Self-Employed Loans UK No Proof of Income: Your 2026 Guide

- June 10, 2026

- Remy Anderson

- Finance Self-employed

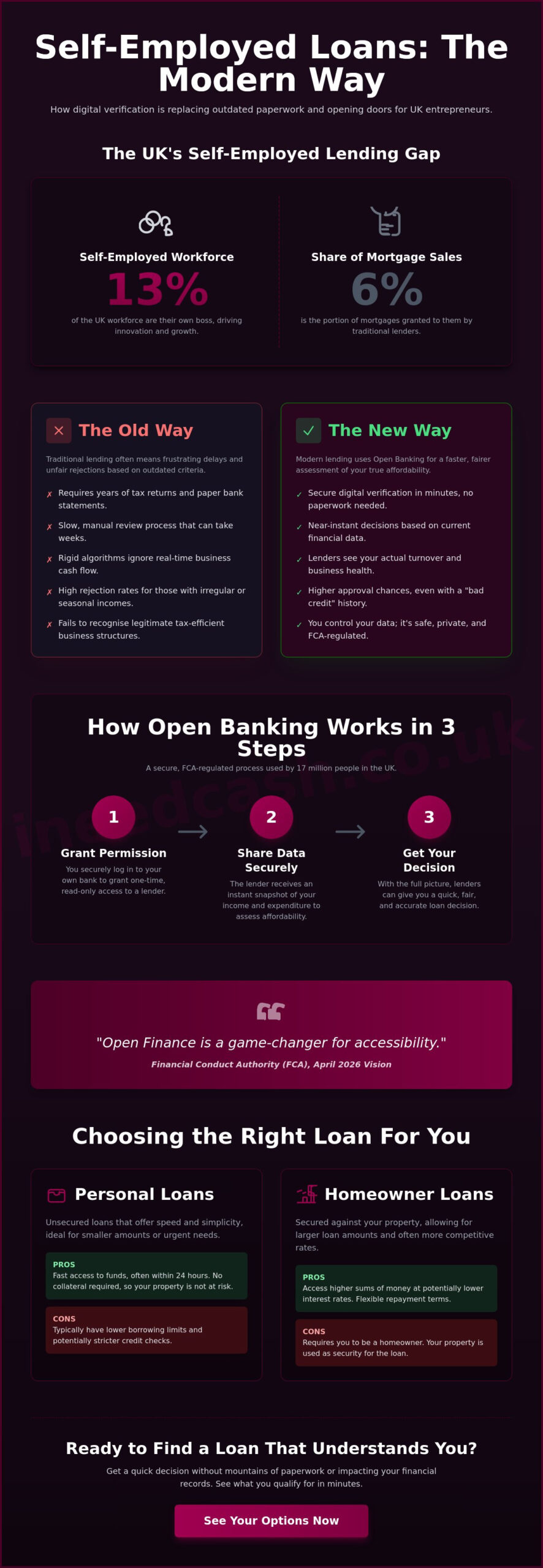

Did you know that 13% of the UK workforce is now self-employed? Yet traditional lenders still lag behind. Self-employed borrowers made up only 6% of mortgage sales in 2025. It’s a frustrating reality that leads to high rejection rates and endless paperwork.

If you’ve been searching for self employed loans uk with no proof of income, you may feel anxious. A "bad credit" label can make you feel judged. High-street banks shouldn’t judge you just because you don’t have a standard payslip.

In 2026, "no proof of income" doesn’t mean "no verification"; it means digital verification that respects your time. The FCA recently launched consultation CP26/18 to encourage lenders to use more discretion for those with irregular incomes.

With the Bank of England base rate at 3.75% as of June 2026, finding a supportive partner is vital. "Open Finance is a game-changer for accessibility," the FCA stated in their April 2026 vision.

By using Open Banking, with 17 million active UK users, you can share data securely. This helps us make a quick decision. It will not affect your financial records. This guide reveals how to secure a loan that recognises real-world cash flow and offers the flexibility you deserve.

Key Takeaways

- Understand why modern lending focuses on digital verification rather than traditional paper tax returns to respect your time and autonomy.

- See how Open Banking provides a risk-free way to share financial data, ensuring faster decisions and more accurate affordability checks for the self-employed.

- Discover how to access self employed loans uk no proof of income by using technology that recognises your real-world cash flow and business potential.

- Compare the speed of personal loans against the lower rates of homeowner loans to find the flexible terms that suit your irregular income.

- Learn the essential steps to organise your digital records and engage with expert brokers who specialise in navigating the modern lending landscape.

Table of Contents

What Are Self-Employed Loans with No Proof of Income?

Searching for self employed loans uk no proof of income doesn’t mean you’re trying to hide your earnings. It means you’re looking for a lender that understands the modern economy. Lenders design these loans for people who don’t have traditional paper tax returns or stacks of payslips.

Instead of manual paperwork, lenders use Open Banking to verify your income digitally and securely. It’s about speed, autonomy, and moving away from the printer.

The early 2000s “no-doc” loans no longer exist. Today’s alternatives are safer and more transparent. According to the ONS, about 13% of the UK workforce is self-employed, yet many still feel locked out of the financial system.

Whether you’re a sole trader, a contractor, or a seasonal worker, these modern products bridge the gap. They focus on your current bank balance and regular turnover rather than just your last three years of tax filings.

Why Traditional Banks Struggle with Self-Employment

High-street banks operate on rigid criteria. They favour PAYE employees because their income is predictable and easy to plug into an algorithm.

If you’re self-employed, your official income may look lower because of tax planning and valid business expenses. This often leads to a "computer says no" response. Traditional lenders often miss the strong business behind tax-efficient figures. This leaves many entrepreneurs feeling frustrated and rejected.

The Role of the FCA in Protecting Self-Employed Borrowers

Regulation is your safety net. The Financial Conduct Authority (FCA) authorises and regulates all reputable brokers and lenders. In June 2026, the FCA released consultation CP26/18. It encourages lenders to use more discretion for people with irregular incomes.

This move proves that the industry is shifting towards a more inclusive model. “No proof” does not mean unsafe. It means a smarter, tech-driven way to show you can afford repayments. It avoids the stress of manual paperwork.

How Open Banking Has Replaced Traditional Paperwork

Stop wasting time scanning old bank statements or waiting for the post. Open Banking is a secure, digital handshake between your bank and a lender.

It provides instant access to your financial data without you needing to print a single page. As of early 2026, about 17 million people in the UK are active users of this technology.

That is nearly 1 in 3 adults. It is the main way to access self employed loans UK with no proof of income. It shows your current affordability at once.

This technology is a lifeline if you have "bad credit" but a healthy business. Lenders no longer have to rely solely on a static credit score from years ago. Instead, they see your daily turnover and regular payments.

"Open Banking allows lenders to see the pulse of your business in real-time, rather than a snapshot from a year ago." This real-time view means faster decisions, fewer manual errors, and more accurate affordability checks. When Comparing Personal Loans for the Self-Employed, look for lenders who embrace this digital-first approach.

Is My Data Safe with Open Banking?

Privacy is often the biggest concern for sole traders. You might worry about who sees your spending habits.

With Open Banking, you retain absolute control. You control exactly what data you share and how long you share it. You can revoke access at any time through your banking app.

It uses a highly secure FCA-regulated framework to keep your financial records private and protected. For a deeper dive, learn more about open banking loans to see how the process works for you.

Ready to see what you qualify for? Start online in minutes and find a solution that fits your business needs. For entrepreneurs looking to invest in specific assets, you can check out V4B Business Finance to explore their tailored equipment finance options.

Comparing Homeowner and Personal Loans for the Self-Employed

Deciding which path to take depends on your assets and how quickly you need the cash. Personal loans are unsecured, meaning they don’t require collateral. They are excellent for speed, but lenders might be stricter on your credit score. If you’re looking for self employed loans uk with no proof of income, personal loans often have lower limits than secured loans.

The Broker Advantage for Self-Employed Borrowers

A broker is your best ally when you don’t fit the standard high-street mould. They have access to a network of independent lenders who specialise in non-traditional income.

This allows them to negotiate individualised conditions that respect your personal autonomy. At I Need Cash, our proprietary moral code ensures we act as your advocate rather than a gatekeeper. You can see how these compare to traditional requirements in Experian’s guide to self-employed loans.

Homeowner Loans: Using Your Equity as Proof

Think of your property equity as a silent partner that vouches for your financial stability. When you have equity, lenders feel more secure, which reduces the need for perfect, multi-year paper records.

This is a game-changer for contractors who have strong current cash flow but "messy" paperwork. With the Bank of England base rate at 3.75% in June 2026, these are often the cheapest way to borrow. Explore our homeowner loan options to see how your property can work for you. Beyond financing your business, if you require professional housing for your team, you can learn more about Homes For Workers to find specialised contractor accommodation.

Short-Term and Bad Credit Loan Options

Not every entrepreneur owns their own home. If you rent or need funds urgently for a business emergency, short-term or bad credit personal loans are viable paths.

These focus heavily on your recent Open Banking data to ensure you can afford the repayments today. They provide a quick solution whilst you grow your business. Get a quick cash loan quote to find a solution that fits your immediate needs.

Ready to secure a deal that works for your unique situation? Apply online now to find the right loan for your business.

Steps to Secure Your Loan Through a UK Broker

Ready to move forward? Securing self employed loans uk no proof of income is a straightforward process when you have the right partner. You don’t need to spend hours at a printer. Instead, follow these four simple steps to get the cash you need for your business or personal goals.

-

Step 1: Organise your digital records. Ensure your business banking is clear and up to date. Since lenders use the secure Open Banking technology we discussed earlier, having a tidy digital footprint makes the process much faster.

-

Step 2: Use a specialist broker. Don’t limit yourself to one bank. Use a broker to access a panel of independent lenders who understand the nuances of self-employment and irregular income.

-

Step 3: Check eligibility via a "soft search". This is your signature safety net. A soft search allows you to see which loans you qualify for without leaving any mark on your credit record or damaging your score.

-

Step 4: Review your personalised quote. Once you have your offers, choose the terms that fit your monthly budget and respect your personal autonomy.

Why Use a Broker Instead of a Direct Lender?

I Need Cash acts as your advocate, not a gatekeeper. Direct lenders only have one set of criteria; if you don’t fit, they simply say no.

We work on your behalf to find the most flexible lenders in the UK. We take a non-judgmental approach to your financial history. Whether you made mistakes in the past or have bad credit now, we find a supportive solution.

Preparing for Your Application: Actionable Tips

Preparing for Your Application: Actionable Tips

Check your credit report before you apply. Use services like Equifax or Experian to ensure your data is accurate.

Another vital tip: keep your personal and business expenses separate. This makes the digital verification process much smoother for the lender. It shows you are organised and in control of your finances.

Ready to take the next step? Start your application today and find the loan that fits your life.

Empower Your Business Growth with Smarter Lending

The days of struggling with endless paperwork and high-street rejections are over. You now have the tools to secure funding based on your real-world cash flow rather than outdated paper records.

By using digital checks and a specialist broker, you can access financial products that fit your unique career path. Modern lending technology recognises your hard work. It can do this even if your income does not follow a standard PAYE pattern.

Finding self employed loans uk no proof of income is about choosing a path that prioritises your personal autonomy. Whether you are a contractor with income that changes, there is a solution for you.

Whether you are a homeowner using your home equity, there is a solution for you. We act as your advocate. We offer a non-judgmental gateway to a wide panel of independent UK lenders. They specialise in self-employment.

As an FCA Authorised and Regulated provider, we offer a safe, transparent, and free service with no obligation quotes. You can explore your options without any impact on your financial records until you’re ready to move forward. Don’t let traditional banking hold you back any longer. Check your eligibility for a self-employed loan now and discover the flexibility your business deserves.

Frequently Asked Questions

Can I get a loan if I have only been self-employed for 6 months?

Yes, you can often secure funding even with a short trading history by using digital verification. Traditional high-street banks often ask for two or three years of accounts.

Modern lenders use Open Banking to review your real-time turnover. This allows them to see the health of your business today rather than waiting for your first annual tax return.

Will applying for a self-employed loan affect my credit score?

Checking your eligibility through a broker usually involves a "soft search," which has no impact on your financial records. This allows you to see your personalised terms without lowering your credit score. A hard search happens only after you formally choose a specific lender. This helps protect your credit rating while you compare options.

How much can I borrow as a self-employed person without tax returns?

Borrowing limits vary based on your monthly cash flow and whether you own your home. Unsecured self-employed loans in the UK with no proof of income may range from £500 to £25,000. Homeowner loans can offer much larger amounts. Lenders check your affordability by reviewing your regular income using digital banking data, not paper SA302 forms.

What is the difference between a secured and unsecured self-employed loan?

The main difference is whether you use an asset like your home as collateral. A secured loan uses your home equity as collateral.

This often means a lower interest rate.

It can also let you borrow more money. An unsecured loan does not need any assets, so it can be faster. However, it may require better credit and offer lower maximum amounts.

Are self-employed loans more expensive than standard personal loans?

Interest rates are generally competitive, though they depend on your individual risk profile. In June 2026, representative APRs for unsecured loans range from 7.1% to 12.24% at major banks. Alternative lenders may charge more if your income is irregular.

Open Banking can help prove your income is stable.

This can lead to lower costs and more personalised terms.

Related links

Open Banking Loans – a modern guide

Smarter borrowing with Open Banking

How to get Car Loan approved first time

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.