Emergency Loans for People on Benefits UK: A Complete 2026 Guide

- May 11, 2026

- Remy Anderson

- Finance

Your benefits are a valid form of income, and being on them shouldn’t mean you’re locked out of financial support when an emergency strikes. You’re likely feeling the pressure of a sudden bill whilst worrying that your employment status will lead to an instant rejection. It’s stressful when you need cash today but feel confused about which benefits lenders actually accept. You deserve a straightforward way to find emergency loans for people on benefits uk without the fear of being judged.

We want to help you move from financial anxiety to total peace of mind. This 2026 guide reveals exactly how to access urgent funds, from interest-free government support to specialised broker-led loans. We’ll explore the new Crisis and Resilience Fund launched on 1 April 2026, explain how to claim up to £812 through Budgeting Loans, and show you how to compare commercial options safely. Discover how to get the cash you need with affordable repayment terms so you can stay in control on your terms.

Key Takeaways

- Learn why traditional banks often decline claims and how the specialist market views your benefits as a stable, valid source of income.

- Compare interest-free government support with private emergency loans for people on benefits uk to find the fastest route to cash.

- Understand the “affordability first” rule that focuses on what you can comfortably repay rather than just your employment status.

- Get the step-by-step checklist for gathering award letters to ensure a smooth, non-judgmental application process today.

- Discover how a diverse panel of lenders can provide quotes in minutes without affecting your credit score, keeping you in control.

What Are Emergency Loans for People on Benefits?

Emergency loans for people on benefits uk are short-term credit products designed specifically for individuals whose main income comes from state support rather than traditional employment. Many high-street banks automatically decline applicants who aren’t in full-time work. This happens because their rigid systems often fail to recognise benefits as a stable form of income. The specialist market for emergency loans for people on benefits uk is different. It focuses on your total household income to see if a loan is affordable for your current budget. Emergency loans for benefits act as a financial safety net for non-standard income earners, providing a bridge during unexpected crises.

Lenders in this space are strictly regulated by the Financial Conduct Authority (FCA). This ensures they have a legal duty to treat you fairly and protect you from taking on debt that isn’t manageable. This modern regulatory framework is a significant evolution from the original UK Social Fund, which was the primary source of government crisis support for decades. While the government still provides certain interest-free advances, commercial lenders offer a faster and more flexible alternative for those who need cash today but don’t meet the DWP’s restrictive six-month eligibility rules.

Common Situations Requiring Urgent Cash

Life doesn’t wait for your next payment date. We often help people who are facing sudden financial shocks that require an immediate response. Common reasons for seeking urgent funds include:

- Essential home repairs: Fixing a broken boiler or a leaking roof amongst rising utility costs.

- Emergency travel: Covering costs for family emergencies or urgent medical appointments that can’t be delayed.

- The “five-week wait”: Bridging the gap during the initial wait for Universal Credit payments.

Whilst government advances exist for some, they aren’t always accessible or enough to cover every essential. In these moments, having access to a quick choice is vital to maintain your household’s stability.

The “I Need Cash” Ethic: Support Without Judgement

We believe everyone deserves access to financial fluidity, regardless of their employment status. Our approach prioritises your current ability to pay over mistakes you might have made years ago. Your credit history is only one part of the story; we care about your future. By working with a wide and varied panel of lenders, we help you find a cash loan quote that fits your specific budget. It’s about being in control on your own terms. We don’t act as a gatekeeper. Instead, we act as a financial ally to help you find the right path forward without the stress of a judgmental application process.

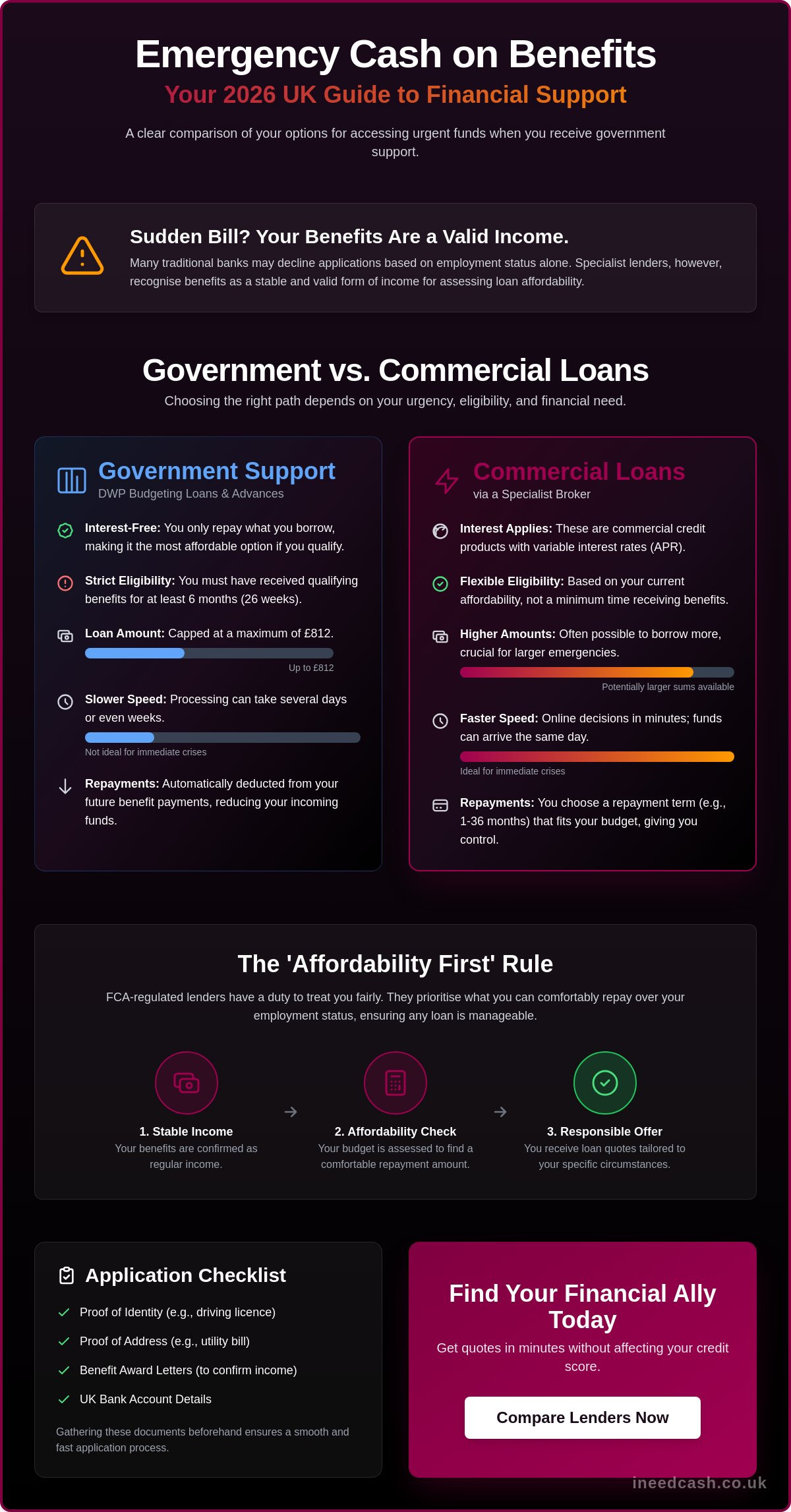

Budgeting Loans vs. Commercial Emergency Loans

Choosing between a government loan and a private lender is a balance of cost versus speed. You generally have two main routes when searching for emergency loans for people on benefits uk: interest-free government support or flexible commercial lending. Whilst government Budgeting Loans provide an interest-free solution for those who can wait, broker-led commercial options offer the rapid speed and flexibility needed for immediate crises. Understanding which one fits your timeline is the first step to regaining control of your finances.

Government Budgeting Advances and Loans

The Department for Work and Pensions (DWP) offers Budgeting Loans to those on legacy benefits like Income Support or Jobseeker’s Allowance. If you’re on Universal Credit, you’ll apply for a Budgeting Advance instead. These are interest-free, meaning you only pay back the principal amount. However, the 6-month rule is a major hurdle. You must have been receiving qualifying benefits for at least 26 weeks to even apply. If your emergency happens in month five, the government system often can’t help you. Additionally, DWP processing times can take several days or even weeks, which doesn’t work when a pipe has burst or your car has broken down today.

Repayments for government loans are automatically deducted from your future benefit payments. While this ensures you never miss a payment, it can make your monthly budget feel incredibly tight for up to 104 weeks. This lack of control over your outgoings can be stressful for households already managing on a limited income.

When a Commercial Loan Makes Sense

Commercial loans offer a different kind of support that prioritises speed and choice. They allow you to borrow more than the standard £812 government cap, which is essential for larger home repairs or family emergencies. You also get to decide your own repayment term, typically between 1 and 36 months. This puts you back in the driving seat, allowing you to tailor your outgoings to what you can actually afford right now rather than having the DWP decide for you.

If you’ve been worried about rejection due to your credit history, remember that our panel of lenders focuses on your current situation. We work with specialists who provide bad credit loans by assessing your benefits as a stable and valid income stream. You aren’t just a credit score to us; you’re a person who needs an immediate solution. You can get started now and see your options in minutes. This combination of speed, accessibility, and choice is what makes commercial options a vital ally for those who need to act fast.

How Lenders Assess Benefit Income in the UK

Modern lenders don’t just tick a box for “employed” or “unemployed” anymore. They’ve evolved to understand that state support is a reliable, steady form of income. When you apply for emergency loans for people on benefits uk, our panel looks at your “residual income.” This is simply the cash you have left over after your essential bills and rent are paid. If your benefits cover your living costs and leave a surplus, you’re often seen as a responsible borrower. This focus on affordability rather than just a payslip is why many people find success with specialist lenders after being turned away by high-street banks.

If you’re currently on Universal Credit, you might have already considered a Universal Credit advance from the DWP. If that isn’t an option or you need more flexibility, commercial lenders will assess your UC award as a valid income stream. Having a part-time job alongside your benefits can also significantly boost your approval chances. It shows an extra layer of financial fluidity, making it easier for lenders to say “yes” to your request for urgent funds.

Accepted Benefit Types for Loan Applications

Not all benefits are viewed the same way by every lender. Disability benefits like Personal Independence Payment (PIP) and Disability Living Allowance (DLA) are often considered the “gold standard” for stability. Because these awards are typically granted for several years, they provide a guaranteed long-term income that lenders love to see. Child Benefit and Tax Credits also bolster your application by proving you have a consistent monthly inflow to cover household costs. Whilst Housing Benefit is usually accepted, lenders will weigh it directly against your rent to ensure your loan repayments won’t put your home at risk.

The Role of Credit Scores and Open Banking

A “bad” credit score isn’t the deal-breaker it used to be. Traditional credit reports often focus on mistakes from years ago, but open banking loans offer a much fairer, real-time view of your finances. By securely sharing your recent banking data, you show lenders how you manage your money today. It proves you’re in control on your terms, allowing them to base their decision on your current behaviour rather than an old score.

We believe in a risk-free approach to finding cash. That’s why we use a “Soft Search” process when you check your eligibility for emergency loans for people on benefits uk. You can see which lenders on our panel are ready to help without it affecting your credit score. It’s a non-judgmental way to explore your options, giving you the peace of mind to make the right choice for your family’s future. Start your application today and get a decision in minutes.

Step-by-Step Guide: Applying for a Loan on Benefits

Applying for emergency loans for people on benefits uk is a process that rewards precision. When you’re facing a financial crisis, it’s tempting to rush through an application to get the cash as quickly as possible. However, taking ten minutes to gather your details ensures a smoother journey and a faster decision. Lenders need to see the exact breakdown of your monthly income to make a responsible offer. Guessing your figures often triggers fraud alerts or leads to an instant decline. Keep your latest award letters close by to ensure every penny is accounted for correctly.

Choosing the right amount to borrow is just as important as the application itself. Don’t be tempted to take more than you actually need. With the average UK household debt sitting at £67,350 as of January 2026, it’s vital to keep your own borrowing manageable. Look closely at the representative example provided by the lender. This shows you the total amount repayable, including interest. Use this data to check if the monthly instalments fit comfortably within your budget after your rent and essentials are paid. Being in control on your terms means only taking on what you can afford to pay back.

Documentation You Will Need

You’ll need a few essentials to verify your status and speed up the process. Most lenders on our panel will ask for:

- Proof of Identity: A valid UK driving licence or passport to confirm your residency.

- Benefit Award Letters: Recent documents from the DWP or HMRC confirming your payment amounts.

- Bank Statements: Statements from the last 90 days showing your benefit deposits and regular outgoings.

- Address History: Details of where you’ve lived for the last three years.

Avoiding Common Application Pitfalls

One of the biggest mistakes is making multiple “hard” applications to different lenders in a short window. This can damage your credit score and signal financial distress to future lenders. We avoid this by using a soft search that protects your rating whilst finding you a match amongst our varied panel. It’s also vital to stay away from unregulated lenders or “loan sharks” who don’t follow FCA rules. Instead, use a regulated payday loan responsibly as a short-term bridge for genuine emergencies. If you have all your documents ready, you can get started with a quote today and see your options in minutes.

Finding Your Financial Ally with I Need Cash

Approaching a single bank often leads to a “computer says no” response because of rigid criteria. At I Need Cash, we act as your financial ally. We don’t judge your situation or your income source. Instead, we use our wide varied panel of lenders to find a solution that works for you. When you search for emergency loans for people on benefits uk through us, you aren’t just applying for credit; you’re accessing a network of specialists who understand the 2026 financial climate. With total UK personal debt reaching £1,946.3 billion in January 2026, we know that many households need a supportive hand to manage sudden shocks.

Speed is our signature. We organise our search to deliver results in minutes because we know emergencies won’t wait. Our system filters through dozens of options to highlight the most sympathetic lenders for your specific circumstances. We operate with the “I Need Cash ethic,” which means total transparency. Every lender on our panel is FCA-regulated, ensuring you are protected by the highest standards of lending practice. You stay in control on your terms throughout the entire journey.

The Benefits of Using a Broker

Using a broker puts the power back in your hands. It simplifies a complex market into a single, easy-to-use tool. The advantages of choosing a broker-led approach include:

- One application, multiple choices: You don’t need to fill out dozens of forms. One simple process connects you to a varied panel of lenders today.

- Benefit-friendly filtering: We automatically remove lenders who don’t accept state support, saving you time and preventing unnecessary rejections.

- No-risk quotes: Checking your eligibility won’t affect your credit score, allowing you to explore your options with total peace of mind.

Our service is free for you to use. We believe that accessing emergency loans for people on benefits uk should be straightforward and stress-free. By matching you with the right lender the first time, we help you avoid the pitfalls of multiple hard credit searches that can damage your financial standing.

Next Steps: Get Started Today

Taking the first step is simple. Use our online tool to provide your basic details and the amount you need. Once you’ve submitted your information, our matching service works instantly to find the best fit from our panel. If you’re matched with a lender, you’ll be able to review their offer, including the repayment terms and the APR, before making a final decision. There’s no pressure and no hidden fees. Ready to take control? Apply for an emergency loan quote now and get the support you deserve today.

Take Control of Your Financial Future Today

You’ve discovered how to navigate the 2026 financial landscape with confidence. From the multi-year Crisis and Resilience Fund to specialised commercial options, you now know that your employment status isn’t a barrier to support. By focusing on your residual income and using modern tools like Open Banking, you can prove your affordability and secure the funds you need. Accessing emergency loans for people on benefits uk is about finding the right fit for your unique budget and timeline.

We want to help you move from anxiety to empowerment. As an FCA Authorised and Regulated broker, we provide a safe and transparent path to financial fluidity. Our quotes won’t affect your credit score, giving you the freedom to explore our wide panel of UK lenders without any risk. You deserve a non-judgmental service that puts your needs first and helps you stay in control on your terms.

Get started with your emergency loan application today. Don’t let an unexpected expense derail your week. Take the first step toward peace of mind and get a decision in minutes. You’ve got this, and we’re here to help.

Frequently Asked Questions

Can I get an emergency loan if I am on Universal Credit?

Yes, you have several options if you receive Universal Credit. You can apply for a Budgeting Advance from the DWP if you’ve been a claimant for at least six months. If you don’t meet that specific timing rule, our panel of specialist lenders accepts Universal Credit as a valid income source. They focus on your current affordability to help you find emergency loans for people on benefits uk today.

Will applying for a loan affect my benefit payments?

Borrowing money does not reduce your monthly benefit award amount. It’s important to remember that if you choose a government Budgeting Loan, the DWP will automatically deduct repayments from your future payments. Commercial loans are different because you pay them back via Direct Debit from your bank account. This keeps your benefit award intact but requires you to manage your own monthly budget carefully.

How much can I borrow whilst on benefits?

Government Budgeting Loans are strictly capped at £812 for households with children as of May 2026. If you need a larger amount for a major repair or emergency, commercial lenders on our panel offer more flexibility. They calculate your limit based on your residual income after all your essential bills are paid. This ensures you only borrow what you can comfortably afford to repay each month.

Do I need a guarantor for an emergency loan?

Most of the short-term and bad credit loans available through our service do not require a guarantor. Lenders now use Open Banking technology to verify your income and spending habits in real time. This modern approach allows them to make a fair decision based on your own financial behaviour. You can get a quote without needing to ask a friend or family member to back your application.

What is the fastest way to get cash if the DWP rejects my Budgeting Loan?

Using a specialist broker is often the quickest way to find an alternative. Whilst government decisions can take several days, our matching service provides quotes for emergency loans for people on benefits uk in minutes. Once you’re approved by a lender on our panel, funds are often transferred to your bank account within one hour. This speed is vital when you’re facing an immediate financial crisis.

Are there interest-free loans available for people on benefits?

Yes, the DWP Budgeting Loan and Budgeting Advance are both 0% interest options. You should also check the Crisis and Resilience Fund, which launched on 1 April 2026 to provide local support for essential living costs. These should always be your first port of call. Commercial loans do charge interest, so they are best used when you don’t qualify for government help or need funds more urgently.

What happens if I cannot repay my loan on time?

You must contact your lender immediately if you think you’ll miss a payment. FCA-regulated lenders have a legal duty to treat you fairly and may offer a temporary breathing space or a revised repayment plan. Missing payments without communication can lead to late fees and damage your credit score. If your total debt feels unmanageable, seek free, confidential advice from organisations like MoneyHelper or Citizens Advice.

Can I get a loan for a car whilst on benefits?

Yes, you can access specialist car finance even if your primary income is from benefits. Lenders often view stable awards like Personal Independence Payment (PIP) or Disability Living Allowance (DLA) very favourably. They treat these as guaranteed long-term income, which helps you secure the transport you need for family or work commitments. We can help you find a quote that fits your specific monthly budget.

Article by

Mandy Paige

Social Content Writer and Blogger

Mandy has been writing for various website for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it lead her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a wiz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.