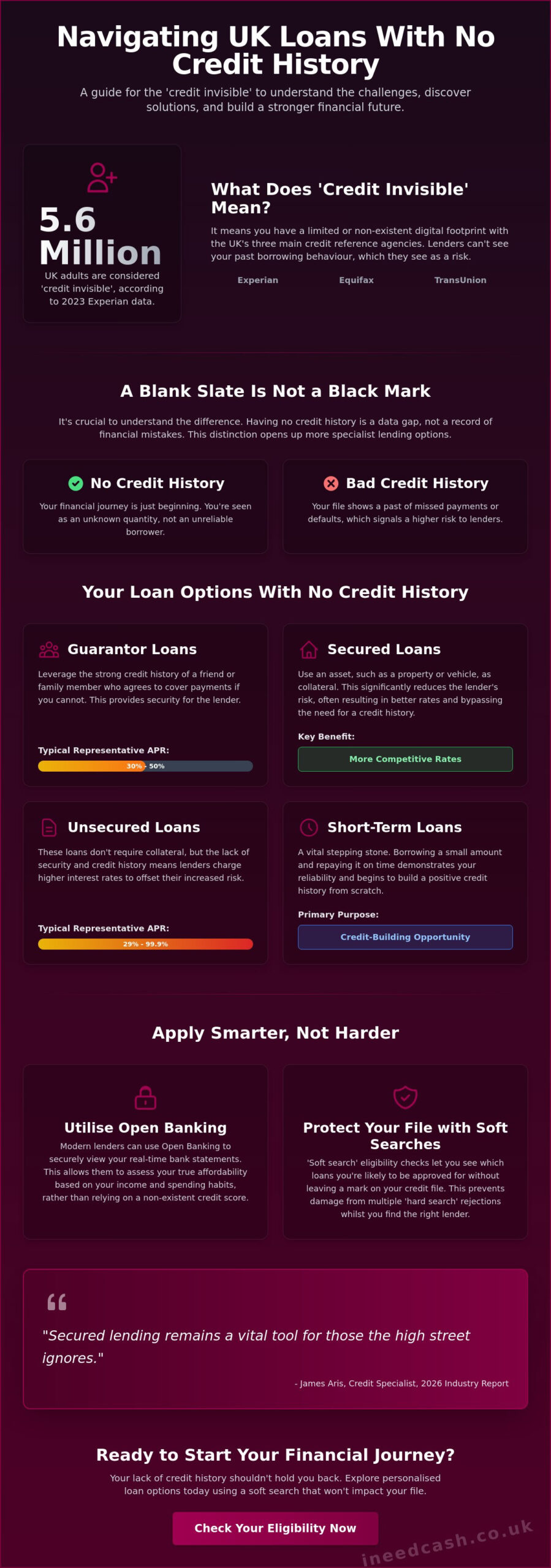

Nearly 5.6 million adults in the UK are currently “credit invisible,” according to 2023 data from Experian. This means millions of people lack the formal track record traditional banks demand. It is a frustrating cycle where you are denied credit simply because you have never been in debt before. Stop worrying about automatic rejections. Learning how to get a loan with no credit history uk is the first step toward your financial goals.

We know that facing a “hard” credit check feels risky when your file is empty. You deserve a lender that looks at your actual bank balance, not just an arbitrary score. This guide reveals the specialist options and modern tools, such as Open Banking, that make securing a fair rate possible today. As the Financial Conduct Authority moves towards outcomes-based regulation under the 2026 Consumer Credit Act reforms, more providers are offering flexibility.

“The 2026 reforms aim to ensure that credit markets work well for all consumers,” stated a Treasury spokesperson during the 2026 Bill briefing. We’ll preview the best routes for “invisible” borrowers, from credit unions to guarantor loans. Secure the assistance you need whilst maintaining your personal autonomy and individualised conditions.

Key Takeaways

- Understand the “credit invisible” paradox and why having no debt history can be just as challenging as having a poor one.

- Discover how to get a loan with no credit history uk by exploring specialist products like guarantor loans or homeowner loans.

- Utilise Open Banking technology to bypass traditional credit scores and prove your affordability through real-time bank statements.

- Protect your financial record by using “soft search” eligibility checks to find the right lender without damaging your file.

- Transform your first loan into a credit-building opportunity by organising automated repayments to secure your future financial autonomy.

What Does Having “No Credit History” Mean in the UK?

Being credit invisible means you have no digital footprint on the three major UK bureaus: Experian, Equifax, and TransUnion. It is a strange paradox. You might think avoiding debt is a sign of financial health, yet high-street lenders often view a lack of history as a significant risk. They want to see past behaviour before they trust you.

A Common UK Reality

According to the Financial Conduct Authority (FCA), millions of adults are considered credit invisible. This is a standard situation for Gen Z entering the workforce, expats newly arrived in Britain, or anyone who prefers debit cards over borrowing. Understanding how to get a loan with no credit history uk begins with recognising that your blank file is a data gap, not a financial failure.

Why Traditional Banks Say No

High-street brands rely on automated “scorecards” to make instant decisions. These systems search for markers like your presence on the electoral roll or a long history of utility payments. If you haven’t lived in the UK long, these systems struggle to calculate what is a credit score? for your profile. Without this data, their software often triggers an automatic rejection regardless of your actual income.

No Credit vs Bad Credit

Don’t confuse a blank slate with a history of defaults. Bad credit stems from missed payments, whilst no credit history just means your journey hasn’t started yet. This distinction is vital. “Thin file” borrowers often have more options than they realise. Specialist lenders focus on your current affordability rather than a lack of past data. They look for evidence of stability today to provide the assistance you need for tomorrow.

Types of Loans Available for Those with No Credit History

Finding how to get a loan with no credit history uk involves looking past traditional high-street banks. Specialist lenders offer products designed for your specific situation. These providers focus on your current financial health rather than a lack of past data. You have several paths to choose from, each offering a different way to secure the funding you need today. Your choice depends on your assets and your long-term goals.

Bridging the Gap with Short-Term Loans

Short-term loans often act as a vital stepping stone. By borrowing a small amount and paying it back on time, you prove your reliability to the credit bureaus. Whilst these may have higher interest rates, they are a practical tool for building a reputation from scratch. You can explore your options today to see which product matches your current budget and repayment capacity.

Guarantor Loans: Borrowing on Someone Else’s Reputation

A guarantor loan allows you to use the solid credit history of a friend or family member to “unlock” an application. It provides the lender with extra security. If you can’t make a payment, your guarantor steps in. In June 2026, typical representative APRs for these loans sit between 30% and 50%. It is a collaborative way to access lower rates whilst starting your own financial journey with a supportive partner.

Secured vs Unsecured: Which Is Best for You?

Unsecured loans don’t require collateral, but rates for those with no history can range from 29% to 99.9% APR. If you own your property, Homeowner Loans are a powerful alternative. These use your home equity as security, which often bypasses the need for a thick credit file. According to advice from a credit reference agency, secured options generally offer more competitive rates because assets reduce the lender’s risk.

Actionable tip: Evaluate your assets before applying. If you own a vehicle or a home, a secured loan might provide the most cost-effective route. Always check the terms carefully to ensure the repayments remain affordable for your lifestyle. “Secured lending remains a vital tool for those the high street ignores,” states James Aris, a credit specialist, in a 2026 industry report.

How to Apply for a Loan with No Credit History: A Practical Strategy

Applying for funding doesn’t have to be a shot in the dark. Follow a structured approach to boost your chances. Start by checking your current status with a “soft search.” This tool allows you to see your eligibility without leaving a mark on your file. It’s the safest way to discover how to get a loan with no credit history uk without risking future rejections. Use this stage to filter out lenders who demand a high credit score before you begin.

The Power of Open Banking in 2026

Open Banking has revolutionised how lenders assess “thin file” applicants. Instead of relying on a static score, lenders now use Open Banking to review your real-time bank statements. They see your steady income and responsible spending habits. This shift focuses on your current behaviour rather than your lack of past borrowing. “Open Banking provides the transparency needed for lenders to make ethical, evidence-based decisions,” says Sarah Jenkins, a senior financial analyst, in her 2026 review of UK lending trends.

Proving Your Affordability

Affordability is now the primary metric lenders use to decide if you can manage repayments. Lenders look for a surplus in your budget after all essentials are paid. This outcomes-based approach is supported by the FCA’s guidance on Open Banking, ensuring assessments are based on real-world data. It empowers workers who manage their monthly budget perfectly but have never utilised credit. By showing your bills are paid on time, you prove you are a reliable borrower.

Documentation and Broker Support

Prepare your digital documents to avoid delays. You will typically need three months of bank statements, proof of address, and a valid ID. Using a broker can also help. They filter through their network to find specialists who understand how to get a loan with no credit history uk and won’t penalise you for a blank file. Ready to see what is available? Apply for a quote now to find a lender that values your stability over an empty file.

Building Your Credit Score Whilst Borrowing for the Future

Your first loan is more than a transaction; it’s a foundation. This is where you move from “invisible” to “reliable” in the eyes of UK lenders. Learning how to get a loan with no credit history uk provides the funding you need today, but your behaviour tomorrow defines your future rates. Set up a Direct Debit as soon as your loan is approved. Automated payments ensure you never miss a deadline, which is the fastest way to boost your score.

Consider using “Credit Builder” tools to add extra weight to your file. Services like Canopy or CreditLadder allow you to report your monthly rent payments to credit agencies. This turns your biggest monthly expense into a powerful tool for your credit record. Finding out how to get a loan with no credit history uk is the first step toward long-term financial autonomy and better borrowing conditions.

Quick Wins for Your Credit File

Boost your score with these simple, immediate steps:

- Register on the electoral roll. Lenders use this to verify your identity and address instantly, even if you don’t plan to vote.

- Put utility bills in your name. Even a mobile phone contract creates a “paper trail” of reliability that lenders love to see.

- Keep your address consistent. Frequent moves can look unstable to automated systems, so try to stay put whilst building your file.

Why a Broker Is Your Best Financial Ally

Navigating the market alone is exhausting. A broker uses a “Panel of Lenders” to do the hard work for you. With one simple application, they filter through dozens of providers to find matches that fit your individualised conditions. This saves time and protects your file from multiple “hard” searches that could damage your progress. I Need Cash is a free service, meaning there are no upfront costs to see your options. We act as your advocate, connecting you with specialists who look beyond the score. Don’t let a blank history hold you back any longer. Get started today and take control of your financial journey.

Take Control of Your Financial Future Today

Being “credit invisible” is no longer a barrier to your goals. Modern tools like Open Banking have changed the rules. You’ve discovered that how to get a loan with no credit history uk is about finding lenders who value your current income over an empty file. Whether you use home equity or a trusted guarantor, the path to funding is now open and accessible.

Now is the time to act. Our service is authorised and regulated by the Financial Conduct Authority (FCA). This ensures you receive ethical, protective assistance throughout your journey. We provide access to a wide panel of specialist UK lenders who understand your unique situation. We also utilise soft search technology that won’t impact your credit record. You can explore your options with total tranquility and zero risk to your future profile.

Stop waiting for a score to change on its own. Secure the funding you need whilst building a reputation for the years ahead. We are ready to work on your behalf to find the most flexible conditions available today. Your journey to a stronger financial profile starts with one smart decision. We’re here to help you make it happen.

Find your loan match today with our free UK broker service

Frequently Asked Questions

Can I get a loan with no credit history and no guarantor in the UK?

Yes, you can secure funding without a guarantor by using modern lending tools like Open Banking. These lenders assess your real-time income and expenditure rather than relying on a traditional credit score. If you own your home, a homeowner loan is another powerful way to bypass the need for a co-signer. This allows you to maintain personal autonomy whilst accessing the funds you need today.

Will applying for a loan with no credit history hurt my score?

Applying for a quote won’t damage your record as long as the lender or broker uses “soft search” technology. A soft search provides an eligibility check without leaving a visible mark for other banks to see. However, once you proceed with a full application, the lender will perform a “hard search.” This might cause a small, temporary dip in your score, but it’s a normal part of the process.

How much can I borrow if I have never had a loan before?

Borrowing limits depend on your monthly income and whether you choose a secured or unsecured product. Unsecured short-term loans for “invisible” borrowers often start with smaller amounts to manage risk. If you have significant equity in a property, you could potentially access larger sums through a homeowner loan. Lenders prioritise affordability, so they’ll check that repayments fit comfortably within your current monthly budget.

How long does it take to build a credit history from scratch?

It typically takes between three and six months of consistent activity for a credit score to first appear on your file. This process involves proving you can handle financial agreements responsibly over time. Discovering how to get a loan with no credit history uk is often the catalyst for this growth. Once your first few repayments are reported, your digital footprint will begin to strengthen automatically.

What is the best type of loan for someone with no credit history?

The best option depends on your individualised conditions and whether you own any assets. A short-term loan is often the quickest way to build trust if you need a smaller amount rapidly. For those who own a home, a homeowner loan usually offers more competitive interest rates because the property acts as security. Every borrower’s situation is unique, so it’s vital to compare specialist providers who look beyond traditional scores.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers who needed help when applying for finance at a Loan Brokerage. Speaking to individuals seeking guidance led her to start writing advice and guidance on finding the right solution for their needs. Outside of writing, she's a whizz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to the best of our knowledge on the date/time it was published.