Verify a Loan Company UK: 2026 Safety Guide

- May 29, 2026

- Remy Anderson

- Finance I Need Cash

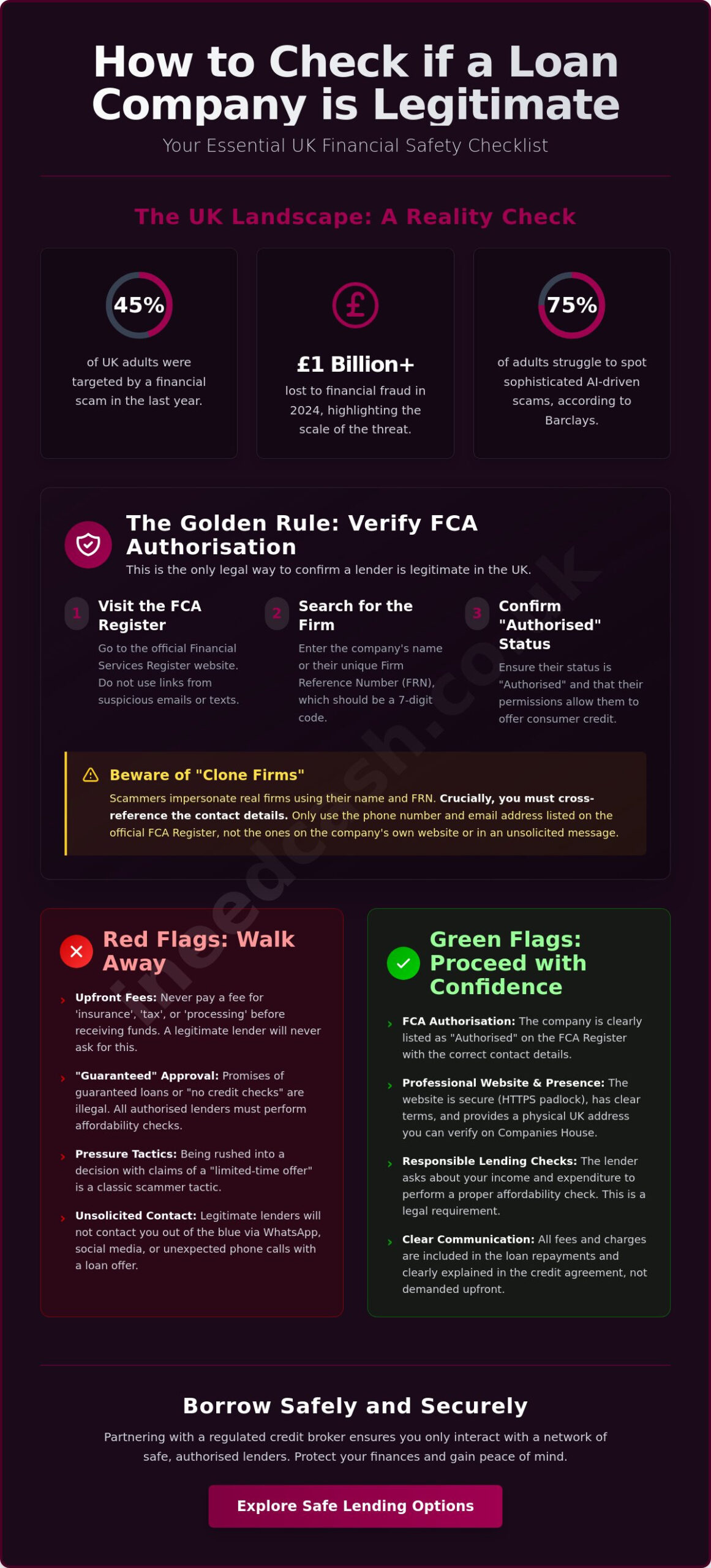

In 2025, 45% of UK adults were targeted by a financial scam. It’s a staggering figure that explains why you feel anxious when seeking financial assistance. With fraud losses topping £1 billion in 2024, knowing how to check if a loan company is legitimate uk is your best defence against identity theft.

You deserve to feel empowered, not pressured by unsolicited calls or confusing terms. This guide will help you avoid loan fraud and recognise loan scams UK while you verify a loan company UK with confidence.

We’re here to provide the assistance you need to verify any lender or broker with confidence. This guide provides a clear checklist to ensure your personal loan or homeowner loan is from an authorised source. "AI advances have made online scams more believable," notes a 2025 report by Barclays, which found that 75% of adults struggle to spot modern fraud.

We’ll preview how to use the FCA Register (your essential FCA Register check) and why checking Companies House is vital. You’ll gain the peace of mind you need to apply for short term loans, safe loans UK, or bad credit loans with no impact on your financial records.

Key Takeaways

- Search the Financial Services Register to confirm a lender’s status before sharing any personal data. It is the only legal way to be certain they are authorised to operate in the UK.

- Spot the “Upfront Fee” trap by walking away if a company asks for payment before releasing your funds. Legitimate lenders will never charge you for “insurance” or “processing” in advance.

- Verify physical addresses on Companies House and look for secure website symbols to protect your identity. These digital steps show you how to check if a loan company is legitimate uk.

- Partner with a regulated credit broker to access a network of safe lending options. This ensures you only interact with providers who follow the strict moral codes of UK regulation.

Table of Contents

The Golden Rule: Verifying FCA Authorisation in the UK

If you want to know how to check if a loan company is legitimate uk, start with the law. Under the Financial Services and Markets Act 2000, any firm offering consumer credit must be authorised. This isn’t a suggestion; it’s a legal mandate. The Financial Conduct Authority (FCA) serves as the UK’s watchdog, ensuring lenders treat you fairly.

Knowing how to check if a loan company is legitimate uk is vital since over £1 billion was stolen by fraudsters in 2024. Verifying a lender’s status is your primary safety net.

How to Use the Financial Services Register Correctly

Navigate to the official FCA Register to begin your search. Every legitimate firm has a Firm Reference Number (FRN). This is a unique seven-digit identifier for every regulated business. Enter this number or the company name into the search bar. Look for the status "Authorised" to ensure they can legally offer paydayloans or personal loans.

If a firm is listed as an "Appointed Representative", they are still under the regulator’s umbrella. Always check their "Activities and Services" tab to confirm they can lend money.

Defeating the "Clone Firm" Tactic

Scammers are getting clever. They often steal the names, addresses, and FRNs of real companies to create "clone firms". This is a major risk many guides miss. To beat this, only use the contact details listed on the FCA Register itself.

If the phone number on the lender’s website doesn’t match the one on the Register, close the tab immediately. Don’t trust unsolicited calls or emails, even if they quote a real FRN. Verifying the source directly from the regulator is the only way to stay safe whilst searching for short term loans or homeowner loans.

Immediate Red Flags: How to Spot a Loan Scam in 2026

Scammers are moving beyond cold calls. In 2026, they use WhatsApp and social media to hunt for targets. If you receive an unsolicited loan offer through an encrypted app, block the sender immediately. This is a vital step in how to check if a loan company is legitimate uk. Legitimate firms won’t slide into your DMs with "exclusive" deals. They value your privacy and follow strict marketing regulations.

Watch out for the "Upfront Fee" trap. Scammers often demand payment for "insurance" or "processing" before they release any cash. Action Fraud, the UK’s national reporting centre for fraud and cybercrime, states: "Legitimate lenders will not ask for payment via gift cards or cryptocurrency." If a firm asks for payment in vouchers, it’s a scam. No exceptions.

The Evolution of Loan Fee Fraud

Criminals now use sophisticated excuses like "holding fees" or "tax payments" to steal your money. According to official loan fee fraud guidance, this remains a massive threat. Loan fee fraud is currently one of the fastest-growing financial crimes in the UK. It preys on those who need immediate assistance. Pressure tactics are designed to stop you from thinking clearly.

Be particularly careful with homeowner loans. Whilst these involve formal property valuations, a real lender won’t ask for a random "admin fee" via a bank transfer. They’ll organise everything through professional, transparent channels. Always trust your gut. If a deal feels too fast or too easy, it probably is. Stop and verify before you send any money.

Guaranteed Approval and "No Credit Check" Myths

The phrase "guaranteed approval" is a massive red flag. Under FCA consumer credit rules, this type of advertising is actually illegal. Every legitimate lender must perform an affordability check to ensure you can manage the repayments responsibly. They have a moral and legal duty to protect you from spiralling debt. Promises of "no credit checks" usually signal a scammer or an unregulated loan shark.

Modern lenders use real-time data to provide fair assessments. This moves you from a state of anxiety to one of empowerment. You can safely explore your options and get started with a quote that respects your financial health. Real lenders want to help you succeed, not trap you in a scam. Always prioritise your security over the promise of "easy" money.

Practical Digital Checks: Assessing the Website and PresenceLooking at a website’s design isn’t enough to guarantee safety. You must dig into the digital DNA of the site. A "locked" padlock symbol in your browser bar confirms the site uses HTTPS for secure data transmission. Whilst this is essential, it only proves the connection is encrypted, not that the company is honest. It’s just the first step in how to check if a loan company is legitimate uk. Use a "WhoIs" lookup tool to see when the domain was registered. If the site was created only a few weeks ago, it’s a massive red flag.

Check the "Registered Office" address usually found in the website footer. Cross-reference this with the Companies House database to see if it’s a real business location. Scammers often use residential flats or virtual mailboxes to hide their true location. Legitimate firms must also provide a clear Privacy Policy.

This document should explain exactly how they handle your data under UK GDPR. If this page is missing or looks like a generic copy-paste job, protect your identity and leave the site immediately. A quick FCA Register check paired with these steps helps surface legit loan companies UK.

Analysing Independent Reviews and Feedback

Don’t take a perfect five-star rating at face value. Scammers often pay for fake reviews to build unearned trust. Look for "bursts" of feedback where dozens of generic five-star comments appear on the same day.

Real reviews for payday loans or personal loans are usually nuanced and mention specific experiences. A total lack of any online history or presence on major review platforms like Trustpilot is a warning sign. Authorised firms usually have a track record you can verify through independent research.

The "Contact Us" Test

Legitimate lenders and brokers always provide multiple ways to get in touch. This should include a UK landline and an official business email address. Be extremely wary of any firm using generic Gmail, Outlook, or Yahoo addresses for their official correspondence.

To be certain, Check the FCA Register to find the firm’s official phone number. Call that specific number to see if it reaches the same company you are dealing with. If the numbers don’t match, you’ve likely found a clone firm. Take control of your security and get started with a verified partner you can trust.

Borrowing Safely with a Regulated Credit Broker

Understanding the difference between a direct lender and a credit broker is essential. A broker like I Need Cash acts as a supportive intermediary. We work on your behalf to find the right fit from a panel of authorised lenders.

This pre-vetting process is a massive shortcut when you’re learning how to check if a loan company is legitimate uk. Every lender we connect you with has already passed rigorous regulatory checks, helping you engage only with legit loan companies UK.

Transparency and Legal Duty

Legitimate brokers must be open about their status. Check the website footer right now. You should see a clear legal name and FCA status. Unlike some shady operators, I Need Cash is a free service. We never charge you for our assistance. If a broker asks for money before matching you with a paydayloan, walk away immediately. Transparency is our moral code.

The Broker Advantage for Bad Credit Borrowers

If you have a poor credit history, you might feel marginalised by big banks. Scammers prey on this financial anxiety with "guaranteed" offers. A regulated broker provides a safe haven. When you request a bad credit loan quote through us, you’re using a secure, encrypted channel. We help you avoid "scattergun" applications.

This protects your credit score from multiple hard searches whilst keeping your data safe and guiding you toward safe loans UK options.

Final Checklist Before You Apply

Don’t let pressure tactics rush your decision. Take a breath and run through these "Big Three" checks one last time. First, verify the firm on the FCA Register (your essential FCA Register check). Second, ensure there are no upfront fees. Third, confirm the website is secure with HTTPS.

These steps are the definitive way how to check if a loan company is legitimate uk. If anything feels wrong, report it to Action Fraud immediately. Stay sharp. You have the autonomy to choose a safe path.

Ready to find a safe, regulated loan? Get started with a secure quote today.

Secure Your Financial Future with Confidence

You now have the definitive toolkit to spot scammers before they strike. Remember that the Financial Services Register is your ultimate shield against fraud. Never pay an upfront fee for a loan; legitimate lenders simply don’t operate that way.

By following these essential steps on how to check if a loan company is legitimate uk, you move from a state of financial anxiety to total empowerment. You deserve a solution that respects your personal autonomy whilst protecting your digital identity from sophisticated 2026 scam tactics and helping you avoid loan fraud.

Take the next step without the stress of uncertainty. We are Authorised and Regulated by the Financial Conduct Authority (FCA), providing a completely free service that puts your needs first.

Our extensive panel of regulated UK lenders ensures you access a wide range of options with no impact on your financial records during the initial quote. Our moral code is built on transparency and speed, ensuring you feel the tranquility of a safe solution. It’s time to stop worrying about identity theft and start moving forward with a partner that values your security.

Check your eligibility with an FCA-authorised broker today and discover a safer way to borrow. Your peace of mind is our priority.

Q&A

Is it normal for a loan company to ask for a fee before I get the money?

No, it is never normal. Legitimate providers of short term loans or homeowner loans will never ask for money upfront. If there are fees, they’re usually added to the loan balance or deducted from the cash you receive. Scammers often use the term "loan fee fraud" to describe this tactic. If you’re asked for a "holding deposit" via bank transfer or gift cards, stop the process immediately. This is one of the most common loan scams UK.

What should I do if I think I have been scammed by a fake lender?

Act fast by contacting your bank to freeze your accounts and stop any pending transfers. You should also report the scam to Action Fraud and consider registering with Cifas for protective registration. This adds a layer of security to your credit file to prevent identity theft. Knowing how to check if a loan company is legitimate uk after an incident helps you verify other firms before you try to recover your losses.

How can I tell if a loan website is a "clone" of a real company?

Look closely at the email address and website URL for subtle inconsistencies. Legitimate firms use professional domains, not generic ones like @gmail.com or @hotmail.co.uk. A clone firm might use a web address that is slightly different from the real one, such as adding a hyphen or an extra letter. Always cross-reference the URL with the official link provided on the Financial Services Register to ensure you’re on the right site.

Can I get a loan from a company that is not registered with the FCA?

Borrowing from an unauthorised company is extremely risky and often illegal for the lender. If a firm isn’t registered with the FCA, you lose access to the Financial Ombudsman Service if things go wrong. This means you have no professional body to help you resolve disputes or reclaim unfair charges. Using the Register is the primary way how to check if a loan company is legitimate uk and ensure you have full legal protection. Always complete an FCA Register check first.

Do legitimate lenders offer "guaranteed" loans for people with bad credit?

No, the FCA explicitly bans lenders from promising "guaranteed" approval in their advertising. Every authorised lender must conduct a proper assessment of your finances to ensure the loan is affordable. This protects you from taking on debt that could lead to financial distress. Whilst you can still find bad credit loans, the final decision always depends on your current income and credit behaviour. Any firm ignoring this rule is likely a scam.

What’s the correct way to verify a lender on the FCA Financial Services Register?

Go directly to the FCA’s official Register and search by the firm’s name or its seven‑digit Firm Reference Number (FRN). Check that the status is “Authorised” (or that they’re an “Appointed Representative” of an authorised firm) and review the “Activities and Services” section to confirm they’re permitted to lend. Then match the firm’s phone number, email and web address against what’s shown on the Register and use only those official contact details. If anything doesn’t match, treat it as unsafe and walk away.

What is a “clone firm” and how do I avoid being tricked by one?

Clone firms copy the name, address and even the FRN of a genuine company to look legitimate. The quickest defence is to ignore any contact details shown on ads, emails, texts or the firm’s own site until you’ve cross‑checked them on the FCA Register. Only use the Register’s phone number and web link. If a caller or message came via WhatsApp or social media, or the number/URL doesn’t match the Register entry, close the tab, block the sender and do not engage—it’s a hallmark of a clone operation.

Does a padlock icon mean a loan website is safe? What other digital checks should I do?

No. The padlock (HTTPS) only confirms the connection is encrypted, not that the company is honest. Strengthen your checks by:

- Running a WhoIs lookup to see when the domain was registered; a brand‑new domain is a red flag.

- Cross‑referencing the “Registered Office” shown in the site footer with Companies House records.

- Ensuring there’s a clear, UK‑GDPR‑compliant Privacy Policy (not a generic copy‑paste).

- Applying the “Contact Us” test: look for a UK landline and a professional business email—not free Gmail/Outlook/Yahoo addresses—and confirm the phone number matches the FCA Register.

What are the biggest red flags that a loan offer is a scam?

Be wary of:

- Any request for an upfront payment (e.g., “insurance,” “processing,” “holding fees,” “tax”)—especially via bank transfer, gift cards or cryptocurrency.

- “Guaranteed approval” or “no credit check” claims—these breach FCA rules; real lenders must assess affordability.

- Unsolicited approaches via calls, emails, WhatsApp or social media DMs.

- Contact details that don’t match the FCA Register, generic email domains, or no UK landline.

- A brand‑new website/domain, vague or missing Privacy Policy, and bursts of too‑perfect online reviews.

- For homeowner loans, any demand for random “admin fees” paid separately by transfer.

How can a regulated credit broker help me borrow safely—especially with bad credit—without harming my credit file?

A regulated broker pre‑vets a panel of FCA‑authorised lenders and matches you to suitable options, so you avoid “scattergun” applications and only deal with legit providers. A reputable broker is transparent about its FCA status (shown in the footer), does not charge you upfront, and offers a secure, encrypted quote process. As outlined in the guide, the initial quote has no impact on your financial records, helping protect your credit while you explore safe loans UK.

Related links

Understanding 24 7 loans UK: What to expect

1000 Loan bad credit UK Direct Lender Guide

And I need help: Where to find financial assistance resource

Best Paid Online survey site 2023

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a loan brokerage. Speaking to individuals seeking guidance led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.