Homeowner Loans in the UK: The 2026 Guide to Financial Fluidity

- April 23, 2026

- Remy Anderson

- Homeowner Loans

Estimated reading time: 16 minutes

What if your home was more than just a roof over your head, but the exact key to erasing your monthly financial stress with a homeowner loan? You’ve worked hard to get on the property ladder, yet the pressure of high-interest debt or a house that needs modernising makes it feel like you’re falling behind. It’s frustrating when traditional banks turn you away because your credit score isn’t perfect, leaving you worried about your future security.

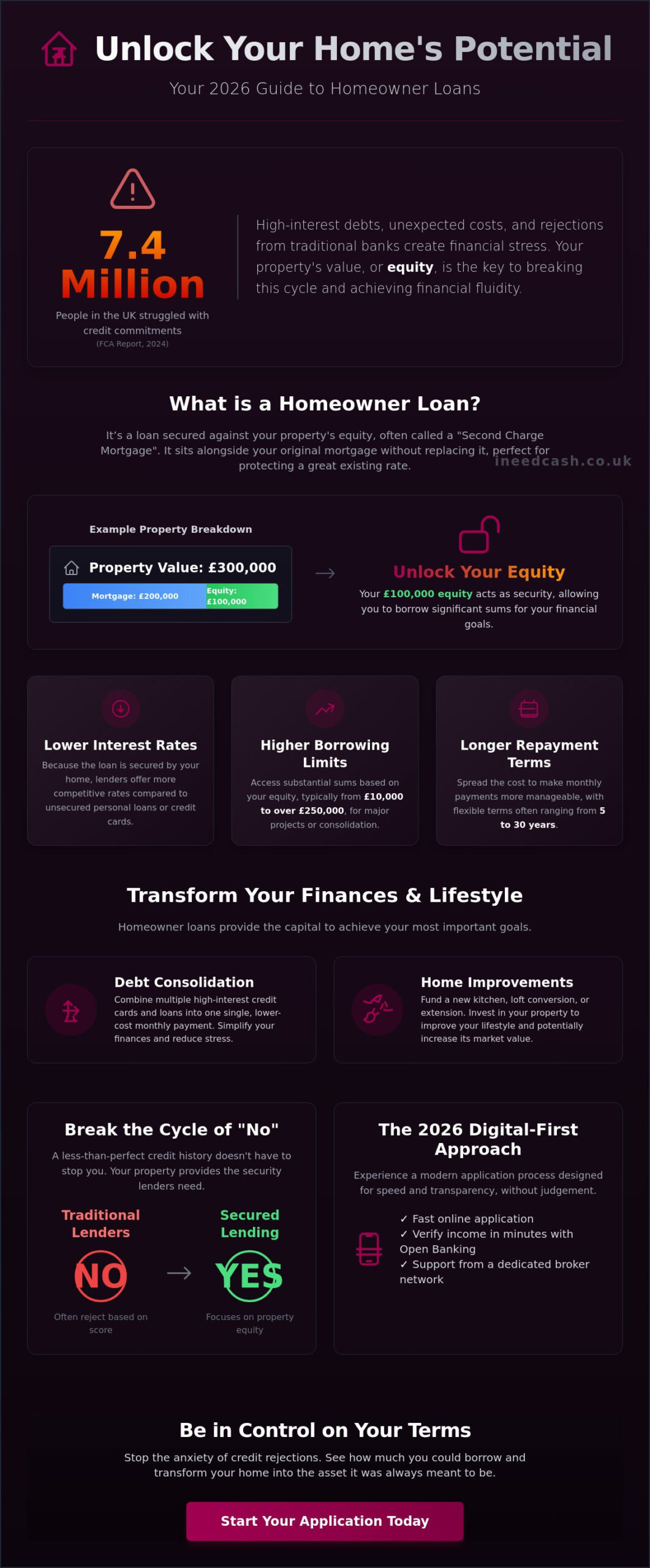

We believe that homeowner loans should be accessible tools for everyone, especially since the Financial Conduct Authority (FCA) 2024 report showed that over 7.4 million people in the UK struggled to meet their credit commitments. We’re here to show you how to unlock your equity with total confidence and finally get that “yes” you deserve. You can stop the anxiety over credit rejections and start seeing your property as a tool for financial fluidity through the I Need Cash ethic. Our 2026 guide explains the vital differences between second charges and remortgaging whilst showing you how to consolidate debt into one single, manageable payment. Start being in control on your terms today and transform your home into the asset it was always meant to be

Key Takeaways

- Turn your property’s equity into immediate “financial fluidity” to cover urgent costs whilst staying in the home you love.

- Learn how to use your home’s value to secure competitive homeowner loans, even if you’ve been turned down by traditional banks.

- Break the cycle of “no” by understanding how secured lending provides a flexible path forward for those with a less-than-perfect credit history.

- Experience the 2026 digital-first approach that uses Open Banking to verify your income in minutes, ensuring speed without the stress.

- Discover how to be in control on your terms by using a supportive broker network dedicated to transparency and your peace of mind.

Table of Contents

- What is a Homeowner Loan? Achieving Financial Fluidity in 2026

- How Homeowner Loans Work: Equity, LTV, and Security

- Homeowner Loans for Bad Credit: Breaking the “No” Cycle

- The 2026 Application Process: Speed without Judgement

- Be in Control on Your Terms: Why I Need Cash?

What is a Homeowner Loan? Achieving Financial Fluidity in 2026

Your home is more than just a roof; it’s a powerful financial tool. If you’re a property owner in the UK, understanding What is a secured loan? is the first step toward unlocking your property’s potential. A homeowner loan is a form of debt tied directly to the equity in your house.

It allows you to borrow large sums of money by using your property as security for the lender.

This is the I Need Cash ethic in action: providing a supportive path to peace of mind when traditional bank doors stay shut. We focus on the concept of financial fluidity. Most homeowners have significant wealth locked away in bricks and mortar, but that wealth is illiquid. You can’t spend a kitchen cupboard or a garden fence. By opting for homeowner loans, you transform that stagnant equity into immediate, usable capital. It moves you from a state of financial anxiety to a position of total control, allowing you to address urgent needs or long-term goals without selling your home. It’s vital to distinguish this from your standard mortgage.

Think of a homeowner loan as a “second charge” on your property. Your original mortgage remains exactly as it is, untouched and in first place. This second loan sits behind it. This structure is perfect if you have a great interest rate on your main mortgage and don’t want to lose it through remortgaging. You get the cash you need whilst keeping your primary financial arrangements intact.

The Core Benefits of Choosing a Secured Path

Opting for a secured path offers distinct advantages that unsecured borrowing simply can’t match. Because the loan is backed by your home, lenders feel more protected, which usually translates into lower interest rates for you. This makes borrowing larger amounts much more affordable than using credit cards or high-interest personal loans. You can also organise your finances more effectively with longer repayment terms, often stretching from 5 to 30 years.

- Lower Interest Rates: Access cheaper borrowing compared to standard personal loans.

- Longer Repayment Terms: Reduce your monthly outgoings by spreading the cost over a decade or more.

- Higher Borrowing Limits: Access substantial sums, often ranging from £10,000 to over £250,000, depending on your available equity.

Common Uses: From Renovations to Consolidation

Debt consolidation is the most frequent reason UK residents seek homeowner loans. If you’re balancing multiple credit cards and store loans, rolling them into one single monthly payment can dramatically simplify your life. It’s about streamlining your behaviour and reducing the mental load of debt management. You replace high-interest chaos with one structured, manageable payment. Investing in your property is another popular choice.

High-end home improvements, such as a £40,000 kitchen renovation or a loft conversion, don’t just improve your lifestyle; they often increase the market value of the asset itself. Beyond that, these loans fund major life milestones. Whether it’s a wedding or helping a child with a university deposit, you can access the funds today without the stress of high-street bank bureaucracy. Be in control on your terms and start building the future you deserve.

How Homeowner Loans Work: Equity, LTV, and Security

Unlock the value hidden in your bricks and mortar. To get started, you need to understand equity. This is the portion of your home you actually own. If your property is valued at £300,000 and you owe £200,000 on your mortgage, you have £100,000 in equity. Lenders use this as a safety net. It allows them to offer larger sums than standard bank loans.

Be in control on your terms by using what you’ve already built. Your Loan-to-Value (LTV) ratio is the decider for your interest rate. If you want to borrow £30,000 and your home is worth £300,000, your LTV is 10%. Lower LTVs usually unlock the most competitive rates on the market. It’s vital to remember that your home acts as the collateral. You can find a clear definition of what is a secured loan through Citizens Advice to understand the legal weight of this agreement. If you don’t keep up with repayments, the lender could repossess your property. A “Second Charge” is a separate loan that sits alongside your mortgage without replacing your original deal.

Homeowner Loans vs. Personal Loans: A Side-by-Side Comparison

Choose the path that fits your budget. Personal loans are great for quick cash, but they usually cap out at £25,000. If you need more for a major renovation or debt consolidation, homeowner loans offer much higher limits, often reaching £100,000 or more depending on your equity. Because the loan is secured, lenders are often more relaxed about “thin” credit files or past mistakes. You aren’t just a number on a spreadsheet; your property provides the security they need to say yes. While personal loans might land in your account faster, secured options provide more flexibility with longer repayment windows that keep monthly costs manageable.

Understanding the Cost: APRC and Arrangement Fees

Don’t just look at the monthly payment. The Annual Percentage Rate of Charge (APRC) shows the total cost, including the interest and mandatory fees over the full term. You’ll need to budget for specific costs like valuation fees, which can range from £200 to over £500, alongside legal fees and potential broker commissions. Transparency is part of the I Need Cash ethic, so we always recommend you use a loan calculator to see exactly how these costs impact your wallet. Get a clear picture of your future repayments before you commit. It’s about moving from financial stress to total peace of mind today.

Homeowner Loans for Bad Credit: Breaking the “No” Cycle

Stop listening to the banks. A low credit score isn’t a dead end. When you apply for homeowner loans, you aren’t just a number on a spreadsheet. You’re a property owner with a valuable asset. This security changes the game for a lender. It reduces their risk significantly, which means they can say “yes” even if you’ve had a CCJ or a missed payment in the last 12 to 24 months. We believe in the I Need Cash ethic; everyone deserves a second chance to fix their finances and find peace of mind. Best of all, checking your options is completely risk-free. Our initial matching process uses a soft search. You get a real quote without hurting your credit score or leaving a footprint for other lenders to see.

Why a Broker is Your Best Financial Ally

High street banks are rigid. If you don’t fit their perfect box, they reject you instantly. We do things differently. I Need Cash acts as your financial ally, connecting you to a wide varied panel of lenders who specialise in complex situations. Whether you’re self-employed with one year of accounts or dealing with past defaults, we find the match that works for you. You get more choice and better odds than walking into a single branch. It’s about putting you back in the driving seat of your financial future. Get started today and see what’s possible without any upfront commitment or hidden fees.

Mitigating Risk: Borrowing Responsibly

Taking out homeowner loans is a serious commitment, so we want you to feel protected. Every lender on our panel is FCA regulated. This means they must follow strict rules to protect your interests and treat you fairly. Before you apply, sit down and look at your monthly outgoings. Use an affordability check to ensure you can comfortably manage the repayments alongside your mortgage. Keeping control of your budget is the best way to ensure your home remains safe. If you decide to move house, you usually have two clear options:

- Porting: You can often move the loan to your new property if the lender agrees.

- Repayment: You can repay the balance using the equity from your house sale proceeds.

We help you find the flexibility you need to move forward. Be in control on your terms and borrow with confidence knowing you have a team that supports your goals.

The 2026 Application Process: Speed without Judgement

Applying for homeowner loans shouldn’t feel like a trip to the headmaster’s office. The 2026 lending environment is built on a digital-first approach that values your time and your privacy. You need cash today, not in three weeks. By embracing Open Banking, we’ve stripped away the archaic barriers that used to slow things down.

This technology allows for secure, instant income verification in under 180 seconds; this means you don’t have to hunt for old paper statements or wait for a manual review. Our system operates on a clear problem-solution logic. You have a financial goal, and we provide the immediate bridge to reach it. One single application puts your requirements in front of a wide panel of lenders simultaneously.

The “I Need Cash” ethic is our commitment to delivering this lightning-fast speed alongside a protective, ethical framework that keeps you in control on your terms. We believe speed should never come at the cost of your financial safety.

Step-by-Step: From Application to Funding

The journey from clicking “apply” to seeing the funds in your account is designed to be frictionless. We’ve optimised every touchpoint to ensure you stay informed and empowered during the process.

- Step 1: The 2-minute online form. You only need to provide the essentials. This includes your contact details, the estimated value of your property, and your current mortgage balance. It’s fast, simple, and quotes won’t affect your credit score.

- Step 2: Instant matching. Our algorithm works in real-time to find your favourite lender from our panel. It compares your profile against thousands of data points to ensure you get a match that fits your specific circumstances.

- Step 3: Verification. Once matched, you’ll complete the final checks. This involves a secure digital verification of your identity and homeownership status to keep the process protected and compliant.

What Documents Will You Need?

While we use digital tools to speed things up, having your details ready will accelerate your funding even further. Most lenders require three core pieces of information to finalise your homeowner loans and release the cash.

- Proof of income. Usually, this means your last three monthly payslips. If you are self-employed, you will need your latest SA302 or tax returns from the most recent tax year to confirm your earnings.

- Mortgage statements. Lenders need to see your current balance and a clean payment history for the last 12 months. This proves you are a responsible homeowner and helps calculate your available equity.

- Identification. A valid UK passport or driving licence is required. This ensures a secure, protected process and prevents identity fraud throughout the application.

Ready to see what you could borrow without the stress? Apply today and be in control on your terms.

Be in Control on Your Terms: Why I Need Cash?

Finding the right financial path shouldn’t feel like a battle. We’ve built a service that puts you back in the driving seat. Dealing with the UK market for homeowner loans is often complex, but our role as a broker is to strip away that difficulty.

We connect you with a vast panel of lenders who see your potential, not just your paperwork. You don’t have to spend hours comparing fine print; we do the heavy lifting to find the most competitive rates available for your specific circumstances.

Our service is 100% free for every applicant. You’ll never see a bill from us because the lenders pay the commission once a deal is finalised. This means you get professional brokerage expertise without any upfront costs. We’re here to act as your financial ally, moving you away from the anxiety of debt and towards the peace of mind that comes with a structured, affordable plan. We believe in “financial fluidity,” ensuring you have the cash you need when you need it most.

The I Need Cash Ethic

We’ve built our reputation on a foundation of transparency and respect. The I Need Cash ethic means you’ll never face aggressive sales calls or hidden surprises in your loan terms. We aren’t gatekeepers standing in your way; we’re facilitators helping you unlock the value tied up in your property. While traditional banks might take 4 to 6 weeks to process secured lending, we focus on digital-first solutions that aim for “instant” feedback.

- Non-judgemental support: We look past previous credit blips to find a way forward.

- No-risk quotes: Checking your eligibility through our platform won’t affect your credit score.

- Total clarity: Every quote is presented in plain English, so you know exactly what you’re signing.

You deserve a lender that respects your time and your goals. By working with a wide variety of regulated UK lenders, we ensure you have a genuine choice. We prioritise speed, efficiency, and empathy in every interaction.

Take the First Step Today

Stop worrying about “what if” and start seeing what’s actually possible. Your home is your asset; let it work for you to consolidate debt, fund a renovation, or manage an unexpected expense. There’s no pressure and no obligation when you use our search tool. It’s a risk-free way to explore the homeowner loans market from the comfort of your own sofa. We’re ready to help you regain your financial confidence. Join the thousands of UK homeowners who have used our platform to find a better way to borrow. It takes less than two minutes to get started, and you could have a decision faster than you think. Be in control on your terms and find the solution that fits your life today.

Get your free homeowner loan quote now

Take Control of Your Financial Fluidity Today

Your property is your biggest asset, so it’s time to make it work harder for your 2026 financial goals. By leveraging your equity, homeowner loans provide a reliable way to access larger sums with more manageable terms than standard unsecured credit. You don’t have to let a less-than-perfect credit history hold you back anymore. Our process is designed for speed and empathy, giving you access to a wide varied panel of UK lenders who look at your potential rather than just your past mistakes. We’re here to help you bridge the gap between where you are and where you want to be. Safety is at the heart of everything we do. As an FCA Authorised and Regulated broker, we ensure your journey is protected and transparent. You can browse your options with confidence because our quotes won’t affect your credit score. This is about giving you the tools to be in control on your terms without the fear of rejection. Start your journey toward financial freedom with a team that values your time and your trust. You’ve got the equity; now get the cash to match your ambitions. Apply for your homeowner loan today

Frequently Asked Questions

Can I get a homeowner loan with a very bad credit score?

Yes, you can often secure a loan even if your credit history isn’t perfect. Because homeowner loans are secured against your property, lenders look at your available equity rather than just your credit score. Statistics from the Finance & Leasing Association show that secured lending remains accessible for people with past defaults or CCJs. It’s about the value in your home and your current ability to pay, not just your past mistakes.

What is the difference between a homeowner loan and remortgaging?

Remortgaging replaces your existing mortgage with a completely new one, while a homeowner loan is a separate debt that sits alongside your current mortgage. You keep your original mortgage rate, which is vital if you secured a low rate before the 2023 interest rate hikes. This approach helps you avoid Early Repayment Charges that typically range from 1% to 5% of your total mortgage balance.

How much can I borrow against my house in 2026?

Most lenders allow you to borrow between 75% and 95% of your property’s total value, minus what you still owe on your mortgage. In 2026, your borrowing limit will depend on your equity levels and the Bank of England’s base rate at that time. If your home is worth £300,000 and your mortgage is £200,000, you could potentially access up to £85,000 in cash depending on your income and affordability.

Will applying for a homeowner loan quote affect my credit score?

Getting a quote with us won’t affect your credit score at all. We use a soft search to check your eligibility, which is invisible to other lenders and doesn’t impact your rating. You only get a hard search on your file if you decide to proceed with a specific lender’s offer. Be in control on your terms and see your options today without any risk to your financial reputation.

Can I use a homeowner loan to pay off my existing debts?

Yes, using homeowner loans for debt consolidation is a very common way to simplify your finances. With average UK household non-mortgage debt reaching £4,453 in late 2023, many people use their equity to clear high-interest credit cards or store cards. This can significantly lower your monthly outgoings by moving multiple expensive debts into one lower-interest payment. Just remember that you are moving unsecured debt to a loan secured against your home.

What happens if I can no longer afford my loan repayments?

Your home is at risk if you do not keep up repayments on a loan secured against it. If you struggle, the FCA’s Mortgage Conduct of Business rules require lenders to treat you fairly and explore all options before taking action. You’ll typically receive a formal notice after two or three missed payments. It’s essential to contact your lender immediately to discuss a payment plan or a temporary breathing space period.

How long does it take to get the money from a homeowner loan?

You can usually expect the funds to arrive in your bank account within 14 to 28 days. The process includes a property valuation and a mandatory seven-day reflection period required by UK law to ensure you’re happy with the deal. We work with a wide varied panel of lenders to speed up the paperwork. This ensures you get your money as quickly as the legal and regulatory checks allow.

Is a homeowner loan the same as a second charge mortgage?

Yes, these two terms describe the exact same financial product. Since the Financial Conduct Authority took over regulation of these loans in March 2016, they have been governed by the same strict consumer protections as your main mortgage. Whether you call it a homeowner loan or a second charge, it means you are borrowing money using your property as security while leaving your primary mortgage completely undisturbed.

Related links