Cheap Personal Loans UK Bad Credit: A 2026 Guide to Lower Rates

- May 15, 2026

- Remy Anderson

- Finance

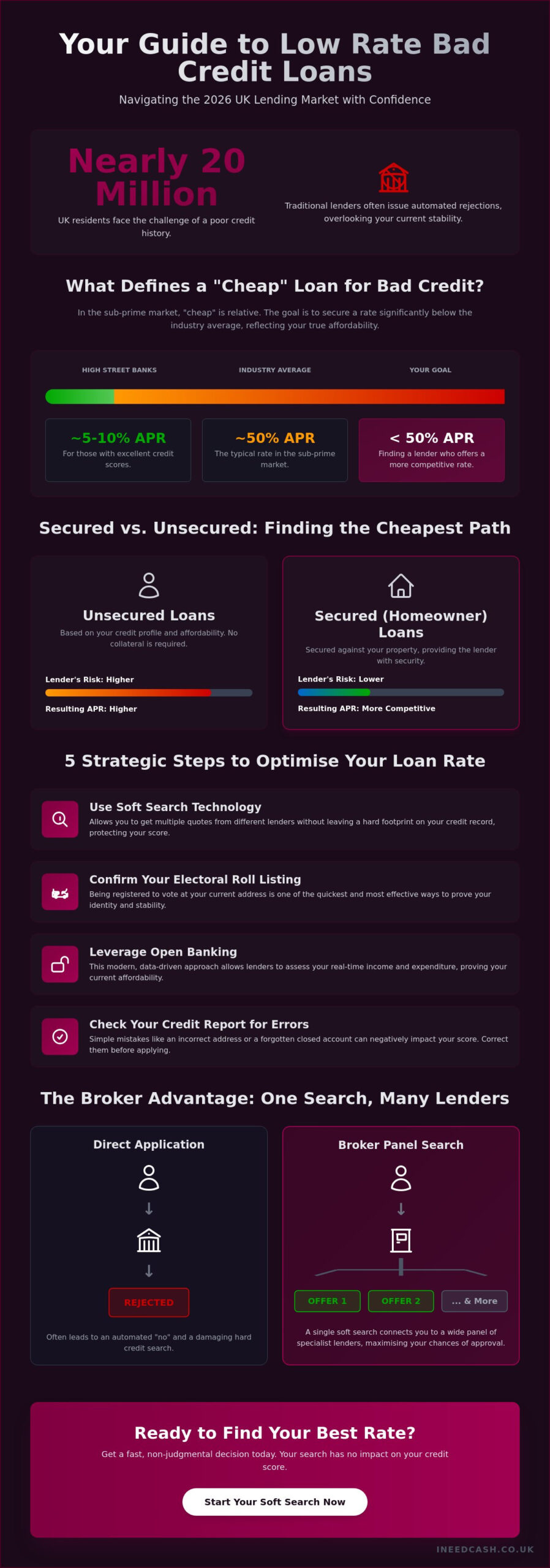

Nearly 20 million UK residents are currently navigating the challenges of a poor credit history, yet traditional lenders often respond with judgment rather than assistance. You likely feel that your past shouldn’t define your financial potential, especially when you’re working hard to maintain a stable household. It is exhausting to face high-interest traps or the constant fear of hard credit searches. You deserve access to low rate bad credit loans uk that respect your current situation and provide a clear, transparent total cost of credit.

Discover how to secure the most competitive personal loan rates in 2026 whilst protecting your credit score from unnecessary damage. We promise to reveal the exact strategies for finding a fast, non-judgmental decision that prioritises your actual affordability over an old score. This guide previews the shift toward data-driven lending, showing you how to lower your monthly repayments and find a supportive partner who values your personal autonomy. Take the first step toward financial empowerment and tranquillity today.

Key Takeaways

- Learn why “cheap” in the 2026 sub-prime market is defined by interest rates significantly lower than the 50% APR industry average.

- Discover how to access low rate bad credit loans uk using soft search technology that allows for multiple quotes without impacting your credit record.

- Understand the cost-saving benefits of homeowner loans and how providing security can unlock more competitive rates than unsecured alternatives.

- Identify the importance of the UK Electoral Roll and Open Banking in proving your current affordability and identity to lenders.

- See how a single application through a broker panel provides a fast, non-judgmental decision by connecting you with a wide network of specialist providers.

What Defines a Cheap Personal Loan for Bad Credit in the UK?

In the UK’s sub-prime market, the concept of a “cheap” loan is entirely relative to your specific credit history. Whilst high-street banks offer single-digit rates to those with perfect scores, the reality for those with past defaults is an industry average closer to 50% APR. Therefore, finding low rate bad credit loans uk means identifying products that sit comfortably below this threshold. It is about locating a lender that views your current stability as a reason to lower the cost of borrowing. Lenders use your financial behaviour to measure the risk of the transaction. A “cheap” loan in 2026 isn’t just about the initial interest rate; it must also involve a total repayable amount that remains manageable. The Financial Conduct Authority (FCA) ensures that lenders act ethically by requiring strict affordability assessments. This prevents you from entering a cycle of debt that you cannot service, ensuring that any assistance provided is actually helpful rather than a burden.The Role of Representative APR in Your Search

When you see a “Representative APR” advertised, it is a legal requirement under UK regulations. It means that at least 51% of successful applicants must receive that specific rate or better. This prevents firms from advertising bait-and-switch deals. You should always look at the APR rather than just the interest rate, as the APR includes all mandatory lender fees. This gives you a more accurate picture of the total cost of your credit.Why Traditional Banks Say No Whilst Brokers Say Yes

High-street banks often operate on a binary scoring system. If you have a “thin” credit file with little history or a “damaged” profile from years ago, their computer systems often issue an automated rejection. Specialist lenders take a more inclusive approach. They look for reasons to say yes, often focusing on your current income rather than past mistakes. Whether you are seeking unsecured personal loans or a different product, a broker panel offers a much higher chance of success. If a bank has turned you down, you can get started with a search that values your current financial health over your credit score.Calculating the Real Cost: Interest Rates and Risk-Based Pricing

Lenders don’t just guess your interest rate. They use complex algorithms powered by data from credit reference agencies like Equifax and Experian to determine your level of risk. This process is known as “Risk-Based Pricing.” It explains why two people applying for the same low rate bad credit loans uk might receive vastly different offers. One person might get a manageable rate because they’ve shown stability recently, while another faces a higher APR due to recent missed payments or high debt levels. Your rate is a personal reflection of your financial story. Understanding how personal loans work in this context is essential for protecting your long-term budget. You must look beyond the monthly payment. A longer loan term might make your monthly bill feel smaller, but it often leads to a massive total interest cost over the life of the debt. For example, a £2,000 loan over five years will cost you significantly more in total interest than the same loan over two years, even if the five-year option feels “cheaper” each month. A “cheap” loan is only truly affordable if the total repayable amount doesn’t spiral out of control.Red Flags That Drive Up Your APR

Lenders look for specific markers that suggest you might struggle to repay. Recent County Court Judgments (CCJs), defaults, or high credit utilisation are major red flags that can push your APR into the triple digits. However, modern lenders are increasingly looking at your recent behaviour. If you’ve been stable for the last 12 months, this can begin to outweigh older financial mistakes. Before you apply, check your own credit report for errors. Even a small mistake in your address or a forgotten account can trigger a higher rate or an instant rejection.Identifying Hidden Fees and Total Repayable Amounts

The interest rate isn’t the only cost you’ll face. Many UK loans include origination fees, late payment penalties, or early exit charges if you want to pay the debt off sooner. Some “fee-free” options might actually be more expensive because the lender has hidden those costs in a slightly higher APR. Always demand to see the “Pre-contract Credit Information” document. This standardised form is required by law and gives you total transparency on the total amount you’ll pay back. It allows you to compare different low rate bad credit loans uk side-by-side without any guesswork. If you want to see what options are available for your specific situation without the stress of traditional bank hurdles, you can get started with a quick search today. It’s a fast, non-judgmental way to see where you stand.Secured vs. Unsecured: Finding the Cheapest Path to Funding

When you’re hunting for low rate bad credit loans uk, you’ll face a critical choice between secured and unsecured borrowing. The difference in cost is often substantial. Unsecured loans for poor credit typically carry higher interest rates, sometimes reaching 49.9% APR or more, because the lender has no safety net if you stop paying. In contrast, secured options use an asset to lower the lender’s risk. This simple shift in structure can unlock much lower rates and higher borrowing limits that would otherwise be out of reach. Security saves you money. By offering your property as collateral, you demonstrate a high level of commitment to the debt. If you have equity in your home, homeowner loans provide a pathway to funding that bypasses the rigid restrictions of high-street banks. These products are designed for those with complex financial histories who still need significant capital. You must consider the weight of this decision carefully. Your home may be repossessed if you do not keep up repayments. It is a powerful tool for lowering your interest costs, but it requires a disciplined approach to your monthly budget.When an Unsecured Personal Loan is the Better Choice

Unsecured borrowing is often the best fit for smaller amounts, typically under £5,000. It is the ideal solution for renters or those who don’t want to risk their property. The primary advantage here is speed. You can apply for cash loans and often receive a non-judgmental decision within minutes. There are no legal fees or property valuations to slow you down. Whilst the interest rate might be higher than a secured product, the lack of risk to your physical assets provides peace of mind for short-term financial needs.Consolidating Debt for Long-Term Savings

Many UK borrowers use secured products to merge multiple high-interest debts into one single, manageable monthly payment. This strategy can drastically reduce your total monthly outgoings and stop the cycle of high-interest traps. Secured loans offer the flexibility of longer repayment windows, which helps to spread the cost and lower your immediate financial pressure. Modern technology has made this process even more accessible. Read our guide on open banking loans to see how real-time data sharing can help you prove your affordability and secure a low rate bad credit loans uk even if your traditional credit score is low. Take the step toward a more tranquil financial future today.5 Strategic Steps to Optimise Your Loan Rate in 2026

You now understand that risk-based pricing is the engine behind your interest rate. To get the best deal, you must actively prove you are a lower risk than your credit score suggests. Optimising your profile is the most effective way to secure low rate bad credit loans uk in today’s digital market. It is about presenting the most stable version of your finances to a panel of lenders who are ready to listen. Follow these five strategic steps to strengthen your application and lower your costs.- Step 1: Use a broker for a soft search. This is your most powerful tool. It allows you to see real offers from a wide panel of lenders without leaving a single mark on your credit file. You get to compare rates in a risk-free environment.

- Step 2: Check your Electoral Roll status. Being registered at your current UK address is the quickest way to verify your identity. Lenders view this as a sign of stability and it can instantly improve your internal risk score.

- Step 3: Settle small, outstanding balances. Clearing even minor debts can significantly improve your debt-to-income ratio. Even paying off a small £50 balance shows you are in control of your monthly outgoings.

- Step 4: Opt-in for Open Banking. Sharing real-time data allows lenders to see your actual affordability today. This bypasses the limitations of older financial mistakes and proves you have the disposable income to handle a new loan.

- Step 5: Ensure total accuracy. Double-check every digit of your income and outgoings. A single typo or a rounded-up salary figure can trigger a fraud flag or lead to an automated rejection.

Leveraging Open Banking for Lower APRs

Open Banking is the primary rate-lowerer for sub-prime borrowers in 2026. By sharing your encrypted transaction data, you bypass the limitations of a stagnant credit score. Lenders use this information to identify your “disposable income,” which is the money you have left after essential bills. This transparency gives providers the confidence to offer more competitive rates because they can see you can comfortably afford the repayments. It is a secure, FCA-regulated process that empowers you to use your own data as leverage to find low rate bad credit loans uk.Document Preparation for a Faster Decision

Speed is essential when a good rate is on the table. Have your documents ready before you click apply. You will need your recent UK bank statements from the last three months, proof of your current address, and your most recent payslips. Readiness prevents your offer from expiring whilst a lender waits for information. Using digital PDF statements instead of scanned paper copies will significantly speed up the verification process. This ensures you lock in the best possible terms before the lender’s criteria change. If you’re ready to see what’s possible for your budget without any risk to your credit file, get started with a soft search now. It’s the first step toward a more affordable loan and a tranquil financial future.The Broker Advantage: Why a Panel Search Beats a Single Application

Applying directly to a single lender is like walking into a shop that only sells one brand. If they don’t have what you need, you’re out of luck. When you’re searching for low rate bad credit loans uk, this limitation can be costly. I Need Cash changes the game by searching an extensive panel of lenders with one single, simple application. Instead of hoping you fit one lender’s narrow criteria, we bring the market to you. This ensures you find the most competitive deal available for your specific financial situation without the need for repetitive forms. Our “No Judgment” philosophy is at the heart of everything we do. We understand that life happens. Past defaults or CCJs shouldn’t stop you from accessing affordable credit today. By comparing multiple offers side-by-side, you can identify the actual lowest rate rather than just accepting the first “yes” you receive. This transparency allows you to see the total cost of credit upfront. Best of all, this service is completely free for you as an applicant. There are no hidden broker fees or surprise charges. We work on your behalf to find the most transparent and cost-effective path to funding.Protecting Your Credit File Whilst You Shop

Every time you apply directly to a lender, they usually perform a “hard search” on your credit record. If you do this multiple times in a short window, it creates a cluster of searches. This can look like financial desperation to other banks and may actually lower your score. We act as a protective shield for your financial reputation. Our platform uses soft search technology to fetch your quotes. These are visible only to you and leave no public footprint on your financial record. You can shop with confidence, knowing your credit score is safe whilst you explore your options for low rate bad credit loans uk.Take the First Step Towards Financial Tranquility

A better financial future isn’t just a dream. It’s a realistic goal when you have the right ally by your side. We’ve designed our application process to be rapid, mobile-friendly, and stress-free. Most users receive a decision within minutes, allowing you to move from a state of anxiety to a feeling of empowerment. Whether you need to consolidate debt or cover an emergency, we’re here to help you find a solution that fits your life. Don’t let a poor credit history hold you back any longer. You can get started right now to see your personalised loan options and reclaim your financial autonomy.Secure Your Financial Future and Lower Your Costs

You’ve seen that a poor credit history doesn’t have to mean falling into high-interest traps. By leveraging modern tools like Open Banking and choosing the right borrowing path, you can unlock much more competitive terms. Whether you opt for a secured homeowner loan or a fast unsecured option, the secret is comparing multiple offers to find the perfect fit for your monthly budget. Accessing low rate bad credit loans uk in 2026 is about using your current financial stability as leverage to get the respect you deserve. Don’t let past mistakes dictate your peace of mind or limit your choices. As an FCA Authorised and Regulated Broker, we provide immediate access to a diverse panel of UK lenders who value transparency over traditional formalities. You can explore your personalised options right now with absolutely no impact on your credit score for an initial quote. It’s time to reclaim your financial autonomy and move toward a state of tranquility with a partner who works on your behalf. Check your eligibility for a cheap personal loan today. We are ready to help you find the right assistance whenever you need it.Frequently Asked Questions

Can I get a personal loan with very bad credit and no guarantor?

Yes, you can secure a personal loan without a guarantor even if your credit history is poor. Specialist lenders in 2026 use Open Banking to assess your real-time disposable income instead of relying solely on old credit scores. This technology allows them to offer low rate bad credit loans uk based on what you can actually afford today. It’s about your current financial behaviour, not just your past mistakes.How much can I borrow with a bad credit loan in the UK?

You can typically borrow between £100 and £5,000 for unsecured personal loans. If you are a homeowner with equity, you might access much larger amounts, sometimes exceeding £100,000 depending on the value of your property. The specific limit depends on your income, current debt levels, and whether you use an asset as security. Always choose an amount that fits comfortably within your monthly budget to ensure tranquility.Will applying for a cheap bad credit loan hurt my credit score?

Checking your eligibility through a broker won’t hurt your credit score because we use soft search technology. This type of search is invisible to other lenders and doesn’t leave a public footprint on your record. A hard search only occurs if you decide to proceed with a full, formal application. This protective layer allows you to shop for the best rates without any risk to your financial reputation.What is the maximum APR for bad credit loans in the UK?

The FCA caps interest on high-cost short-term credit at 0.8% per day, but standard personal loans don’t have a specific legal APR ceiling. You might see representative APRs ranging from 21.8% to 99.9% depending on the lender and your risk profile. Finding low rate bad credit loans uk involves comparing these offers side-by-side to ensure you aren’t paying more than the industry average for your specific credit tier.How long does it take to receive the money after approval?

Many lenders can transfer funds to your bank account within minutes of final approval. For unsecured personal loans, the process is often fully automated and incredibly fast. Homeowner loans take longer because they require property valuations and legal checks. If you have your digital PDF documents ready, such as bank statements and payslips, you can significantly speed up the turnaround time for any loan type.Can I get a loan if I am currently unemployed or on benefits?

You can still apply for a loan if you are on benefits or currently unemployed, provided you have a steady source of income. Lenders need to see that you have enough money left over each month to cover the repayments after your essential costs. They will look at your bank statements to verify your financial stability. It’s about proving you can manage the debt responsibly in your current situation.Is a homeowner loan always cheaper than a personal loan for bad credit?

Homeowner loans are generally cheaper than unsecured personal loans because they carry less risk for the lender. By using your property as collateral, you can often secure a much lower APR and spread the cost over a longer period. However, you must remember the risk involved. Your home is at risk if you don’t keep up the repayments, so always weigh the lower rate against the potential impact on your assets.What happens if I cannot keep up with my loan repayments?

You should contact your lender immediately if you think you might miss a repayment. Most firms are required by the FCA to show forbearance and help you find a manageable solution. Missing payments will lead to late fees and will damage your credit score. If you have a secured loan, the lender could eventually take steps to repossess your property, so early communication is vital to protect your future.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whiz with a pair of scissors as she originally trained as a hairdresser.