How to Get a Vehicle Loan: Your Guide to Funding Your Next Car

- April 26, 2026

- Remy Anderson

- Car Finance

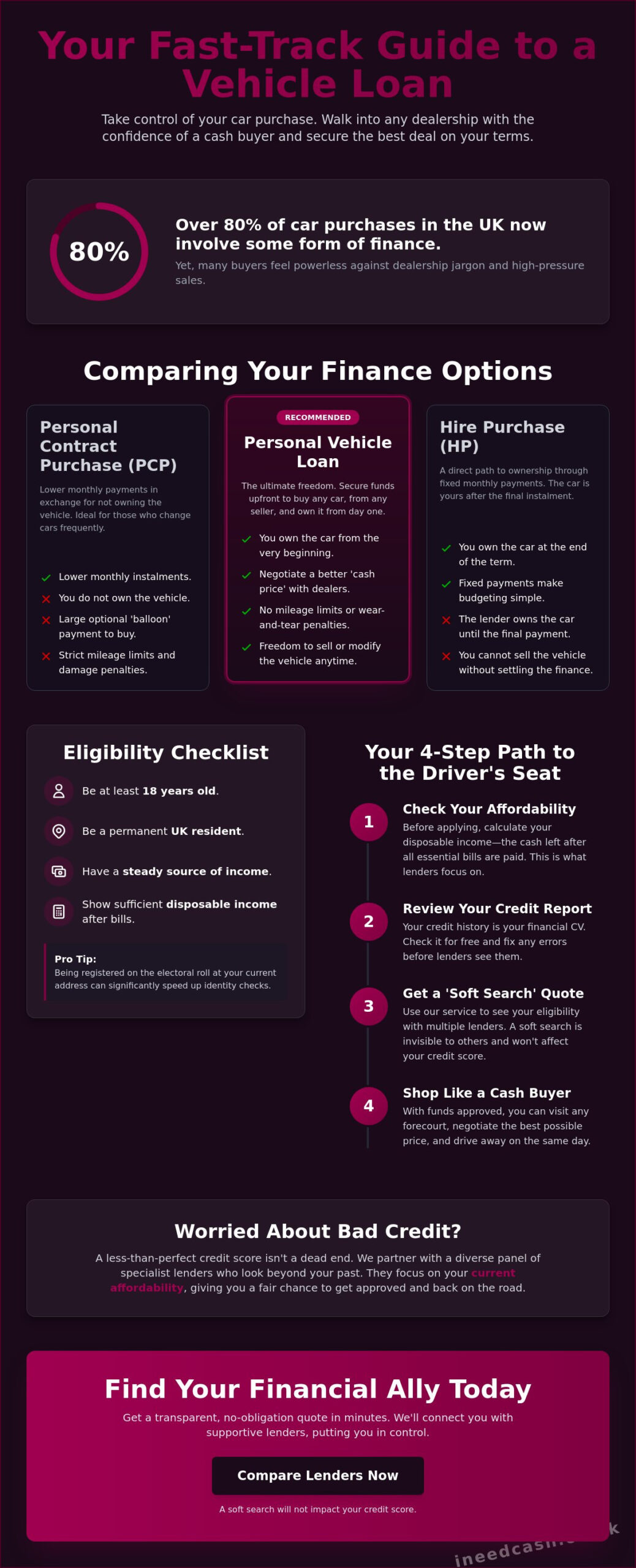

What if you could walk onto a car forecourt with the confidence of a cash buyer, completely avoiding the high-pressure sales pitch in the back office? Over 80% of car purchases in the UK now involve some form of finance, yet many drivers still fear the sting of rejection from traditional high-street banks. It’s stressful to feel like a gatekeeper is standing between you and the keys to your new vehicle. You probably want a simple way to drive away without the confusion of PCP or HP jargon clouding your vision.

We believe everyone deserves a fair shot at getting on the road. This guide shows you exactly how to get a vehicle loan on your terms, regardless of your past credit mistakes. You will learn how to secure the best finance for your specific situation, compare the total cost of borrowing, and access funds today so you can buy your car tomorrow. We’re stripping away the complexity to give you a clear, fast path to car ownership. Be in control and get the support you need to drive away with confidence.

Key Takeaways

- Understand why owning your car from day one might be better than dealership finance and how to choose the right credit path.

- Discover how lenders assess your disposable income and the specific criteria you need to meet for a quick decision.

- Compare the pros and cons of Hire Purchase and PCP to ensure your monthly instalments suit your lifestyle and long-term goals.

- Follow our expert guide on how to get a vehicle loan by identifying your surplus cash and fixing credit report errors before you apply.

- Learn how the “I Need Cash ethic” puts you in control on your terms by connecting you with a diverse panel of supportive lenders.

Table of Contents

- What is a Vehicle Loan and How Does It Work?

- Eligibility Requirements: Can You Get a Vehicle Loan?

- Comparing Your Options: Hire Purchase vs PCP vs Personal Loans

- How to Apply for a Vehicle Loan: A Step-by-Step Guide

- Finding Your Financial Ally with I Need Cash

What is a Vehicle Loan and How Does It Work?

Need a new set of wheels today? A vehicle loan is a straightforward form of personal credit designed to get you behind the wheel of a car, van, or motorcycle without the wait. It’s a simple arrangement where a lender provides the cash you need upfront, and you pay it back over a fixed period. Unlike some complex dealership schemes, a personal vehicle loan often means you own the car outright from day one. There’s no middleman holding onto the logbook until your final payment. Understanding how to get a vehicle loan starts with the repayment structure. You’ll typically repay the balance in fixed monthly instalments over a set term. Most UK lenders offer terms between one and seven years. A shorter term means you pay less interest overall, while a longer term keeps your monthly outgoings lower. It’s all about finding the balance that fits your monthly budget and gives you peace of mind. When you browse for quotes, you’ll see the term “Representative APR” frequently. This is a vital piece of the puzzle in how car financing works across the UK. By regulation, this rate must be offered to at least 51% of successful applicants. Your individual rate might vary based on your credit history, but this figure helps you compare different lenders fairly. We want you to be in control on your terms, so we always aim for transparency in every quote.The Difference Between Secured and Unsecured Vehicle Finance

Unsecured loans, often called personal loans, are the most popular choice for UK car buyers. These are based on your creditworthiness and your ability to pay, rather than the vehicle itself. Secured loans use the car as collateral. While secured options can sometimes offer lower interest rates for those with a less-than-perfect credit score, they carry higher risk. If you fall behind on payments, the lender has the right to repossess the vehicle. Most drivers prefer the flexibility and protection of an unsecured loan to keep things simple and stress-free.Why Choose a Loan Over Dealership Finance?

Choosing a personal loan over dealership finance puts the power back in your hands. Showrooms can be high-pressure environments where sales staff push specific finance products to meet targets. By securing your own loan first, you can browse at your own pace. You won’t have to worry about restrictive mileage limits or massive “balloon” payments that often catch people out at the end of a Personal Contract Purchase (PCP) deal. When you know how to get a vehicle loan before visiting the lot, you become a cash buyer in the eyes of the dealer. This often allows you to negotiate a much better “cash price” for the vehicle. Dealers want the sale finalised quickly, and having funds ready to go gives you a significant advantage. It’s the most efficient way to shop, ensuring you get the car you want at a price you’ve chosen.Eligibility Requirements: Can You Get a Vehicle Loan?

Understanding how to get a vehicle loan starts with meeting the foundational criteria. You must be at least 18 years old and a permanent UK resident to apply. Lenders require a steady source of income, typically evidenced by three months of payslips or bank statements. They don’t just look at your total salary; they focus on your disposable income. This is the amount of cash remaining after you have paid for your rent or mortgage, council tax, utility bills, and groceries. Your credit report serves as a financial CV. It determines the interest rates you are offered and your total borrowing limit. A higher score often leads to lower monthly costs. One simple way to boost your chances is by joining the electoral roll. Data shows that being registered to vote at your current address can significantly speed up the identity verification process. For a deeper look at what lenders evaluate, this consumer guide to auto loans provides a helpful breakdown of the standard requirements.Bad Credit and Vehicle Finance: Is It Possible?

A low credit score is not an automatic “no.” Specialist lenders now exist to help people who have been turned down by high street banks. I Need Cash works with a wide, varied panel of lenders who look at your current affordability rather than just your past mistakes. If you have a CCJ or a default from two years ago, you can still find a path to ownership. The key is honesty. Declaring your financial history upfront allows us to match you with a lender that specialises in your specific situation.The Importance of a Soft Credit Search

Learning how to get a vehicle loan safely means protecting your credit file. A soft credit search allows you to see your eligibility and potential rates without leaving a visible footprint for other lenders. You should avoid making multiple “hard” applications in a short period, such as three applications in 30 days. This behaviour can make you look desperate for credit and may lower your score. I Need Cash prioritises soft searches to ensure you stay in control of your financial health. You can view your potential quotes today without any risk to your current rating.Comparing Your Options: Hire Purchase vs PCP vs Personal Loans

Choosing finance is about more than just the monthly cost. You want a deal that fits your life. Hire Purchase (HP), Personal Contract Purchase (PCP), and Personal Loans are the three heavyweights in the UK market. Each one works differently. Understanding how to get a vehicle loan is the first step to saving thousands of pounds over the life of your car.- Hire Purchase (HP): You pay a deposit, usually 10 percent of the car’s price. You then make fixed monthly instalments. Once the last penny is paid, the car is yours.

- Personal Contract Purchase (PCP): This offers the lowest monthly costs. You aren’t paying for the whole car, just the depreciation. To keep it at the end, you must pay a massive ‘balloon’ payment.

- Personal Loans: You borrow the cash from a bank or lender. You buy the car outright. You then pay the lender back over a set time.

Which Option Costs More in the Long Run?

PCP feels like the cheapest choice every month. It’s tempting. However, if you want to keep the car, PCP is often the most expensive route. The interest builds up on that large balloon payment for years. HP is more predictable. You know exactly what the total cost is from day one. Watch out for hidden rules too. HP and PCP often force you to use approved service centres. These can be 20 percent more expensive than your local garage. A personal loan avoids these traps entirely.Flexibility and Ownership Rights

Personal loans give you the ultimate freedom. You are the legal owner the moment you hand over the cash to the dealer. This is why they are the favourite choice for used car buyers. If you want to sell the car next month, you can. With HP, you don’t own the vehicle until the final payment. You can’t sell it without the lender’s permission. Choose the finance that lets you make the rules. It’s about finding financial fluidity that works for you and your family.How to Apply for a Vehicle Loan: A Step-by-Step Guide

Ready to get behind the wheel? We want to help you move from financial anxiety to total empowerment. Following a clear process ensures you stay protected and get the best deal for your circumstances. Knowing how to get a vehicle loan starts with a clear plan and the right financial ally by your side. Step 1: Calculate your surplus. Forget the total car price for a moment. Look at your monthly bank statements and find your “surplus” cash after all bills, rent, and food are paid. This is your true budget. Be realistic about what you can afford to ensure you stay in control on your terms. Step 2: Clean up your credit file. Use free services like Equifax or Experian to check your report. Errors happen; a simple mistyped house number can damage your score. Fix these mistakes before you apply to give yourself the best chance of approval. Step 3: Let a broker do the heavy lifting. Don’t waste hours filling out dozens of forms. Use a broker platform to compare a wide panel of lenders with one quick search. This saves time and helps you find lenders ready to say yes to your specific profile. Step 4: Weigh up the quotes. Look for the sweet spot between a low APR and a monthly cost that feels comfortable. Once you understand how to get a vehicle loan through a broker, you will see that quotes won’t affect your credit score when using soft-search technology. This allows you to shop around risk-free. Step 5: Secure your funds. Complete the formal application once you’ve picked your winner. Many lenders transfer funds within 24 hours, often even on the same day, so you can head straight to the dealership with confidence. Stop waiting and start driving. Get your vehicle loan quote today and see your options in minutes.Documents You Will Need to Organise

Speed is everything when you want a new car. Have these items ready to keep the process moving fast and maintain your peace of mind:- Proof of Identity: A valid UK driving licence or passport.

- Address History: You need your full address details covering the last 3 years.

- Income Verification: Your last 3 months of payslips or bank statements to prove you can handle the repayments.

- Vehicle Info: Details of the car you want, though many lenders approve a set amount before you even choose the vehicle.

What to Do If You Are Declined

If the answer is “no,” don’t panic. This isn’t the end of the road. Ask the lender for the specific reason; it is often a simple data mismatch or a recent change in your employment status. The I Need Cash ethic is about second chances, but you must be smart. Wait at least 30 days before trying again to let your credit file settle. Applying for multiple loans in a single week looks frantic to banks. Instead, consider a broker who specialises in matching applicants with lenders who look past a thin credit history.Finding Your Financial Ally with I Need Cash

Securing the right car finance often feels like an uphill battle, especially if your credit history has a few bumps. That’s where we step in to change the narrative. I Need Cash isn’t a lender; we’re a dedicated broker working on your behalf to find the most competitive deal available. We understand that life happens and financial situations change. Our “I Need Cash ethic” ensures we provide a non-judgmental, inclusive service for everyone, regardless of their past financial hiccups. We see the person, not just the paperwork. When you’re figuring out how to get a vehicle loan, you shouldn’t have to jump through hoops or wait weeks for an answer. We provide access to a wide, varied panel of lenders through one simple application. This process takes just minutes and, most importantly, it won’t hurt your credit score. We use soft search technology to provide initial quotes, giving you the freedom to explore your options without the fear of damaging your rating. Our platform is built for speed, support, and transparency, offering you the financial fluidity needed to get behind the wheel faster.Be in Control on Your Terms

Traditional banks often give a flat “yes” or “no,” leaving you with zero wiggle room or alternative options. We believe in empowering you with choices. By matching you with various lenders from our panel, we put you back in the driving seat. Our process is digital-first. You can apply from your phone whilst on your lunch break or sitting at home, anywhere in the UK. Because we’re authorised and regulated by the Financial Conduct Authority (FCA), you can enjoy total peace of mind. You’re dealing with a professional ally that prioritises your security and fair treatment at every stage.Start Your Journey Today

Many brokers hide costs in the fine print, but we don’t play those games. There are no hidden fees for using our matching service; it is completely free for every applicant. We focus on removing the stress from how to get a vehicle loan by providing clear, honest support from start to finish. Don’t let financial anxiety hold you back from the car you need for work, family, or personal freedom. Get your quotes today and see exactly how much you could borrow for your next vehicle. The road to your dream car starts with a single, risk-free step. Apply for your vehicle loan quote today and experience a faster, fairer way to fund your future.Drive Away with Confidence Today

Securing the keys to your next car starts with understanding your finance options. Whether you choose the flexibility of a Personal Contract Purchase (PCP) or the straightforward path of Hire Purchase (HP), the right choice puts you in the driving seat. You’ve now mastered the essentials of how to get a vehicle loan by checking your eligibility and following our step-by-step application guide. It’s time to move from financial anxiety to total empowerment. Finding the right car is exciting; your funding should feel the same way. I Need Cash is your non-judgmental financial ally in this journey. We’re authorised and regulated by the Financial Conduct Authority, so you know your interests are protected. Our free service provides instant access to a wide panel of independent UK lenders without any hidden broker fees. We believe in the I Need Cash ethic of transparency and speed. You can explore your options in minutes and stay in control on your terms. Your next vehicle is within reach, and we’re here to help you grab the keys. Start your vehicle loan search now – it won’t affect your credit score Get the support you need and start your journey toward a better drive today.Frequently Asked Questions

Can I get a vehicle loan with a very bad credit history?

Yes, you can get a vehicle loan even if you have a poor credit history. Our panel of lenders looks at your current affordability rather than just focusing on past mistakes. We believe in the “I Need Cash ethic” of giving everyone a fair chance to move forward. If you can prove you afford the monthly repayments today, you could secure the car you need within 24 hours. Be in control on your terms and apply now.How long does it take for the money to arrive in my bank account?

You could see the money in your bank account in as little as 15 minutes after final approval. Most lenders on our panel aim to complete the transfer within 24 hours of you signing the digital agreement. This rapid speed ensures you don’t miss out on the perfect car whilst browsing. Start your application today to find out how quickly you can get behind the wheel of your next vehicle.Is it better to get a car loan from a bank or a dealership?

Choosing between a bank or a dealership depends on your need for speed versus specific interest rates. Banks often provide lower rates for those with excellent credit, but dealerships offer point-of-sale convenience. Using a broker gives you access to a wide varied panel of lenders, meaning you get more choice. This helps you understand how to get a vehicle loan that fits your specific budget and personal circumstances.What is the maximum amount I can borrow for a vehicle loan?

Most UK lenders offer personal vehicle loans up to £50,000, though some specialist providers go higher for luxury cars. Your specific limit depends on your monthly income and current debt levels. Lenders typically cap repayments at 25 percent of your net monthly take-home pay to ensure the loan remains manageable. Knowing your limit helps you shop with confidence and stay in control of your finances without any hidden surprises.Will applying for a car loan quote affect my credit score?

No, checking your eligibility with us won’t affect your credit score at all. We use a soft search to find you the best rates from our lenders without leaving a visible mark on your file. You only get a hard search once you decide to proceed with a specific offer. This risk-free approach allows you to be in control on your terms while exploring your options for a new car today.Do I need a deposit to get a vehicle loan through a broker?

You don’t necessarily need a deposit to secure funding through a broker. We work with lenders who offer 100 percent finance options, meaning you can borrow the full purchase price of the car. According to 2023 industry data, 0 percent deposit deals are increasingly popular for used car purchases. This removes the stress of saving for months and lets you get on the road much faster than traditional methods.Can I use a personal loan to buy a used car from a private seller?

Yes, using an unsecured personal loan is a brilliant way to buy a car from a private seller. Because the money is paid directly into your bank account, you can pay the seller via bank transfer immediately. This flexibility is a key part of how to get a vehicle loan when you aren’t buying from a traditional forecourt. It puts the bargaining power firmly in your hands to get the best deal.What happens if I can’t afford my monthly vehicle loan payments?

You must contact your lender immediately if you struggle to make your payments. Under Financial Conduct Authority (FCA) rules updated in 2024, lenders must provide tailored support to customers in financial difficulty. This might include a temporary payment holiday or a revised repayment plan. Taking action early protects your credit score and helps you find a sustainable way to manage your debt while keeping your car for daily use.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various website for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it lead her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a wiz with a pair of scissors as she originally trained as a hairdresser.