Loan Computation: A Comprehensive Guide to Calculating Your Borrowing in 2026

- May 19, 2026

- Remy Anderson

- Finance

What if the difference between a manageable monthly repayment and a financial headache was just five minutes of basic maths? You don’t need a finance degree to master loan computation. With average personal loan rates reaching 12.27% in May 2026, knowing your numbers is your best defence. It’s time to take control of your borrowing today.

We know how stressful it is to face confusing jargon or fear rejection due to your credit history. You want a repayment plan that fits your lifestyle, not one that keeps you awake at night. This guide promises to clear the fog and provide the assistance you need. You’ll learn to compare APRs and find the most cost-effective Personal or Homeowner Loans amongst a sea of UK lenders. We’ll preview the latest 2026 interest trends and regulatory shifts to give you total autonomy over your financial future.

Key Takeaways

- Master the essentials of loan computation to accurately predict your monthly repayments and find the most cost-effective deal amongst UK lenders.

- Learn why a lower monthly payment might actually signal a higher total cost over the life of your loan.

- Discover the mathematical differences between using property equity for homeowner loans versus the flexibility of unsecured personal loans.

- Understand how lenders assess risk for those with imperfect credit histories and why your data isn’t a final verdict.

- Gain the confidence to use a broker as your advocate to help you organise your finances and access a diverse panel of providers with a single application.

What is Loan Computation and Why Does it Matter for You?

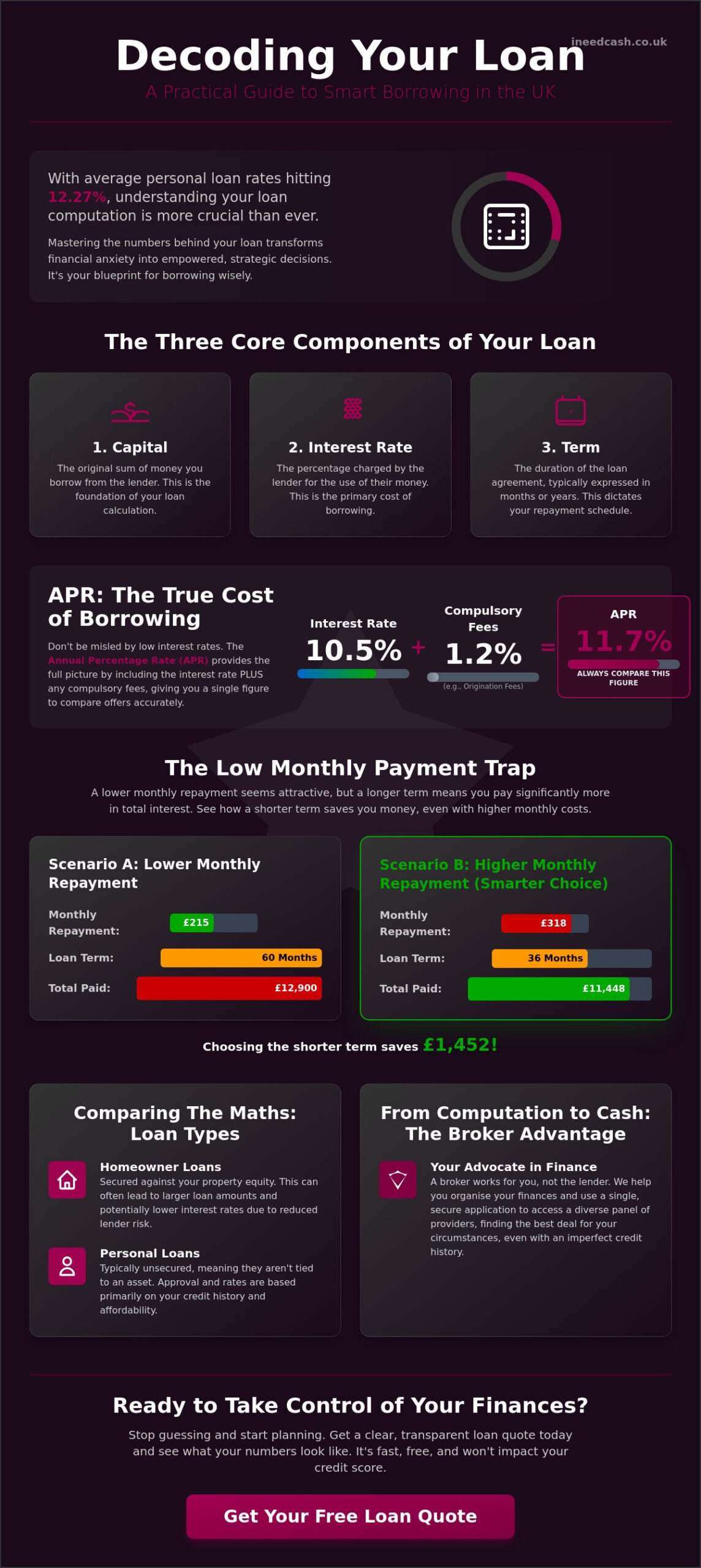

Think of loan computation as the financial blueprint for your borrowing. It is the precise method used to determine your monthly repayments, the total interest you will pay, and the final cost of the credit. Without this calculation, you are essentially signing a contract without reading the price tag. Mastering these figures allows you to organise your household budget with absolute autonomy whilst ensuring you never overextend your resources. It transforms a complex financial product into a clear, manageable plan that fits your life. Transparency in these calculations is the foundation of trust between you and your broker. When a provider is open about how they reached a specific figure, it moves you from a state of financial anxiety to a feeling of tranquility. It is about your personal agency. You deserve to see the inner workings of your deal. This level of clarity helps you stay in control of your financial behaviour, turning what could be a stressful transaction into an empowered, strategic choice. High-quality assistance means never being left in the dark about where your money is going. It is vital to distinguish between a preliminary quote and a final loan computation. A quote is typically an estimate based on a soft credit search, which won’t impact your financial records. A final computation only occurs after a full application and a hard search. This final figure reflects your individualized conditions, such as your exact income and credit history. If you want to see what your specific numbers might look like, you can apply for a loan quote today to begin the process with total security.The Core Components of Your Calculation

Every loan calculation relies on three main ingredients. First is the Capital, which is the original sum you borrow. Second is the Interest, the fee charged by the lender for the use of that capital. Finally, the Term is the duration of the agreement, which dictates the rhythm of your repayments. These elements are combined to create an Amortization schedule. This schedule is a detailed table showing exactly how each payment is divided between the principal and the interest over the entire life of the loan.The Role of the Financial Conduct Authority (FCA)

UK regulations are built to protect your interests. The Financial Conduct Authority (FCA) ensures that all lenders and brokers provide transparent calculations. This includes the requirement for representative examples in all marketing materials, allowing you to see a realistic cost of borrowing before you commit. Regulated brokers like I Need Cash prioritise your financial safety by following these strict ethical standards. Whether you are looking for Homeowner Loans or personal credit, we ensure the numbers are fair and clear.The Anatomy of the Calculation: APR, Interest, and Fees

APR is the single most important number in your loan computation. It is the real price of borrowing. Lenders often shout about low interest rates, but the APR tells the full story. It combines the interest rate with compulsory fees, like origination charges. If you want to know how to calculate loan payments accurately, you must look at the APR. It ensures you are comparing like for like amongst different UK providers. It is your shield against misleading marketing and hidden surprises. Don’t let hidden costs catch you out. Many loans come with origination fees that typically range from 0.5% to 1% of the total amount. If you have a lower credit score, these fees can climb as high as 12% according to data from May 2026. These costs are often deducted from the cash you receive. Your loan computation needs to account for the net amount you actually get in your bank account. Always check for early repayment charges too. These can penalise you for being proactive with your finances, so read the fine print before you sign any agreement. A common trap is focusing only on the monthly figure. A lower monthly payment feels easy on the wallet, but it often means a much higher total cost. This happens because you are borrowing the money for longer, allowing interest to accumulate over years rather than months. Most UK loans also front-load interest. This means your early payments primarily cover the lender’s profit rather than reducing your original debt. Understanding this helps you organise your finances with more confidence and clarity.Fixed vs Variable Rates: Computing the Risk

Stability or flexibility? Fixed rates offer total peace of mind. Your payment stays the same every month, regardless of economic shifts. Variable rates can be cheaper at the start, but they carry the risk of rising if national interest rates climb. Choose the path that fits your favourite way to manage your budget. If you prefer certainty, fixed is your best bet. If you can handle a little movement for a potentially lower rate, variable might work for you.The Impact of Loan Terms on Your Total Repayable

Time is money. Short-term loans have higher monthly costs but lower total interest. Long-term loans spread the cost, making them affordable day-to-day, but the total repayable amount will be significantly higher. Find the sweet spot where you can comfortably afford the monthly payment without paying a fortune in interest over the years. Balance is key. Aim for the shortest term you can realistically manage to keep your total costs as low as possible.Homeowner Loans vs Personal Loans: Comparing the Maths

Your choice between a secured and unsecured loan changes the entire landscape of your loan computation. If you own your home, you have a powerful financial asset that can unlock lower rates and higher borrowing limits. Personal loans are unsecured, meaning they rely purely on your credit score and income. Homeowner loans, however, use your property as security. This reduces the risk for the provider, often resulting in a more cost-effective APR compared to unsecured options. It is a strategic way to leverage your hard-earned equity for your benefit. Computing the “Loan to Value” (LTV) ratio is a vital step for any homeowner. This figure represents the percentage of your home’s value that you are borrowing against. Lenders use this to determine your individualised conditions. For example, if your home is worth £300,000 and you have a £150,000 mortgage, your current LTV is 50%. A lower LTV usually triggers better offers because the lender feels more secure. Calculating loan payments based on this ratio helps you see exactly how much “room” you have to borrow whilst maintaining a safety net. Personal loans don’t require collateral, which makes them faster to process but often more expensive. As of May 2026, the average personal loan rate sits around 12.27% for those with good credit. In contrast, home equity-based products often hover at lower averages, such as 8.03% for certain terms. This difference can save you thousands of pounds over the life of the agreement. When performing your loan computation, always weigh the speed of an unsecured loan against the long-term savings of a homeowner-specific product.Computing Your Available Home Equity

Find your borrowing power by looking at current market trends. Start by estimating your property’s value amongst similar homes in your area. Subtract your remaining mortgage balance from this total. The result is your available equity. Homeowners have more flexibility because they can often spread repayments over a longer term, which lowers the monthly burden. This autonomy allows you to organise your finances without the immediate pressure of high monthly outgoings.Which Loan Type Wins for Your Situation?

The right choice depends on your goal. If you are computing for major home improvements, homeowner loans are usually the favourite choice. They provide the large sums needed for extensions or renovations at a lower cost. If you are dealing with emergency costs or smaller purchases, a personal loan or short-term loan might be better. These options offer immediacy and don’t involve your property. You can explore our Homeowner Loan options to see which mathematical path leads to your ideal solution.Loan Computation for Bad Credit: Navigating Imperfect Histories

Bad credit is just a data point. It is not a final verdict on your character. We believe in personal autonomy and looking forward, not back. When lenders perform a loan computation for someone with a history of CCJs or defaults, they are essentially measuring your current risk. They look at your present ability to pay rather than just your past mistakes. This approach opens doors that traditional banks often slam shut. It’s about finding a solution that works for your current lifestyle and needs. There is a clear trade-off to understand. Accessibility and speed often come with higher APRs. For those with bad credit, interest rates can reach 35.99% or higher according to data from April 2026. This reflects the increased risk the lender is taking. However, this isn’t just a cost; it’s an opportunity. Consistent, on-time repayments are the fastest way to compute a path to credit recovery. Every instalment you pay on a Bad Credit Loan helps rebuild your financial reputation. You are essentially buying back your credit score with every successful payment. Our role is to act as your supportive advocate. We work with an extensive network of providers to find the most flexible terms for your specific situation. You aren’t just another number to us. We prioritise your financial safety and ensure you have the information needed to make an empowered choice. If you need immediate assistance, apply now to see your options and take back control of your financial journey.The “Soft Search” Advantage

Brokers use a soft search to compute your eligibility. This is a vital technical reassurance for your peace of mind. A soft search allows us to scan our panel of lenders without leaving a mark on your financial records. It protects your credit score whilst you explore your options. You can see your potential terms with total security. It’s a risk-free way to find the help you need without the fear of further damage. We ensure the process is transparent and fast.Budgeting for Higher Interest Rates

Organise your weekly budget to handle the higher costs of these loans. When interest rates are higher, shorter terms are often your best friend. They keep the total interest from spiralling out of control over many years. Focus on what you can realistically afford each week. A repayment plan should feel like a bridge to tranquility, not a burden. If you are ready to take the first step towards empowerment, you can get a loan quote today. It’s time to stop worrying and start planning your future.From Computation to Cash: The Broker Advantage

Mastering the maths is only the first step. Now you need to turn that knowledge into a tangible solution. This is where a broker becomes your most valuable advocate. Instead of spending hours filling out forms for dozens of different banks, you use one single application. We act as a digital-first intermediary, working on your behalf to find the most cost-effective deal amongst our extensive network of providers. It is about speed, efficiency, and personal agency. A broker simplifies the final loan computation by doing the heavy lifting for you. We understand that financial anxiety often stems from a lack of choice or fear of rejection. By accessing a diverse panel of lenders, we increase your chances of finding a repayment plan that fits your lifestyle. You maintain total autonomy throughout the process. You review the offers, compare the terms, and choose the path that makes sense for your budget. We provide the assistance; you make the decisions. Speed is a core part of our mission. In the fast-moving economy of May 2026, you shouldn’t have to wait weeks for an answer. Our technology allows you to move from your initial loan computation to a formal approval in record time. We strip away the traditional formalities that slow down high-street banks. This modern approach ensures you get the cash you need without the unnecessary stress of long procedures. It’s a supportive service designed for the modern borrower.The I Need Cash Process: Simple and Effective

Getting started is straightforward. First, tell us your needs and your preferred loan amount. Second, our technology instantly computes the best matches amongst our lender panel. Finally, you receive tailored offers with clear, transparent computations. There are no hidden surprises or confusing jargon. Just honest, helpful options presented in a way that empowers you to take the next step with confidence.Ready to Organise Your Finances?

There is a unique tranquility that comes from having a clear financial plan. You no longer have to guess about your borrowing costs or worry about the impact on your future. Now is the best time to take control of your borrowing and find a solution that respects your past whilst protecting your future. We are here to facilitate your success. If you are ready to move from calculation to cash, start your application now and see what our network can do for you.Take Control of Your Financial Future Today

You now have the tools to master your borrowing. You understand that a lower monthly payment doesn’t always mean a better deal. You know how to leverage your home equity or navigate the market with a less than perfect credit history. This knowledge moves you from a state of financial anxiety to one of total empowerment. It’s time to put your loan computation into practice and find the flexibility you deserve. You are ready to organise your budget with absolute confidence. We provide a free service for all applicants, giving you access to a wide panel of UK lenders with a single search. As an FCA authorised and regulated broker, we prioritise your financial safety and personal autonomy. Our process is fast, transparent, and designed to fit your unique lifestyle. Don’t let confusing jargon or past mistakes hold you back any longer. We are here to act as your advocate and facilitate the solution you need. Get your personalised loan computation today and see how simple borrowing can be. Take the first step towards financial tranquility and start your journey now. You have the power to change your story.Frequently Asked Questions

How is a loan repayment calculated in the UK?

Your monthly repayment is calculated by combining the total amount you wish to borrow with the interest rate and spreading that sum over your chosen term. UK lenders use a specific mathematical formula to ensure each payment covers a portion of the original capital whilst also paying off the interest due for that period. This creates a fixed monthly figure that allows you to organise your budget with total certainty and peace of mind.Does a loan computation include all the fees I will have to pay?

A comprehensive loan computation should include all compulsory costs through the APR. This figure combines the interest rate with essential charges like origination fees, which often range from 0.5% to 1% for standard loans. However, optional fees or charges for late payments are typically not included in the initial calculation. Always review your agreement to ensure you have a transparent view of every potential cost before you commit.Can I change my loan term after the initial computation?

You can adjust your loan term at any point before you sign the final agreement. Changing the duration will immediately alter your monthly outgoings and the total interest you will pay over the life of the loan. Shortening the term increases your monthly payment but saves you money in the long run. Extending the term lowers the monthly burden but adds to the total cost, so choose the balance that fits your lifestyle.Why is the APR on my computation different from the representative APR?

The representative APR is a marketing figure that lenders must offer to at least 51% of successful applicants. Your personal loan computation is based on your individualised conditions, including your specific credit history, income, and employment status. If you have a lower credit score or unique financial circumstances, your personal rate may be higher than the headline figure you saw in an advertisement or on a comparison site.Will checking my loan computation affect my credit score?

Checking your options with a broker usually involves a soft search, which has no impact on your financial records. This technical reassurance allows you to explore different lenders and compare terms with total security. A hard search only occurs when you decide to proceed with a full application for a specific product. It is a risk-free way to find the assistance you need without worrying about damaging your credit score.How does my home equity affect the loan computation for a homeowner loan?

Your home equity is the primary factor used to determine your Loan to Value (LTV) ratio. Having more equity usually results in a more favourable calculation because the lender’s risk is significantly reduced. This often unlocks access to larger loan amounts and lower interest rates that aren’t available through unsecured personal loans. It is a strategic way to leverage your property to secure more cost-effective borrowing terms for your future.What happens if I want to pay off my loan earlier than computed?

You have the legal right to settle your loan early, but you should check your agreement for early repayment charges first. These fees are designed to cover the lender’s lost interest and are usually capped by regulation. Paying off your debt ahead of schedule can save you a significant amount in total interest costs. Always perform a quick check to ensure the savings from paying early outweigh any exit fees charged by the provider.Can a broker help me find a lower computation than a direct lender?

A broker acts as your advocate by searching an extensive network of providers to find the most competitive deal for your situation. Whilst a direct lender only offers their own specific products, a broker compares multiple options simultaneously. This increases your chances of finding a lower interest rate and a repayment plan that offers the flexibility you need. It is an efficient way to access a diverse panel of lenders with a single application.

Article by

Mandy Paige

Social Content Writer and Blogger. Mandy has been writing for various websites for a number of years, particularly for companies in the consumer finance industry. She began her career guiding customers who needed assistance when applying for finance at a loan brokerage. Speaking to individuals seeking guidance led her to start writing advice and guidance on finding the right solution for their needs. Outside of writing, she’s a whizz with a pair of scissors, having originally trained as a hairdresser.