Loans for Single Parents on Benefits UK: Your 2026 Financial Guide

- June 8, 2026

- Remy Anderson

- Bad Credit Finance

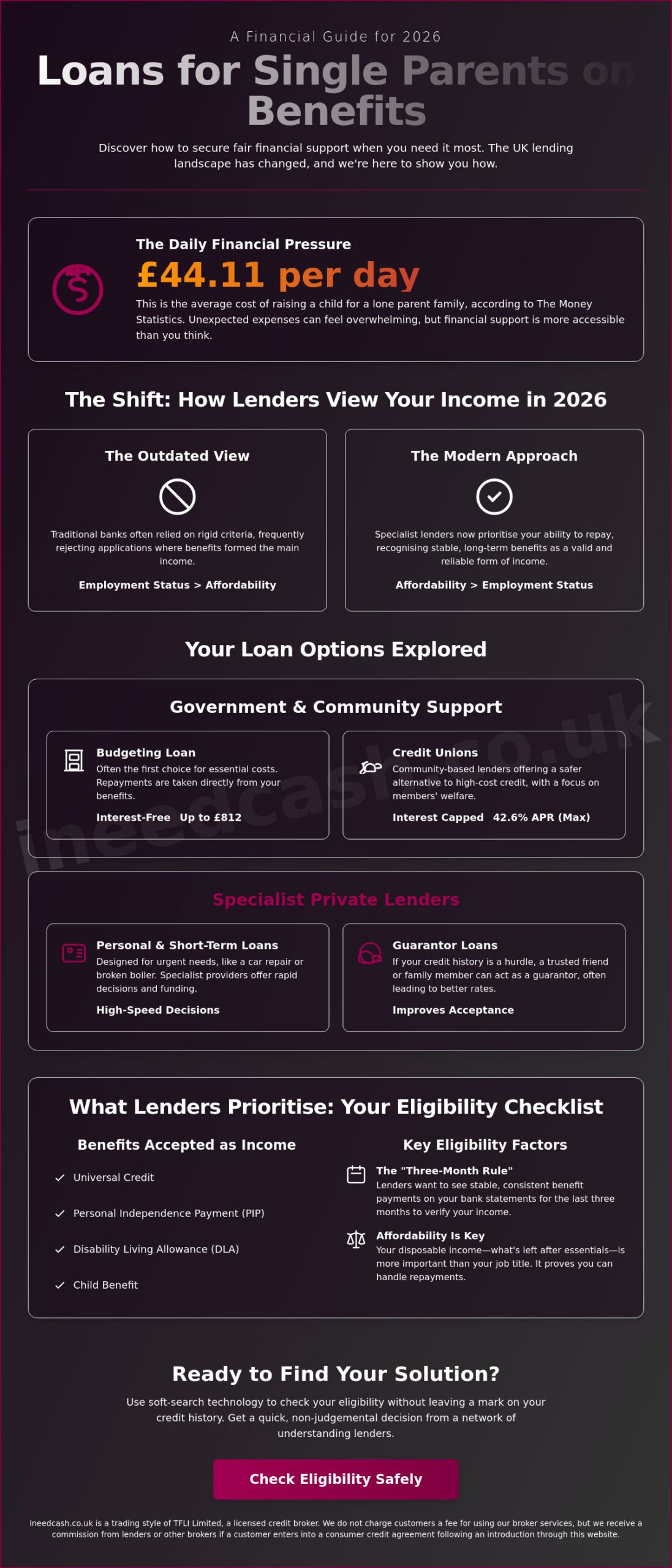

Did you know that by early 2026, the average cost of raising a child for a lone parent family reached £44.11 per day? This data from The Money Statistics highlights the immense pressure on your monthly budget. When an emergency strikes, finding loans for single parents on benefits in the UK can feel hard. You may worry that your job status makes you unseen by traditional banks.

Or you may be unsure which benefits count as valid income.

We believe your family deserves stability, regardless of your circumstances. Discover fair financial support as a single parent on benefits. Use our simple guide to UK loan options and eligibility.

We’ll move you from anxiety to tranquility by showing you exactly which lenders value your autonomy. This guide covers everything from interest-free Budgeting Advances to specialist providers.

They recognise Universal Credit as a stable income stream. It’s time to find a supportive partner who looks past your credit file and prioritises your family’s future.

Key Takeaways

- Discover how the 2026 lending market now treats benefits as valid income, opening doors for single parents previously rejected by high-street banks.

- Compare interest-free government options with private sector loans for single parents on benefits uk to find the most cost-effective solution for your family.

- Learn about the “Three-Month Rule” and how maintaining stable benefit payments on your bank statements can significantly boost your application success.

- Protect your financial record by using soft-search technology that allows you to check eligibility without leaving a visible mark on your credit history.

- Save time and reduce stress by accessing a wide network of non-judgemental lenders through a single application process designed for rapid results.

Table of Contents

Can You Get a Loan as a Single Parent on Benefits?

Yes. The short answer is a definitive yes. The UK lending landscape in 2026 has changed. You cant get single parent loans in the UK.

Lenders now focus on affordability first.

This affects loan models for single parents on benefits in the UK.

Gone are the days when a lack of traditional full-time employment meant an automatic rejection. Today, many specialist providers recognise that stable, long-term benefits are a reliable form of income. They look at the money coming in, not just the name of the organisation paying it.

Overcoming the "Poverty Premium"

Life as a lone parent is expensive. Research from Gingerbread shows that single parents often face a “poverty premium.”

They may pay more for everyday essentials because they cannot access the best deals. This financial squeeze makes finding fair loans for single parents on benefits uk even more vital. If you own your property, homeowner loans may offer lower interest rates by using your home as security.

The "Affordability" Myth vs Reality

Modern lenders prioritise your "disposable income" over your specific job title. They want to see what remains in your bank account after you pay for the essentials.

While UK lending algorithms include childcare costs. Lenders also look at how stable your Universal Credit or Child Benefit payments are. Your ability to repay the debt today matters, not just how you earned your money yesterday. This transparency ensures you aren’t taking on more than you can handle.

Why Traditional Banks Often Say No

High-street banks often rely on rigid, outdated criteria. They prefer "standard" earners and often struggle to process applications where benefits form the majority of the income.

Historically, the UK Social Fund closely linked family financial support, but today’s market offers more diversity. A specialist broker acts as your advocate. They connect you with providers who understand non-standard income and respect your autonomy.

Types of Loans Available for Single Parents in 2026

Finding the right financial support depends on your specific needs and timeline. Whether you need immediate cash for a broken boiler or a long-term personal loan for a used car, several paths exist.

The 2026 market offers many loan options for single parents on benefits in the UK. These range from interest-free government support to specialist private lenders. Your goal is to match the loan type to your family’s specific situation and repayment capacity.

Government and Community Options

A Budgeting Loan is often the first port of call. These are interest-free and can provide up to £812 for those claiming Child Benefit.

Alternatively, Credit Unions offer community-based lending. The law caps their interest rates at 3% per month, roughly 42.6% APR. This makes them a safer alternative for those with lower incomes who want to avoid high-cost credit.

Short-Term and Personal Loans

For those with fair credit, unsecured personal loans remain a viable option. If you need money today for an urgent repair, payday loans offer a high-speed alternative.

We designed these for immediate family emergencies. Comparing these structures helps you maintain personal autonomy over your family budget while getting the support you need. Specialist lenders now focus on your current resilience rather than past mistakes.

Which Benefits Count as Income?

Lenders have become much more inclusive. Most now accept Universal Credit, Personal Independence Payment (PIP), Disability Living Allowance (DLA), and Child Benefit as valid income.

Be aware that some providers require benefits to make up only a specific percentage of your total income. This flexibility is a cornerstone of the modern, non-judgemental lending market. It makes sure no one unfairly excludes you because of your employment status.

The Role of Guarantor Loans

If your credit history is a hurdle, a guarantor loan allows a trusted friend to support your application. This often results in a lower APR. Alternatively, explore modern Open Banking Loans for instant verification without manual paperwork.

Ready to see what is available? Start today with a quick eligibility check that won’t impact your record.

Eligibility and Affordability: What UK Lenders Look For

Lenders in 2026 prioritise your financial behaviour over your employment status. When searching for loans for single parents on benefits uk, the "Three-Month Rule" is your most powerful tool.

Lenders typically want to see three consecutive months of stable benefit payments on your bank statements. This consistency proves you have a reliable "income floor" to support repayments. It gives them the confidence to say yes, based on your current resilience. It also reflects your ability to manage a household budget.

Proving Your Financial Resilience

“Open Banking has changed how we assess affordability for single parents,” says Sarah Jenkins. She is the Financial Inclusion Lead at UK Money Watch. She said this in June 2026. "It allows lenders to see real-time financial resilience rather than just a static, often outdated credit score."

This technology provides a transparent view of your ability to manage money. It shifts focus from past credit mistakes to your disposable income today. This helps ensure you are not unfairly penalised for your history.

Managing Your Debt-to-Income Ratio

Lenders calculate your debt-to-income ratio to ensure repayments are sustainable. "In 2026, we want a balanced ledger. We want debt repayments to stay below 35% of total benefit income," says James Thorne. He is a Senior Analyst at Credit Insight UK (May 2026).

Understanding your options for loans on benefits starts with knowing your data. Check your credit score for free via Experian or Equifax to see exactly what lenders see before you apply.

Preparing Your Bank Statements

Organising your finances before applying is essential. Avoid "red flags" on your statements, such as frequent gambling transactions or excessive overdrawn fees. These suggest financial instability to an automated system.

Ensure the benefit names on your statements match your application exactly. If you claim Universal Credit, the entry should clearly state "DWP UC" or a similar official marker. This helps avoid delays and supports a smooth, fair application process. It also respects your time.

Avoiding "No Credit Check" Scams

Stay vigilant against unregulated lenders promising "guaranteed" loans. These are often predatory scams designed to exploit urgent needs.

All FCA-regulated lenders must perform a credit or affordability check by law. They do this to ensure you aren’t taking on debt you can’t afford. We only work with regulated providers who follow these strict safety rules to protect your interests. If you’re ready to find a safe, fair quote, you can apply for a loan quote now.

How to Apply for a Loan Safely with I Need Cash

Applying for credit often feels like a high-stakes gamble when you are managing a household alone. Every rejection from a high-street bank can leave a mark on your record, making future attempts even harder.

We eliminate this stress. By applying once, we can search many lenders. This increases your chances of finding loans for single parents on benefits UK.

You won’t need to apply many times by hand. We act as your advocate, connecting you to providers who value your stability.

Your credit score is precious. We use advanced soft search technology to protect it. This means you can see your personalised options.

You can also check if you’re eligible.

You can do this without it showing up on your financial history.

Ready to see your options? Get a loan quote today and take the first step toward financial tranquility.

Our Non-Judgemental Approach

We position ourselves as your supportive partner, not a gatekeeper. Our network includes specialists who specifically cater to those with non-traditional income or less-than-perfect credit records.

We don’t judge you for past financial hiccups; we look for reasons to approve you based on your current affordability. This inclusive approach ensures single parents, often marginalised by traditional institutions, have a seat at the table. It also supports the personal autonomy they deserve.

Next Steps After Approval

Once you are matched with a lender, transparency remains the priority. Your final contract will clearly state the Annual Percentage Rate (APR). It will also list the total cost of credit. It will include your exact repayment dates.

You are always in control of the decision. From July 15, 2026, new FCA rules will provide stronger consumer protection across many credit types. They also add stricter affordability checks to help keep you safe. Start your journey now with a mobile-friendly process.

Take Charge of Your Family’s Financial Future

You now have the tools to navigate the lending market with confidence. Remember that your benefits are a legitimate foundation for credit.

Modern lenders are increasingly focused on your real-world affordability rather than just a job title. By prioritising financial stability and preparing your bank statements, you move closer to the flexibility your family needs. Finding loans for single parents on benefits in the UK doesn’t have to mean rejection. It’s about finding a lender who understands your life.

We are here to act as your advocate. As an FCA authorised and regulated broker, we offer a free service.

It connects you to a wide panel of specialist UK lenders.

They understand your unique situation. We value your personal autonomy and work to find terms that fit your individual conditions. Our goal is to move you from a state of financial anxiety to a feeling of empowerment and tranquility.

FAQ

Can I get a loan on Universal Credit with no job?

Yes, you can. Specialist lenders in 2026 treat Universal Credit as a stable income stream for their affordability assessments. They value your ability to meet monthly repayments rather than your employment status.

This shift makes it easier to find loans for single parents on benefits uk even without a job. Your current financial resilience matters more than your past history or job title.

How much can a single parent borrow on benefits?

Borrowing limits depend on your specific award and monthly outgoings. As of June 2026, the government caps Budgeting Loans for people on Child Benefit at £812. Private lenders may offer higher sums, but they’ll strictly assess your disposable income first.

They want to ensure the debt is affordable for your family. They do not want it to squeeze your daily budget or cause future financial stress.

Will applying for a loan affect my benefit payments?

No, taking out a loan doesn’t count as income for benefit purposes. It won’t reduce your monthly award directly. You just need to keep an eye on the Universal Credit savings threshold.

Savings below £6,000 don’t affect your payments. If a large loan pushes your total capital above this limit, we might reduce your monthly award until the balance drops back down.

What is the fastest way to get an emergency loan on benefits?

The quickest route is usually through an online broker matching you with a specialist lender. These providers use Open Banking technology to verify your income instantly. This allows for rapid decisions on loans for single parents on benefits uk, often providing funds within hours. An efficient way to handle urgent family emergencies or unexpected household repairs without a long wait.

Are there specific grants for single parents that I should try first?

Yes, always explore non-repayable grants before taking on debt. Charities like Buttle UK or Turn2us offer support for specific household needs.

You should also check your local council’s Crisis and Resilience Fund. This scheme replaced the Household Support Fund in April 2026. It provides emergency help with food, fuel, or essential items. It supports families who are in immediate need.

Related links

Who qualifies for for 30 hours free childcare and how to apply

Aid for low in come families (part 3): find financial aid

1000 Loan bad credit UK direct lenders guide

Aid for low in come families (part 1): Government emergency loans

Article by

Mandy Paige

Social Content Writer and Blogger

Mandy has been writing for various website for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it lead her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a wiz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.