Cheapest Car Finance Loans: Find the Best UK Rates

- June 26, 2026

- Remy Anderson

- Finance

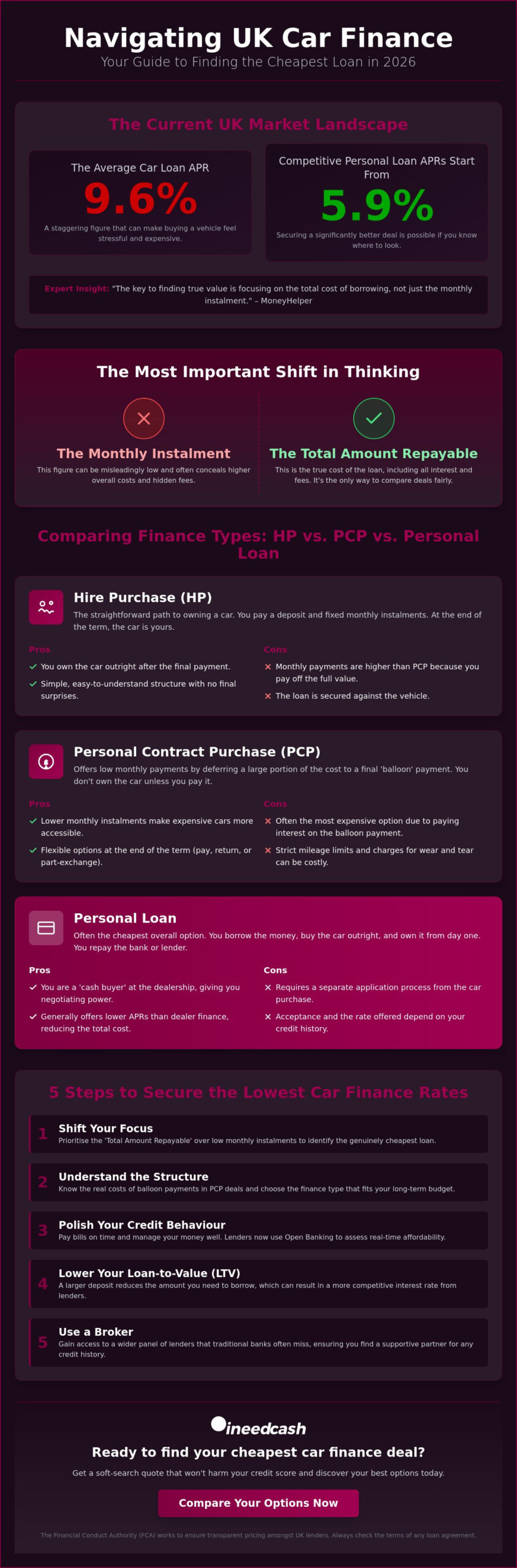

Did you know that the average car loan APR in the UK currently sits at 9.6%? It is a staggering figure that can make any driver feel anxious about their next vehicle purchase. You likely feel that finding the cheapest car finance loans is an uphill battle, especially whilst trying to decode the difference between PCP and HP or worrying about hidden fees. We understand that financial stress; it is why we are here to help you move from anxiety to total empowerment.

You can secure a significantly better deal by understanding the current market landscape. With the Bank of England holding the base rate at 3.75% as of June 2026, there are still highly competitive options if you know where to look. According to the Financial Conduct Authority (FCA), their motor finance redress scheme is expected to return £7.5 billion to consumers, highlighting just how important it is to have a transparent partner on your side. “The key to finding true value is focusing on the total cost of borrowing, not just the monthly instalment,” notes the advice team at MoneyHelper.

This article helps you navigate the UK market to find the absolute lowest rates and total costs for your next vehicle. We will show you how to secure a low-APR loan, explain the benefits of a soft search quote that won’t harm your credit score, and help you dodge the hidden traps that catch most buyers out.

Key Takeaways

- Shift your focus from monthly instalments to the Total Amount Repayable to identify the cheapest car finance loans available today.

- Uncover the hidden costs of ‘balloon’ payments and learn which finance type—HP, PCP, or Personal Loan—best suits your long-term budget.

- Master five practical steps to polish your credit behaviour and lower your Loan-to-Value ratio for a more competitive interest rate.

- Gain access to a vast panel of lenders that traditional banks often miss, ensuring you find a supportive partner regardless of your financial history.

- Understand how the FCA’s commitment to transparent pricing protects you from hidden fees and ensures a fair deal on your next vehicle.

What Defines the Cheapest Car Finance Loans in 2026?

Finding the cheapest car finance loans requires looking past the shiny monthly instalment figure. Many buyers fall into the trap of choosing a deal because the monthly cost looks affordable, only to realise they are paying thousands more over a five-year term. To secure a true bargain, you must focus on the “Total Amount Repayable”. This figure includes the loan principal, every penny of interest, and any hidden admin fees. Understanding what is car finance? and how its structure affects your long-term wealth is the first step toward financial tranquility.

The Financial Conduct Authority (FCA) works hard to ensure transparent pricing amongst UK lenders, especially following the motor finance redress scheme which is expected to return £7.5 billion to consumers. However, you must still be cautious of the “Representative APR”. This rate only has to be offered to 51% of accepted applicants. If your credit history is less than perfect, you might find yourself in the other 49% who pay more. In 2026, Open Banking is revolutionising this process. Lenders now assess your real-time spending behaviour rather than just a historic score, offering more tailored and potentially lower rates for those who manage their money well.

APR vs. Flat Interest Rates: The Hidden Difference

Always prioritise the APR over flat interest rates when comparing deals. A flat rate might look lower because it is calculated on the original loan amount, whereas APR accounts for the reducing balance as you pay it off. APR is the total cost of borrowing including fees and interest. It provides a level playing field for comparing different lenders. Actionable tip: Use a car finance calculator to check the total repayable amount and ensure you aren’t paying for “cheap” monthly costs with a massive overall debt.

The Impact of 2026 UK Economic Trends on Borrowing

The Bank of England has held the base rate at 3.75% as of June 2026, providing a period of relative stability for borrowers. While the average car loan APR remains around 9.6%, lenders have shifted their focus toward “affordability” in this post-inflationary climate. They aren’t just looking at what you earn; they are looking at what you keep. To get the cheapest car finance loans, you need to prove that your disposable income can comfortably handle the repayments without causing financial strain. This supportive approach from lenders aims to prevent buyers from overextending themselves in an uncertain economy.

Comparing Finance Types: HP, PCP, or Personal Loan?

Choosing the right structure is vital to securing the cheapest car finance loans. Hire Purchase (HP) is straightforward; you pay a deposit and then monthly instalments until you own the car outright. Because you are paying off the full value from day one, monthly costs are higher. However, you avoid the massive interest charges associated with deferred payments. If your goal is long-term ownership, this often beats complex dealer-led deals because there is no “option to purchase” fee or surprise final bill.

Why PCP Might Be More Expensive Than It Looks

Personal Contract Purchase (PCP) attracts buyers with low monthly payments, but it is often the most expensive choice in total interest. This happens because of the “balloon payment”—a large sum deferred until the end. You pay interest on this deferred amount throughout the whole term. To protect yourself, always review your consumer rights in car finance. Be wary of mileage limits and damage charges; exceeding these can quickly turn a “cheap” deal into a financial headache.

Unsecured personal loans from banks or brokers frequently provide the cheapest car finance loans. Representative APRs for these loans often start from 5.9% for amounts between £7,500 and £25,000. Compare this to the 8.9% or 9.9% common in dealer HP or PCP agreements. By using a personal loan, you become a cash buyer at the dealership. This gives you more leverage to negotiate the car’s price, as the dealer doesn’t need to worry about finance commissions.

The Homeowner Loan Alternative for High-Value Vehicles

For luxury or high-value vehicles, homeowner loans can provide access to lower rates by using your property as security. This often allows for longer repayment terms and larger loan amounts than unsecured options. “Secured debt typically offers lower interest rates because the lender’s risk is reduced, but it’s vital to remember your home is at stake,” says Sarah Coles, Head of Personal Finance at Hargreaves Lansdown, in a report for the Daily Express. If you want to see what options fit your budget, you can check your eligibility online today.

5 Steps to Secure the Lowest Car Finance Rates

Securing the cheapest car finance loans isn’t just about luck. It’s about preparation. You can actively lower your interest rates by following a few simple steps before you even visit a dealership. Start by cleaning up your credit favourite. Check that you are on the electoral roll and dispute any errors immediately. Even small mistakes on your record can push you into a higher interest bracket, costing you hundreds of pounds over the life of the loan.

Boosting Your Credit Score for a Better Tier

Lenders in 2026 use highly sensitive scoring models from agencies like Equifax and Experian. These models prioritise stability and recent behaviour. To ensure you qualify for the best tiers, avoid making any new credit applications for three to six months before applying for your car loan. This “quiet period” signals to lenders that you aren’t desperate for cash, making you a more attractive, lower-risk borrower. When comparing finance types, remember that your score dictates the APR you’ll actually receive.

Next, focus on your deposit. Increasing your down payment reduces the Loan-to-Value (LTV) ratio, which often triggers a lower interest rate. Aim for at least 10% to 20% of the car’s value. You should also opt for the shortest repayment term you can comfortably manage. Whilst a longer term lowers monthly costs, it massively increases the total interest paid.

The ‘Sweet Spot’ for Loan Duration

A 36-month term is often the most cost-effective balance. Data shows that stretching a loan to a 60-month term can nearly double the total interest paid compared to a 36-month term. This is a common trap that makes “cheap” monthly payments very expensive in reality. Finally, use a broker to perform a soft search. This allows you to see quotes from a panel of lenders without impacting your credit file. Avoid dealer add-ons like GAP insurance or paint protection; these are almost always cheaper when bought independently. If you want to find the cheapest car finance loans for your situation, get started with a quote today.

How a Broker Finds the Cheapest Deals for All Credit Types

Direct banks are gatekeepers. They have one set of rules; if you don’t fit their narrow criteria, you’re often left with a high-interest offer or a flat rejection. A broker acts as your advocate instead. By accessing a vast panel of lenders, a broker identifies the cheapest car finance loans tailored to your specific financial behaviour. This is especially vital given the current economic climate, where the Office for National Statistics (ONS) reports that household budget pressures are changing how we borrow. “The broker model increases competition, ensuring that even those with thin credit files can access the cheapest car finance loans through specialist panels,” notes a summary from the Competition and Markets Authority.

Soft Searches: Comparing Rates Without the Risk

Fear of rejection often stops people from shopping around. Traditional “hard” credit checks leave a mark on your file, which can temporarily lower your score. Soft search technology changes the game. It allows you to see multiple real-world quotes without any impact on your financial records. This transparency is a core part of finding a low-APR deal whilst protecting your future borrowing power. It moves you from a state of uncertainty to one of total control.

Specialist Lenders for Unique Situations

Bad credit isn’t a barrier to a competitive deal in 2026. Lenders now use Open Banking to look at your current money management rather than just mistakes from years ago. If you are self-employed or looking for bad credit car finance, specialist lenders on a broker’s panel can offer rates that high-street banks simply won’t. Be honest about your outgoings during the application; this ensures the deal you secure is both the cheapest and the most sustainable for your lifestyle.

At I Need Cash, we believe in personal autonomy and individualized conditions. We streamline the entire process, connecting you to our extensive network of providers in minutes. You get the speed of a digital-first intermediary backed by a supportive, non-judgmental approach. We work on your behalf to find a solution that fits your budget perfectly. Secure your quote today and experience a risk-free journey toward your next vehicle purchase.

Drive Away with Confidence and Real Savings

You now have the tools to secure the cheapest car finance loans without the stress of traditional banking hurdles. By focusing on the total amount repayable rather than just monthly costs, you protect your long-term wealth. Remember that your recent financial behaviour and a healthy deposit are your best assets for unlocking lower interest rates. Whether you choose HP for ownership or an unsecured personal loan for flexibility, your path to a better deal is clear.

As an FCA Authorised and Regulated facilitator, we provide a safe and ethical way to explore your options. Our quick and easy online application gives you access to a wide panel of UK lenders, ensuring you find a supportive partner that values your autonomy. Take the final step toward your next vehicle with total tranquility. We are here to help you move from financial anxiety to empowerment.

Get a personalised car finance quote today with no impact on your credit score. You deserve a deal that works for your specific needs, and we are ready to assist you in finding it.

Frequently Asked Questions

What is a good APR for car finance in 2026?

A good APR in 2026 typically starts from 5.7% for loans over £25,000 or around 5.9% for amounts between £7,500 and £15,000. With the Bank of England base rate held at 3.75%, any offer below the national average of 9.6% is considered competitive. Your specific rate will depend on your credit behaviour and the total amount you intend to borrow. Smaller loans under £5,000 usually carry higher rates, often starting from 9.2% APR.

Can I get the cheapest car finance with a bad credit score?

You can still secure the cheapest car finance loans for your specific credit tier even if your financial history isn’t perfect. Modern lenders use Open Banking to assess your current affordability and spending patterns rather than just looking at old defaults. By working with a broker who has access to specialist panels, you find providers who value your current stability. This approach ensures you get the most competitive rate available for your unique circumstances.

Is it cheaper to get a personal loan or dealer finance?

It is generally cheaper to use an unsecured personal loan from a bank or broker than to choose dealer-led finance. Representative APRs for personal loans frequently start at 5.9% for mid-range amounts, whilst dealer HP or PCP deals often begin around 8.9% or higher. Using a personal loan also turns you into a cash buyer at the dealership. This gives you significantly more leverage to negotiate a lower price on the vehicle itself.

How does a larger deposit affect my car loan interest rate?

A larger deposit lowers your Loan-to-Value (LTV) ratio, which often triggers a move into a lower interest rate bracket. Lenders view a significant down payment as a sign of financial stability and reduced risk. Aiming for a deposit of 20% can help you secure the cheapest car finance loans by proving your commitment. This not only reduces your monthly instalments but also slashes the total interest you pay over the entire term.

What happens if I want to pay off my car loan early?

You have a legal right to pay off your car loan early under the Consumer Credit Act. Most lenders will apply an early settlement fee, which is typically equivalent to one or two months’ interest. Even with this fee, clearing the balance early usually saves you a significant amount in future interest charges. Always request an official “settlement figure” from your lender to see exactly how much you can save by ending the agreement ahead of schedule.

Article by

Mandy Paige

Social Content Writer and Blogger Mandy has been writing for various websites for a number of years, especially for companies in the consumer finance industry. She started her career guiding customers wanting help when applying for finance at a Loan Brokerage. Speaking to individuals wanting guidance, it led her to start writing help and guidance on finding the right solution for their needs. Outside of writing, she is a whizz with a pair of scissors as she originally trained as a hairdresser.

Disclaimer

The content of this article/blog was correct to our knowledge on the date/time it was published.