Bad Credit Homeowner Loans: Direct Lender vs Broker – Which is Better in 2026?

- May 25, 2026

- Remy Anderson

- Finance

Applying to your local bank for a loan might be the fastest way to damage your financial future in 2026. If you are weighing up bad credit homeowner loans direct lender vs broker, you likely already know that high street institutions prioritise rigid algorithms over your actual circumstances. It is exhausting to feel like a number. We are here to support your journey and help you move from financial anxiety to tranquility. We understand the fear of rejection when you are simply trying to unlock equity in your property.

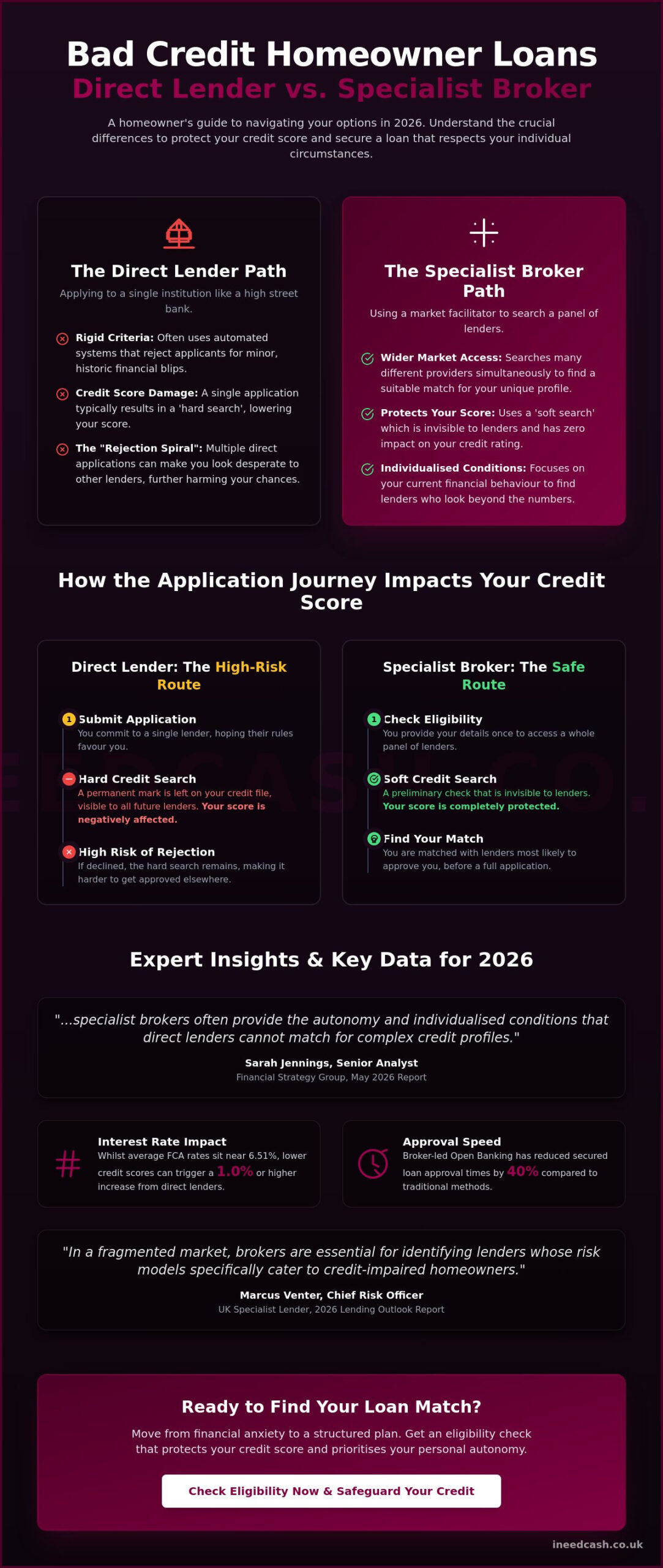

You deserve a route that protects your credit score whilst finding a cost-effective APR. Sarah Jennings, a Senior Analyst at the Financial Strategy Group, stated in their May 2026 report that “specialist brokers often provide the autonomy and individualised conditions that direct lenders cannot match for complex credit profiles.” Data from the Financial Conduct Authority (FCA) shows that whilst average interest rates sit near 6.51%, lower scores can trigger a 1.0 percentage point increase. This guide compares the speed and approval rates of both paths to help you take control. Discover how to avoid hidden fees and secure funds with the right assistance, using insights from the Office for National Statistics.

Key Takeaways

- Understand the core differences in bad credit homeowner loans direct lender vs broker to see why a panel-based approach often wins on approval rates.

- Learn how modern Open Banking technology allows specialist brokers to verify your income instantly for a faster, smoother application.

- Discover how to safeguard your credit score by avoiding multiple hard searches through a single, intelligent broker search.

- Identify the specific scenarios where a direct lender might work versus when a broker is essential for non-judgmental assistance.

- Move from financial anxiety to a structured loan match that prioritises your personal autonomy and individualised conditions.

Homeowner Loans for Bad Credit: The Direct Lender vs Broker Dilemma

Deciding how to access equity in your property when your credit score is less than perfect feels like a high-stakes gamble. You are likely facing a choice between two distinct paths. A direct lender is a single source of funds that uses rigid, internal criteria to decide if you qualify. Conversely, a credit broker acts as a market facilitator. They organise a search across a panel of different providers to find a match for your unique circumstances.

Safety and Regulation in the UK Market

When looking at bad credit homeowner loans direct lender vs broker options, remember that both paths are FCA regulated. This ensures you have immediate security and professional protection whichever route you take. We understand that choosing a loan with bad credit can feel stressful, but these regulations exist to protect your interests and ensure ethical lending practices across the industry.

Why Traditional Bank Loyalty Often Fails Homeowners

High street banks typically favour “perfect” credit profiles. They often reject homeowners for minor financial blips that happened years ago. This is where the real danger begins. A single rejection from your long-term bank can trigger a “rejection spiral.” If you keep applying directly to different lenders, every hard search leaves a permanent mark on your file. This makes you appear desperate to other providers, which can further damage your score and limit your future choices.

The Broker as Your Financial Ally

Think of a specialist broker as a supportive partner rather than a gatekeeper. They look beyond a simple number to understand your current financial behaviour. Some direct lenders claim that using a Mortgage broker or loan intermediary involves “hidden fees.” However, many modern facilitators operate on a model that is free for the applicant. This provides you with personal autonomy. You can access homeowner loans with individualised conditions that adapt to your specific needs.

The Mechanics of Lending: How the Application Journey Differs

The journey you take depends on how much risk you want to manage yourself. Applying to a direct lender is a one-to-one commitment. You present your case to a single entity and hope their internal rules favour you. A broker offers a one-to-many search. They scan multiple providers simultaneously to find the best fit for your profile. This is vital when weighing up bad credit homeowner loans direct lender vs broker paths.

Protecting Your Credit Score During the Search

Brokers use a ‘soft search’ safety net to protect your score whilst you compare. A soft search is a preliminary check that doesn’t leave a visible footprint. Open Banking loans allow brokers to verify your income instantly. David Thorne, Head of Lending at UK Finance Tech, noted in his 2026 Digital Credit Review: “Real-time data sharing has reduced approval times for secured loans by 40% compared to traditional manual underwriting.”

The Direct Lender’s Process

Direct applications almost always involve a ‘hard search.’ This leaves a permanent mark on your credit file. If you are rejected, that mark stays there for other lenders to see. There is also a risk of internal bias. If a lender’s board decides to reduce their exposure to “higher risk” borrowers mid-application, your request might be declined regardless of your personal merits.

The Broker’s Digital Edge in 2026

In 2026, sophisticated algorithms match you to a homeowner loan in seconds. These digital tools understand which lenders on a panel currently have an appetite for bad credit. You gain an advocate who knows the market’s latest shifts. They guide you toward providers who value your current behaviour over past mistakes. If you want to see what options are available without damaging your record, check your eligibility now.

Strategic Comparison: When to Choose a Bank vs. a Credit Broker

Bank loyalty makes sense for “Direct Winners” with perfect files and long-standing relationships. For most homeowners, a broker is the “Broker Winner.” Marcus Venter, Chief Risk Officer at a UK specialist lender, noted in the 2026 Lending Outlook Report: “In a fragmented market, brokers are essential for identifying lenders whose risk models specifically cater to credit-impaired homeowners.” They find the lowest APR amongst dozens of providers, dispelling the myth that they are just middlemen who add unnecessary costs.

Navigating the ‘Bad Credit’ Barrier

When weighing bad credit homeowner loans direct lender vs broker options, remember that banks use binary “yes/no” filters. Brokers bypass these by accessing specialist lenders who look at current affordability. This is crucial as Office for National Statistics data indicates that shifting economic pressures in early 2026 have impacted millions of UK credit scores. A broker provides the individualized conditions needed to move past these rigid filters and secure funds.

Complex Income and Self-Employed Solutions

Use a broker if you have a complex income, such as being self-employed or having multiple revenue streams. Direct lenders often struggle with non-standard pay slips or seasonal earnings. A broker acts as an advocate, presenting your case to lenders who understand modern work patterns. They find the most cost-effective deal by comparing your specific profile against a vast panel of providers who appreciate non-traditional financial behaviour.

Speed and Urgency: Who Wins the Race?

Contrast a traditional bank appointment with a modern digital search. A bank may take weeks to process a manual underwriting request. A broker uses a rapid cash loan application to find matches in minutes. If you need an urgent, non-judgmental decision that respects your time, start your search today and see your options without damaging your credit record.

Securing Your Homeowner Loan with Confidence

Securing a loan when your credit history is less than perfect shouldn’t feel like an uphill battle. You have already seen the differences in bad credit homeowner loans direct lender vs broker models. Now is the time to move from financial anxiety to empowerment. We promise a free, non-judgmental service that works on your behalf. We aren’t here to judge past mistakes. We are here to facilitate a successful match that respects your personal autonomy. Your financial record is a history, not a life sentence.

The Checklist for a Successful Application

Preparation is the key to a rapid turnaround. Organise your documents early to avoid delays. Follow these steps for a smoother journey:

- Check your equity: Know the current market value of your property versus your remaining mortgage.

- Verify your income: Have your recent bank statements ready or use Open Banking for instant verification.

- Use a soft-search broker: Protect your score whilst exploring your eligibility across multiple lenders.

- Compare the real APR: Look beyond the headline rate to see the total cost.

The Annual Percentage Rate (APR) includes all interest and mandatory fees, making it the most reliable way to compare the true cost of different offers. This transparency ensures you find a cost-effective solution without hidden surprises.

Your Next Steps to Financial Tranquillity

Stop the guesswork and start a safe, professional search. By choosing a partner that understands the bad credit homeowner loans direct lender vs broker landscape, you gain access to individualised conditions. We act as your advocate, scanning our extensive network to find providers who value your current behaviour. Past defaults or CCJs don’t have to dictate your financial future. Take control of your equity and find the flexibility you deserve. Get started with your homeowner loan search today and see your options!

Take Control of Your Financial Future

Choosing between bad credit homeowner loans direct lender vs broker doesn’t have to be a source of stress. You now understand that whilst banks offer familiarity, specialist brokers provide the agility and personalised conditions needed for complex credit histories. By using soft-search technology, you can protect your score whilst exploring a vast panel of independent UK lenders who look beyond your past mistakes. This approach moves you from a state of anxiety to one of empowerment and tranquility.

I Need Cash acts as your supportive partner in this journey. We are an FCA regulated broker, ensuring ethical and secure lending practices at every step. Our service is completely free for applicants with no hidden upfront brokerage fees. You gain immediate access to a network of providers who specialise in non-judgmental assistance. Stop worrying about high street rejections and start looking forward to the flexibility your home equity can provide. Start your free, non-judgmental homeowner loan search with I Need Cash now! Your past doesn’t define your potential; let us help you find the right path today.

Frequently Asked Questions

Is it cheaper to get a homeowner loan from a bank or a broker?

A broker is often cheaper for those with poor credit because they compare multiple rates to find the lowest APR available. While banks might offer lower headline rates to “perfect” customers, a broker prevents you from accepting a high-interest default option by scanning a wider panel. This ensures you get the most cost-effective deal tailored to your specific financial behaviour and current affordability.

Can I get a homeowner loan with very bad credit through a broker?

Yes, brokers specialise in connecting homeowners with lenders who have a high appetite for risk and look beyond a simple credit score. Unlike traditional banks with rigid filters, brokers use specialist panels to find individualised conditions for those with defaults or CCJs. This is the most effective way to navigate the bad credit homeowner loans direct lender vs broker choice when your financial history is complex.

Will applying through a credit broker affect my credit score?

No, initial searches through a reputable broker use soft search technology that has zero impact on your financial records. This acts as a safety net. It allows you to check eligibility and compare options without leaving a visible footprint for other lenders to see. You only undergo a hard search once you choose a specific offer and proceed with a formal application, protecting your score during the search.

How much do brokers charge for finding a homeowner loan in the UK?

Many brokers provide a free service to applicants where the lender pays the commission instead of the borrower. This eliminates the confusion over hidden fees that often causes anxiety during the loan search. Always check the initial disclosure document to confirm there are no upfront costs. This ensures your path to financial tranquillity remains affordable, transparent, and focused on your personal autonomy.

Why did my bank reject my homeowner loan application but a broker found me a deal?

Banks use automated systems based on rigid internal criteria, whereas brokers use advocates to match you with flexible providers. A broker understands which lenders on their panel are currently favouring bad credit profiles. This individualised approach bypasses the traditional barriers that lead to high street rejection. It offers you a supportive route to securing funds that your local bank branch simply cannot match.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.