Loan Broker vs Direct Lender UK: Which is Better for Your Borrowing in 2026?

- May 21, 2026

- Remy Anderson

- Finance

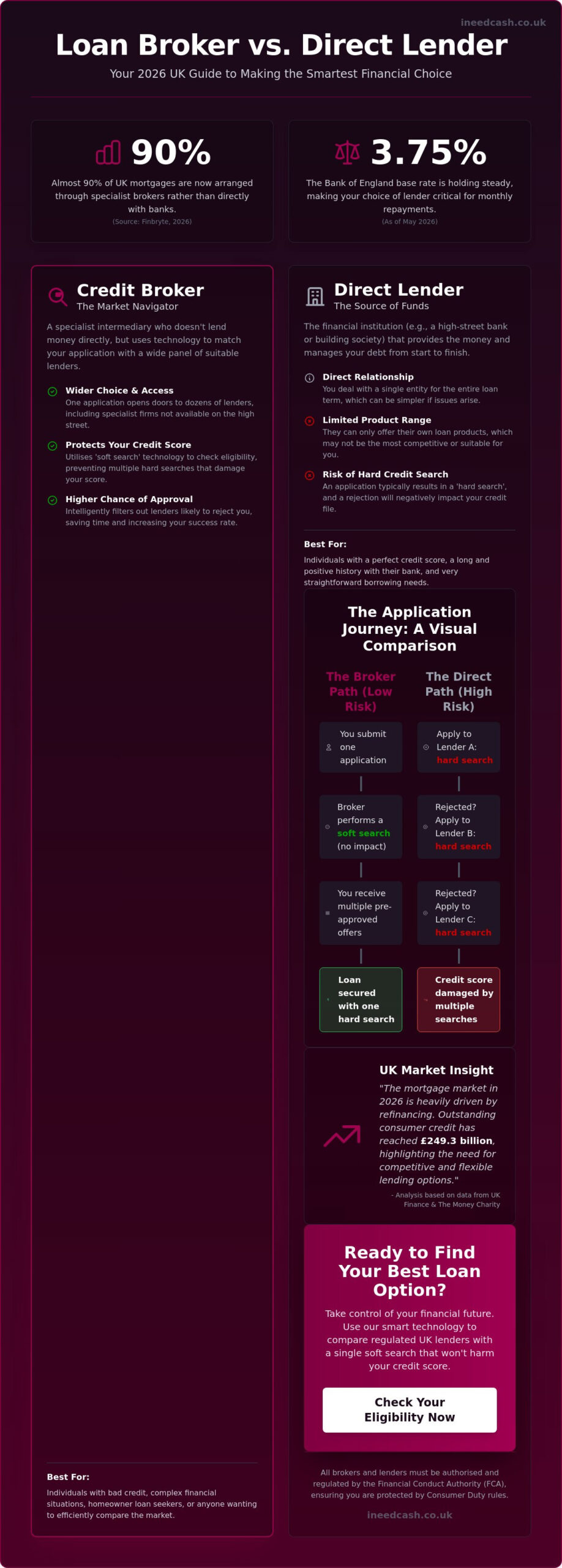

Did you know that almost 90% of UK mortgages are now arranged through intermediaries rather than directly with banks? (Source: Finbryte, January 2026). With the Bank of England base rate holding at 3.75% as of May 2026, the stakes for your monthly budget are high. You’re likely weighing up the loan broker vs direct lender uk options whilst feeling the stress of a potential rejection. Avoid hidden fees and check your eligibility without worrying about a negative impact on your financial records.

Outstanding consumer credit reached £249.3 billion this year, according to The Money Charity. “The mortgage market in 2026 is heavily driven by refinancing,” notes the trade association UK Finance. This guide provides the assistance you need to secure the best possible APR, with personal loan rates currently starting from 5.7%. Discover how to boost your approval chances for homeowner loans or personal loans whilst maintaining your autonomy. Get a clear decision on which path empowers you to take control of your financial future and find the flexibility you deserve.

Key Takeaways

- Understand how a credit broker acts as a specialist intermediary to match you with multiple providers whilst a direct lender handles your debt personally.

- Discover why modern technology in 2026 allows brokers to offer rapid turnarounds and a wider variety of options for your immediate financial needs.

- Analyse the loan broker vs direct lender uk debate to find out why brokers are often the best choice for securing bad credit loans or homeowner loans.

- Identify when going straight to a bank makes sense for those with perfect credit scores and long-standing financial histories.

- Take autonomy over your application process to secure the best possible APR and avoid multiple credit searches that could damage your score.

Understanding the UK Lending Landscape: Brokers and Direct Lenders Explained

In May 2026, the Bank of England base rate sits at 3.75%. This stability is welcome, but finding the right deal remains a challenge. When you need cash, you face a fundamental choice: loan broker vs direct lender uk. Both entities must be authorised and regulated by the Financial Conduct Authority (FCA). This ensures you’re protected by the Consumer Duty rules. Whilst a direct lender is the source of the funds, a credit broker acts as your advocate in a crowded market.The Role of the Direct Lender

A direct lender is the company that actually puts the money into your bank account. They manage your debt from start to finish. High-street banks and building societies are the most common examples. They set their own criteria and interest rates based on their specific risk appetite. However, they only offer their own products. If you don’t meet their strict requirements, you’ll likely face a rejection that could hurt your credit score.The Role of the Credit Broker

A credit broker, such as I Need Cash, is a specialist intermediary. They don’t lend money themselves. Instead, they match you with a panel of various lenders. This “search once, see many” approach is vital in 2026’s volatile economy. You might wonder, What is a mortgage broker? or a loan broker? Essentially, they are non-judgmental facilitators. They use smart technology to find a match that fits your unique situation without you having to apply to dozens of different firms individually.Why Choice Matters Right Now

With outstanding consumer credit reaching £249.3 billion this year, having options is your best defence against high costs. A broker provides a safety net. They look across the market to find the most competitive rates for homeowner loans or personal loans. This empowers you to make an informed decision rather than settling for the first offer you see. It turns a stressful search into a managed, supportive process that respects your time and your financial autonomy.The Broker Advantage: Why Multiple Lenders Often Beat One

One application. Dozens of lenders. In 2026, speed is everything. You don’t have time to fill out fifty different forms or wait days for a response. A broker does the heavy lifting for you. They use advanced technology to scan the market in seconds. When you’re weighing up a loan broker vs direct lender uk, the power of choice is your greatest asset. It moves you from a state of uncertainty to a position of strength.Access to a Panel of Regulated Lenders

Many specialist lenders in the UK don’t deal with the public directly. They prefer to work through intermediaries who understand their specific criteria. This means a broker provides an “open door” to exclusive financial products you simply cannot find on the high street. Why use a mortgage broker or loan broker? The answer lies in this market access. We work on your behalf to find the right fit for your unique conditions.Protecting Your Credit Score

Rejection is painful, and every hard credit search leaves a mark on your record. This can create a downward spiral for your borrowing chances. Modern brokers solve this with soft search technology. “A broker can often provide a quote using a soft search, meaning your credit score remains untouched whilst you compare options.” This approach is frequently combined with Open Banking loans to provide an accurate, real-time view of your affordability without the risk.Filtered Results for Higher Success

Stop guessing which lenders will accept you. Brokers act as a filter. They automatically remove providers where your application is likely to be rejected. This saves you from unnecessary anxiety and keeps your financial record clean. It’s about personal autonomy and making the system work for you, not the other way around. If you want to see which lenders are ready to say yes, get started now and explore your personalised options in minutes.Direct Lending Realities: When Going Straight to the Source Makes Sense

Sometimes, the shortest path is the most appealing. If you have a flawless credit score and a decade-long relationship with a high-street bank, going direct might feel like the natural choice. Direct lenders provide a single point of contact for the entire life of your loan. There are no intermediaries. You deal with one entity from the first click to the final payment. This simplicity is a favourite for borrowers who value a traditional, linear relationship with their financial provider.Simplicity and Loyalty Rewards

When comparing a loan broker vs direct lender uk, it’s important to recognise that direct lenders often reward loyalty. If you already hold a current account, you might see “pre-approved” offers in your banking app. These can sometimes come with faster funding times because the bank already understands your income and spending behaviour. It’s a straight line to the cash you need, provided you fit their specific, often narrow, criteria. This approach offers autonomy to those with stable, predictable financial histories.The Single Application Process

Convenience is a powerful motivator. Tapping a button in your existing banking app feels effortless. However, this ease often comes with a hidden cost. By only looking at one provider, you never truly know if a more competitive rate exists elsewhere. It’s the “all your eggs in one basket” risk. Whilst it feels fast, a “computer says no” result from your own bank can feel like a dead end. You’re left with a rejection and no alternative plan to secure the funds you need.When Direct Lenders Might Fall Short

High-street banks usually have the strictest criteria in the UK market. If your circumstances are slightly complex or you’re seeking bad credit loans, a direct lender’s rigid rules might lead to an immediate rejection. Unlike a broker who scans multiple options, a direct lender only has one product range. A rejection here usually involves a hard credit search. This can lower your score and make future borrowing even harder. Choice provides a safety net that a single lender simply cannot match.Broker vs Direct Lender: The Comparison for Homeowners and Bad Credit

Deciding between a loan broker vs direct lender uk means choosing between a rigid algorithm and a human-centric approach. Whilst a bank uses a spreadsheet to judge your worth, a broker sees the individual behind the application. This distinction is vital for those with complex equity or recovering from past financial mistakes. You need a partner who prioritises your success over their own narrow lending rules and provides a clear path forward.The Homeowner Loan Perspective

Navigating homeowner loans requires a deep understanding of equity requirements. In 2026, competition for equity-based products is fierce. Brokers help you look beyond the strict criteria of traditional banks. They find lenders willing to consider your whole situation, including the actual value of your property. This gives you the autonomy to leverage your property’s value on your own terms without the fear of an automated rejection based solely on a credit score.Acceptance Rates for Bad Credit

Direct lenders often ignore “difficult” cases to minimise their risk. This leaves many borrowers feeling marginalised by the traditional system. Brokers specialise in these scenarios. They act as non-judgmental facilitators, connecting you with providers who value your current affordability. Remember: “Your past doesn’t define your financial future.” Brokers organise the search to favour lenders with high acceptance rates for your profile, protecting your credit score from unnecessary hard searches that could cause further damage.Transparency and Cost Efficiency

Many assume brokers always charge high fees. However, I Need Cash provides a free service to applicants. You get the benefit of a massive lender network without any upfront costs. This transparency helps move you from financial anxiety to tranquility. You deserve a stress-free process that respects your time and your situation. If you’re ready to see your highest approval chances, apply for a loan quote today and take back control of your finances.Making Your Choice: How to Get Started with Your Loan Application Today

Choosing between a loan broker vs direct lender uk comes down to your personal circumstances. If you have a high credit score and a strong bank history, direct lending offers simplicity. However, if you want to compare the wider market or have a complex financial history, a broker provides the necessary assistance. Take autonomy over your borrowing and don’t settle for the first offer. You deserve a solution tailored to your individualised conditions.Identifying Your Borrowing Needs

Decide if you need a short term loan for an emergency or a long-term homeowner solution. Before applying, check your credit report to understand your standing. This helps you target the right providers immediately. Always borrow responsibly and only what you can afford to repay. Planning your budget ensures you move from financial anxiety to tranquility whilst maintaining total control over your monthly outgoings.Getting Your Personalised Quote

Ready to find the best rate? Use our digital search tool to scan our panel of regulated lenders in seconds. This process is rapid, secure, and designed to put you in the driving seat. By using soft search technology, you can explore your options without any impact on your financial records. This risk-free approach allows you to see exactly what you qualify for before making a final commitment.Fast and Secure Approval

Our facilitator role ensures you aren’t just another number in an algorithm. We work on your behalf to find the highest approval chances for your profile. Once you have your quote, the next steps are straightforward and transparent. Get started with your loan quote now. Take the first step toward a stress-free application process today and secure the funds you need with confidence.Take Control of Your Financial Future Today

Choosing between a loan broker vs direct lender uk defines how much you pay and how likely you are to be accepted. You’ve seen that whilst direct lenders offer a linear relationship, brokers empower you with a market-wide map. This choice is vital in 2026 as interest rates and lending criteria continue to shift. By scanning a wide panel of UK lenders, you ensure you aren’t settling for the first offer but securing the most competitive terms for your unique profile. Our service is designed to be your supportive partner. We’re FCA Authorised and Regulated, specialising in homeowner and bad credit loans where traditional banks often fall short. We prioritise your autonomy by providing quotes using soft search technology. It keeps your credit score safe whilst you compare options. You deserve a facilitator that works on your behalf, not a gatekeeper that shuts doors. It’s time to move from financial anxiety to a state of tranquility. Find your perfect loan match today with our free search tool. Stop the cycle of stress and start your journey toward empowerment and peace of mind.Frequently Asked Questions

Is it better to use a broker or a direct lender for bad credit?

It is generally better to use a broker because they specialise in matching you with providers who accept lower credit scores. When weighing up a loan broker vs direct lender uk for bad credit, a broker acts as an advocate with a panel of specialist firms. Whilst a single bank might reject you immediately, a broker scans multiple options simultaneously to increase your approval chances.Do loan brokers in the UK charge a fee for their services?

Many brokers are free to use for applicants, including I Need Cash, as they receive a commission from the lender instead. However, some brokers may charge an upfront or success fee, so you should always check their Terms and Conditions. In 2026, transparency is a requirement under FCA Consumer Duty rules, so any fees must be clearly stated before you commit.Will applying through a broker like I Need Cash hurt my credit score?

No, initial applications through our platform use soft search technology which does not impact your credit score. This allows you to see your eligibility and potential rates across a panel of providers risk-free. A hard search only occurs later in the process if you decide to proceed with a specific lender’s offer and submit a full application that requires a final credit check.Can I get a loan faster by going directly to a lender?

Not necessarily, as modern brokerage technology in 2026 allows for rapid turnarounds that often match or exceed direct applications. Whilst your own bank might fund you quickly if you are already an account holder, a broker can identify which specialist lenders are currently offering the fastest processing times for your specific profile. This saves you from waiting on a slow provider.How do I know if a loan broker is legitimate and regulated?

You can verify any firm by checking the Financial Services Register on the FCA website. Every legitimate broker and lender in the UK must be authorised and regulated by the Financial Conduct Authority. This regulation ensures they follow strict codes of conduct and provides you with access to the Financial Ombudsman Service if you need assistance with a dispute.What is the main difference between a homeowner loan and a personal loan?

The main difference is that a homeowner loan is secured against your property, whilst a personal loan is unsecured. Because you are using your home as security, homeowner loans often allow you to borrow larger amounts over longer terms with potentially lower interest rates. However, your home may be at risk if you don’t keep up repayments, so you must borrow responsibly.Can a broker help me find a loan if I have been rejected by my bank?

Yes, brokers are often the best solution after a bank rejection because they have access to a much wider variety of lending criteria. High-street banks have become increasingly rigid in 2026. A broker looks beyond a simple credit score to find lenders who consider your current affordability and specific needs, turning a frustrating “no” from your bank into a potential “yes.”What information do I need to provide when applying through a broker?

You typically need to provide basic personal details, your address history for the last three years, and information about your income and monthly outgoings. Providing accurate data helps the broker match you with the right provider quickly. In the loan broker vs direct lender uk comparison, brokers often use Open Banking to verify this information instantly, making the entire process much smoother and more secure.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.