Different Types of Car Finance Explained: A UK Guide for 2026

- May 20, 2026

- Remy Anderson

- Car Finance Finance

With the average car finance compensation payout hitting £829 this year, are you certain your next agreement is actually built for your benefit? It is easy to feel overwhelmed when you are staring at a screen full of confusing acronyms like PCP and HP. You want to get on the road quickly, but the fear of hidden balloon payments or a rejection due to your credit score can make the whole process feel like a minefield. We understand that financial anxiety. Compare the different types of car finance available in the UK today without the jargon or the judgement.

We agree that finding the right deal should feel empowering, not exhausting. This guide promises to strip away the complexity and give you total clarity on your monthly costs. We will help you break down every option from Hire Purchase to personal loans, which currently offer stable rates between 6.2% and 8.5% APR as of May 2026. Discover exactly how each choice impacts your wallet and gain the confidence to pick the perfect plan for your budget. Stop worrying about the fine print and start focusing on the drive. Let’s get you moving.

Key Takeaways

- Master the basics of spreading vehicle costs so you can drive away today without draining your savings.

- Compare the different types of car finance to decide whether you prefer the full ownership of Hire Purchase or the lower monthly costs of PCP.

- Identify how small adjustments to your deposit and mileage estimates can significantly reduce your overall interest payments.

- Uncover how Open Banking technology is opening doors for drivers with bad credit or limited financial history to secure a rapid approval.

- Learn how to leverage a vast network of providers to find an ideal deal and strengthen your bargaining power at the dealership.

Understanding the Different Types of Car Finance in the UK

Stop waiting for the “perfect time” to save up thousands for a new vehicle. You need to get on the road now. Whether it is for a new job, a growing family, or simply the freedom to travel, your mobility shouldn’t be held back by a lack of upfront cash. Car finance is a straightforward credit agreement that allows you to spread the cost of a vehicle into manageable monthly chunks whilst you drive it today. It is the most popular way for British drivers to get behind the wheel. Most people prefer keeping their hard-earned savings for life’s emergencies rather than handing over a massive lump sum at a dealership. Exploring the different types of car finance is the first step toward reclaiming your financial autonomy. You are in the driving seat. Choosing a finance plan is not just about the car; it is about finding terms that fit your life and your unique budget. We believe in providing a supportive, non-judgmental path to vehicle ownership. You deserve a solution that works for you, regardless of your past financial hurdles. By understanding your options, you move from a place of anxiety to a position of total control.The difference between owning and hiring

Decide what happens when the agreement ends. Ownership-focused finance means the car is yours once you make the final payment. It is a simple, transparent route to long-term asset ownership. Hire-focused finance, often called leasing, allows you to drive the latest models with lower monthly costs. You are essentially paying for the car’s depreciation rather than its total value. Your future plans should dictate your choice today. If you want a car to keep for a decade, aim for ownership. If you prefer upgrading to a new model every few years, hiring might be your best bet. Both are valid paths amongst the different types of car finance available.Why spread the cost of your vehicle?

Protect your cash flow. Spreading the cost ensures you have money left for other essentials like rent, groceries, and bills. It also gives you access to better, safer, and more fuel-efficient vehicles than you could likely afford to buy outright. A newer car often means lower maintenance costs and higher reliability. Additionally, making regular, on-time payments is a practical way to demonstrate responsible financial behaviour. This can help strengthen your financial standing over time. If you are ready to see how we can help you get moving, check out our tailored options for car finance today. We focus on speed and flexibility to get you on the road fast.Comparing the Four Main Car Finance Options

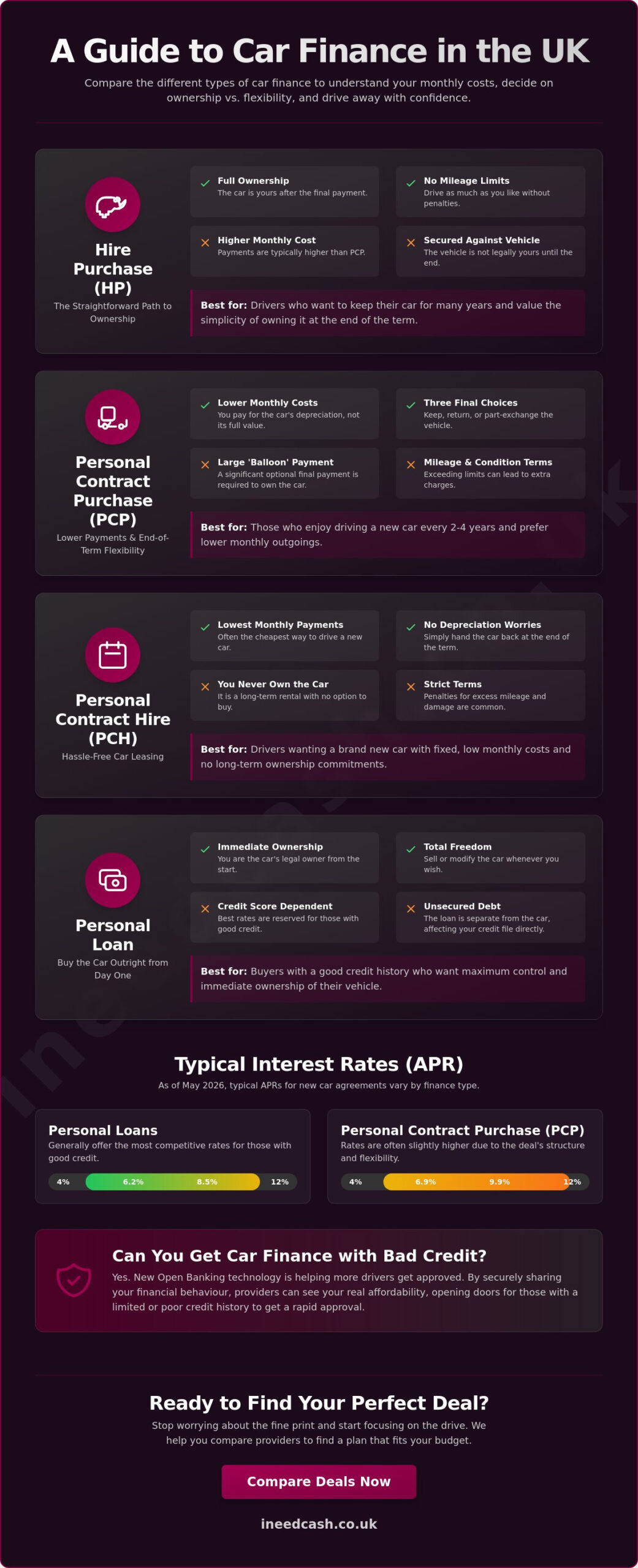

Securing the right deal means matching the agreement to your lifestyle. You shouldn’t settle for the first offer a dealer hands you. Amongst the different types of car finance, four main paths dominate the UK market. Each has distinct advantages depending on whether you value low monthly outgoings, total flexibility, or long-term ownership. Understanding these nuances helps you avoid the stress of hidden costs and puts you back in control of your financial future.- Hire Purchase (HP): A simple, transparent path where you pay a deposit and monthly instalments until you own the car outright.

- Personal Contract Purchase (PCP): Offers lower monthly payments by deferring a large “balloon” payment to the end of the term.

- Personal Contract Hire (PCH): A long-term rental agreement where you drive a new car for a fixed period and then hand it back.

- Personal Loans: You borrow the cash to buy the car upfront, making you the legal owner from the very first day.

Hire Purchase (HP) vs Personal Contract Purchase (PCP)

Hire Purchase is the most straightforward route to ownership. You won’t face mileage limits or extra charges for minor wear and tear because the goal is for you to keep the vehicle. It is ideal if you plan to drive the car for many years and want to avoid a large final bill. Conversely, PCP is built for flexibility. You pay for the car’s depreciation rather than its full value, which keeps your monthly budget manageable. As of May 2026, PCP interest rates for new cars typically range between 6.9% and 9.9% APR. At the end of the contract, you decide whether to pay the balloon payment to keep the car, swap it for a newer model, or simply walk away. This choice empowers you to adapt as your circumstances change.Personal Loans and Leasing (PCH)

Choosing an unsecured personal loan gives you total freedom. Because you own the car immediately, you can sell it or modify it whenever you like without asking a finance company for permission. Interest rates for these loans are currently stable, sitting between 6.2% and 8.5% APR. If you prefer the “new car smell” every few years without the intention of ever owning the vehicle, PCH is your best bet. It often includes maintenance packages, though you must stick to strict mileage limits to avoid penalties. Evaluating these different types of car finance allows you to pick a plan that protects your cash flow whilst getting you on the road quickly.Choosing the Right Finance Type for Your Budget

Stop guessing about your monthly outgoings. You need a plan that secures your lifestyle without draining your bank account. When you weigh up the different types of car finance, your daily habits matter more than the badge on the bonnet. Your annual mileage is the biggest factor. High-mileage drivers often find that PCP or PCH agreements become prohibitively expensive due to steep penalties for exceeding agreed limits. If you are doing 15,000 miles a year for work, a different path is essential to keep your costs manageable. Evaluate your deposit carefully. A larger upfront payment isn’t just about showing off; it’s a strategic move to slash your total interest. By paying more now, you lower the monthly burden on your future self. For those planning to keep a vehicle for seven years or more, the “long-haul” options like Hire Purchase or a Personal Loan are usually the most cost-effective. You avoid the cycle of endless interest and eventually reach the tranquility of zero monthly car payments. Flexibility also matters. If you anticipate your family growing or your job changing, you need the option to swap vehicles without facing massive exit fees.The “Frequent Upgrader” vs the “Long-Term Owner”

PCP remains the UK’s favourite for a reason. It is perfect for people who want to change their car every three years to stay under warranty and enjoy the latest tech. You pay for the use of the car, not the whole thing. However, if you want to eliminate monthly payments entirely, HP is the solid choice. It requires a bit more commitment each month, but the finish line is clear. You must balance the excitement of a new number plate with the reality of long-term interest costs. Comparing different types of car finance requires a clear-eyed look at your long-term goals rather than just the immediate thrill of a new drive.Hidden costs to look out for

Understanding APR is vital, but the lowest rate isn’t always the best deal. Some agreements hide administration fees or “option to purchase” charges that inflate the total cost. Always check the total amount payable, not just the headline interest rate. Mileage limits are another trap. A simple change in your daily commute could result in a surprise bill of hundreds of pounds when you return a lease. Finally, keeping your car in good “nick” is essential for PCP and PCH. Lenders expect “Fair Wear and Tear,” but significant scuffs or stains will lead to damage recharges that can ruin your budget. Stay informed and stay in control.Can You Get Car Finance with Bad Credit?

Don’t let a low credit score stall your life. The non-judgmental truth is that your financial past does not have to dictate your future on the road. Many modern lenders now specialise in helping people with a wide range of credit histories. They understand that life happens. Whether you’ve had a missed payment or a CCJ in the past, there are still different types of car finance designed specifically to help you get moving again. You deserve a second chance and a supportive partner to help you find it. We are here to help you bridge the gap between where you are and where you want to be. Technology is making approvals faster and fairer. If you are a homeowner, you may have more options than you realise. Using homeowner loans can often unlock more competitive rates for funding a vehicle because the loan is secured against an asset you already own. This provides lenders with extra security, which they often reward with better terms. Crucially, you can now check your eligibility with many providers without any impact on your credit file. This lets you explore different types of car finance with total peace of mind and zero risk to your score.How lenders view your behaviour in 2026

Lenders have moved beyond the rigid “pass or fail” scores of the past. In 2026, the focus has shifted toward your current stability and immediate affordability. They want to see that you can comfortably manage the monthly instalments today, even if things were difficult five years ago. A steady income and recent responsible behaviour often carry more weight than an old mistake. By using open banking loans, providers get a secure, real-time view of your actual finances to make a faster and more accurate approval decision based on who you are now. This transparency builds trust and speeds up your journey to the dealership.Specialised options for “non-standard” applicants

If your file is particularly thin, guarantor car finance can be a game-changer. This involves a friend or family member with a stronger credit history backing your agreement, which significantly lowers the lender’s risk. Alternatively, bad credit loans can serve as a vital stepping stone. These agreements get you the vehicle you need today whilst giving you a chance to rebuild your credit profile through regular, on-time payments. To give your application the best possible boost, ensure you are on the electoral roll and try to reduce any small, lingering debts before you apply. These small steps show you are serious about your financial autonomy. Ready to see what is possible? Get your personalised quote today and take the first step toward your next car.How to Find Your Ideal Car Finance Deal Today

Stop wasting hours on comparison sites that don’t know your story. You need a fast route to the finish line. Using a credit broker like I Need Cash gives you an immediate advantage in a crowded market. We connect you to a wide panel of lenders, ensuring you see the different types of car finance that actually fit your specific circumstances. Speed is everything. Get a quote in minutes and head to the dealership with the confidence of a cash buyer. You maintain total autonomy throughout the process. You choose the deal that aligns with your monthly budget and lifestyle, rather than being forced into a corner by a single dealer’s limited offer. We believe in transparency and speed. By accessing a broad network, you bypass the gatekeepers of traditional banking. This approach empowers you to move from financial anxiety to a state of tranquility. You are no longer guessing what you can afford. You are walking into a transaction with a pre-approved plan that protects your interests. It is about putting you back in control of your journey.The benefit of a broker ally

We act as your supportive partner, not just another middleman. We work for you to find the most flexible terms available amongst the different types of car finance. This includes access to specialised “broker-only” deals that aren’t always visible on standard comparison sites. Our non-judgmental approach removes the stress from the application process. We are indifferent to past mistakes and focused on your current ability to pay. By leveraging our extensive network of providers, we ensure you aren’t just another number in a faceless database. We advocate for your approval.Ready to get on the road?

Preparation is your best tool for a rapid turnaround. Have your photo ID, proof of address, and recent payslips ready to go. Having these documents organised ensures your application moves through the system without any frustrating hitches. Getting a car finance quote before you even step onto a forecourt puts you in a much stronger negotiating position. You already know your limits, so you won’t be swayed by expensive dealer add-ons or confusing terminology. Take action today to secure your vehicle. Apply for a loan quote now and move one step closer to the driver’s seat. Your journey to a better car starts with a single, simple click.Take Control of Your Journey Today

You now have the clarity to move forward with total confidence. Navigating the different types of car finance doesn’t have to be a source of stress when you have the right information. You understand that whether you prioritised the long-term ownership of a personal loan or the lower monthly outgoings of a lease, the choice was entirely yours. Your personal autonomy is the most important part of this process. Past mistakes shouldn’t stop you from getting a reliable vehicle that fits your current life and budget. We are ready to act as your supportive partner in this transition. Our service is FCA Authorised and Regulated, giving you the security you need when making a big financial decision. We provide access to a wide panel of UK lenders through a quick, non-judgmental process that values your time and your unique circumstances. You can stop worrying about the fine print and start focusing on the freedom of the open road. Your next car is closer than you think. Find the car finance that fits your life—Get Started Now!Frequently Asked Questions

Which type of car finance is the cheapest overall?

Personal loans and Hire Purchase (HP) are generally the cheapest different types of car finance if your goal is long-term ownership. Whilst PCP offers lower monthly instalments, the total amount payable is usually higher because you are paying interest on the large deferred balloon payment throughout the term. Choosing HP means you pay off the car’s full value faster, reducing the total interest cost.Can I end my car finance agreement early if my circumstances change?

You can end your agreement early by requesting a settlement figure from your lender at any time. If you have already paid at least 50% of the total finance amount, including interest and fees, you may also have the legal right to a “Voluntary Termination.” This allows you to return the car and walk away without further monthly obligations, provided the vehicle is in good condition.Do I need to pay a deposit for car finance in the UK?

You don’t always need a deposit, as many lenders offer “no-deposit” car finance options to help you get on the road immediately. However, putting down even a small amount is a smart move. It reduces your monthly instalments and lowers the total interest you will pay over the life of the agreement, making the car more affordable in the long run.What happens at the end of a PCP agreement if I don’t want the car?

If you don’t want to keep the vehicle at the end of a PCP term, you can simply hand the keys back to the finance company. This is one of the most flexible features of this finance type. As long as you haven’t exceeded your agreed mileage limit and the car meets “Fair Wear and Tear” standards, you won’t have anything extra to pay.Can I get car finance if I am self-employed or have a fluctuating income?

Yes, being self-employed is not a barrier to securing a deal amongst the different types of car finance available today. Lenders now use Open Banking technology to verify your income directly through your bank statements. They focus on your actual affordability and recent financial stability rather than requiring years of perfect tax returns or traditional payslips.Is it better to get a personal loan or Hire Purchase for a used car?

A personal loan is often the better choice for a used car because interest rates are currently stable between 6.2% and 8.5% APR. Used car HP rates can be significantly higher, with some reaching up to 14.5% APR in May 2026. Using a loan also means you own the vehicle outright from day one, giving you more freedom to sell it later.Will applying for car finance affect my credit score?

Initial eligibility checks use a “soft search” which has zero impact on your credit records or your ability to get future credit. A “hard search” only occurs when you move forward with a full application. This might cause a small, temporary dip in your score, but making regular, on-time payments will help rebuild your credit profile quickly.What is a balloon payment and how do I prepare for it?

A balloon payment is the final, large lump sum required to take full ownership of a car at the end of a PCP agreement. You can prepare for it by setting aside a monthly savings pot or by planning to refinance the balance through a personal loan. Alternatively, many drivers choose to trade the car in and use any equity as a deposit.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.