UK 25 000 Loan – Choosing the Best One

- March 13, 2026

- Remy Anderson

Estimated reading time: 13 minutes

Takeaways

- Securing a 25 000 loan represents a pivotal financial step, often tied to personal projects or debt consolidation.

- To avoid damaging your credit score when comparing offers, use tools for ‘soft searches’ rather than completing multiple formal applications.

- Understand that the ‘Representative APR’ isn’t guaranteed for all borrowers and varies based on individual credit scores.

- Choosing between unsecured and secured loans depends on risk; unsecured loans protect assets but may have stricter approval criteria above £25k.

- Calculating the true cost of a loan includes considering total interest over different terms, as longer terms can result in significantly higher overall costs.

Contents

- Soft Searches vs. Hard Checks: How to Shop for a £25k Loan Without Damaging Your Credit Score

- Why the ‘Representative APR’ Isn’t Guaranteed: Calculating Your Real Monthly Repayments

- Choosing Between Unsecured and Secured Borrowing: Protecting Your Home While Finding the Best Rates

- The ‘Hidden’ Math of 5-Year vs. 10-Year Terms: Balancing Monthly Affordability Against Total Interest

- Smart Funding: Using £25k for High-Impact Projects or Debt Consolidation

- Decoding the Small Print: Early Repayments and FCA Protections

- Your 3-Step Action Plan to Secure a £25,000 Loan Safely

- FAQ

Securing a UK 25 000 loan is a major financial milestone that often separates a long-held dream from reality. Whether you are funding a high-end kitchen renovation or looking to consolidate existing debts, this specific amount represents a critical boundary in the lending market.

For many high-street banks, a 25 000 loan serves as the effective ceiling for unsecured borrowing. In practice, this means it is typically the largest sum you can access based purely on your credit history. This is without needing to secure the debt against your home or vehicle.

Since the financial commitment is significant, verifying your lender’s safety is non-negotiable. All legitimate personal loans UK providers must be authorized by the Financial Conduct Authority (FCA). This is a status that guarantees you specific legal protections under the Consumer Credit Act. Breaking down the regulations and costs allows you to borrow with confidence.

Soft Searches vs. Hard Checks: How to Shop for a £25k Loan Without Damaging Your Credit Score

Shopping around for the best deal is smart, but formally applying to every bank you see can be dangerous. This can be due to the negative effect of loan application on credit rating. Each official application triggers a “hard search,” leaving a visible footprint on your file. They can stay there for up to 12 months. If you create too many of these footprints in a short period, it signals “credit-seeking behavior”. This can spook lenders and actually lower your score just when you need it most.

You can avoid this risk by using eligibility tools that perform a “soft search” instead. This acts like a private background check; the lender reviews your history to give you a provisional quote. This is where other banks cannot see the inquiry. Loan pre-approval and soft searches are the only way to compare real offers across the market. This is without damaging your future borrowing power.

Check the eligibility criteria for a £25k personal loan safely by following this routine:

- Audit your file: Check your own credit report first to spot and fix any errors.

- Use eligibility checkers: Stick to comparison sites that strictly use soft searches to find quotes.

- Assess the odds: Only proceed to a full application if the tool shows a high “likelihood of acceptance.”

Once you find a willing lender, you need to verify the actual cost, because the advertised “Representative APR” isn’t guaranteed for everyone.

Why the ‘Representative APR’ Isn’t Guaranteed: Calculating Your Real Monthly Repayments

Seeing a low interest rate on a comparison site often feels like a victory. However it is dangerous to assume that specific number will appear on your final contract. Under UK regulations, the “Representative APR” displayed in advertisements only needs to be offered to 51% of successful applicants.

This means that nearly half of the people approved for the exact same product could be charged a significantly higher rate, due to their credit scores. The representative APR for large bank loans acts more like a showcase price. It is not a guaranteed offer for every customer.

Change in % percentage

Small percentage shifts create massive financial differences when borrowing £25,000 over a standard five-year term. If you secure a 6% APR, your monthly bill sits around £483, costing roughly £4,000 in total interest. However, if your risk profile pushes you to a “Personalised APR” of 12%, that payment jumps to over £556.

Over the life of the loan, this shift forces you to pay an extra £4,300 merely for the privilege of borrowing. Accurately anticipating the monthly repayments on a 25000 pound loan requires waiting for this personalised offer to assess true affordability.

Volume often dictates value in the lending market. Borrowing a larger sum can sometimes unlock cheaper interest rates than requesting a smaller amount. Lenders incur fixed administrative costs for every application, so they frequently incentivize larger commitments by lowering the percentage charged. This “tiered pricing” structure means the best loan rates uk lenders offer are typically found in the £7,500 to £25,000 bracket. Before finalizing your request, it is worth checking if your specific loan amount sits on the boundary of a lower interest rate band.

If your personalised unsecured rate prove too high, you might hit a wall with standard personal loans. At this £25,000 price point, lenders become stricter with their criteria. Which prompts many borrowers to consider using their assets to reduce the lender’s risk. This naturally leads to the critical decision of whether to pledge your property as collateral to secure a loan.

Choosing Between Unsecured and Secured Borrowing: Protecting Your Home While Finding the Best Rates

For most borrowers, an “unsecured” personal loan is the gold standard because it keeps your assets safe. In this arrangement, the bank lends strictly based on your credit history and income, meaning your house is not automatically at risk if you stumble on a payment. However, £25,000 often acts as a “soft ceiling” for many unsecured loans uk providers offer.

While some high-street banks advertise limits up to £50,000, approval criteria become aggressively strict past the £25k mark. If your credit score is anything less than excellent, lenders may simply reject the application rather than offering a higher interest rate.

Hitting a wall with standard approvals often forces homeowners to consider “secured” loans. By pledging your property as collateral, you provide the lender with a safety net, often unlocking lower interest rates or acceptance despite a rocky credit history. The trade-off is severe: unlike unsecured debt, where a lender usually needs a court order to pursue assets, a secured loan gives the lender a direct legal claim on your home. This elevates the consequences of missed payments from a damaged credit score to potential repossession.

Comparing the unsecured vs secured borrowing options UK lenders provide requires looking beyond just the acceptance letter. Core differences include:

- Asset Risk: Unsecured debt protects your property; secured debt leverages it.

- Speed: Unsecured funds often arrive within 24 hours, whereas secured loans involve property valuations that can take weeks.

- Oversight: While both are offered by Financial Conduct Authority regulated lenders, secured loans often carry heavier penalties for early repayment.

Even with the right loan type selected, the actual cost of borrowing £25,000 depends heavily on the timeline you choose.

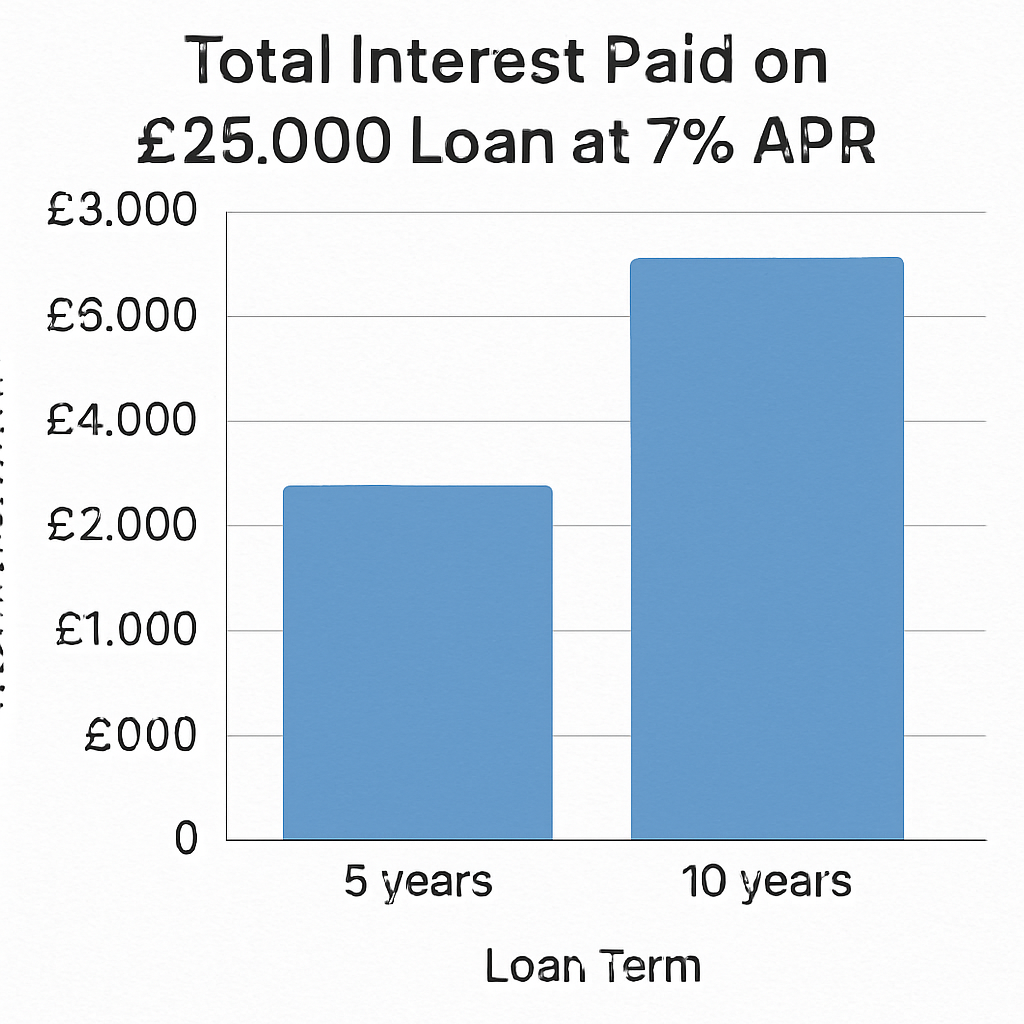

The ‘Hidden’ Math of 5-Year vs. 10-Year Terms: Balancing Monthly Affordability Against Total Interest

Focusing solely on the monthly outgoing is tempting when browsing loan offers, especially when a longer duration drops that figure significantly. Stretching a £25,000 balance over a 10 year loan might make the repayments feel manageable alongside your other bills, but this comfort often comes with a steep price tag.

Lenders earn profit for every day you hold their money, meaning a decade-long agreement doubles the amount of time interest has to accumulate compared to a standard five-year deal. While the monthly relief is real, it essentially trades your future financial freedom for current cash flow.

Calculating what is the total cost of credit reveals the true financial impact better than looking at the direct debit alone. At a 7% interest rate, borrowing £25,000 over five years costs roughly £4,700 in interest. If you extend that same loan to ten years to lower your payments, the total interest payable on high value loans skyrockets to nearly £10,000. That is an additional £5,300 paid to the bank simply for the privilege of paying slower, demonstrating why the cheapest loan on paper isn’t always the one with the lowest monthly repayment.

Finding the sweet spot requires an honest look at your budget to see how much you can repay without risking default. The best lenders for five year repayment terms often provide calculators that let you toggle the duration, helping you visualize exactly where the interest costs spike.

By committing to the shortest term you can realistically afford, you minimize the “wasted” money spent on interest and clear the debt faster. Once you have optimized the loan term to save money, the next priority is ensuring those funds are deployed effectively for your specific goals.

Smart Funding: Using £25k for High-Impact Projects or Debt Consolidation

Once the duration is set, the focus shifts to ensuring the borrowed funds actually generate value rather than just covering costs. Taking out such a significant sum should be viewed as a strategic investment; borrowing 25k for home improvement projects, for instance, works best when the renovation adds equity to your property that exceeds the interest paid. A loan this size is a tool, and its effectiveness depends entirely on how the capital is deployed against your financial goals.

Different objectives require specific “success metrics” to justify the borrowing costs:

- Strategic Consolidation: Replacing multiple credit cards charging 24% APR with a single loan at 6–8%, aiming to reduce monthly outgoings by hundreds of pounds.

- Asset Appreciation: Funding a loft conversion or modern kitchen extension where the increase in the home’s resale value outweighs the £25,000 investment.

- Operational Savings: Purchasing high-efficiency solar panels or an electric vehicle where long-term fuel and energy savings help offset the loan interest.

While consolidating debt with a twenty-five thousand pound loan is mathematically sound, it requires strict behavioral discipline to succeed. The most common trap is clearing credit card balances only to immediately run up new debt on those same cards, effectively doubling your financial burden. Do not treat this financial product like the fast cash loans advertised for quick emergencies; it is a serious, long-term contract governed by strict UK regulations. These rules are vital, particularly if you find yourself able to clear the balance ahead of schedule.

Decoding the Small Print: Early Repayments and FCA Protections

Clearing debt ahead of schedule sounds ideal, yet banks often penalize this efficiency. Since lenders profit from interest over time, cutting the loan short reduces their earnings, leading many to enforce specific early repayment charge terms and conditions.

Under UK law, this penalty is usually capped at around 58 days’ interest, ensuring you aren’t unfairly punished for financial success. Before learning how to apply for a personal loan online, you should calculate whether the exit fee outweighs the interest you would save, as the timing of your settlement significantly impacts the final cost.

Beyond exit fees, your signature activates safeguards designed to keep the playing field level. All Financial Conduct Authority regulated lenders must provide a statutory 14-day “cooling-off” period, granting you the right to withdraw from the agreement if you change your mind shortly after the funds arrive. This protection is a core component of the Consumer Credit Act, offering a safety net that unregulated lenders do not provide. These rights naturally lead into the final safety check.

Your 3-Step Action Plan to Secure a £25,000 Loan Safely

Taking out a UK 25 000 loan transforms from a daunting obligation into a strategic tool when you understand the mechanics. You have the insight to look past the marketing headlines and focus on what impacts your wallet: affordability, security, and the true price of borrowing.

Before signing any agreement, run through this final safety check to ensure the commitment fits your life:

- Check Eligibility Safely: Use a “soft search” tool to review loan eligibility criteria without harming your credit file.

- Verify the Budget: Ensure monthly payments fit comfortably within your actual disposable income, leaving room for emergencies.

- Review the Fine Print: Calculate the total cost of credit, specifically checking for arrangement fees and Early Repayment Charges (ERCs).

Securing funding is not just about approval; it is about ensuring the debt serves your goals. Not that it restricts your future. With these steps, you are ready to approach lenders not just as a borrower, but as an informed customer.

FAQ

Question: Is £25,000 really the maximum I can borrow without securing the loan?

Short answer: £25,000 is often the effective ceiling for unsecured personal loans with many UK high‑street banks, but it isn’t a hard cap. Some lenders advertise unsecured limits up to £50,000; however, approval criteria become much stricter above £25k. If your credit profile isn’t excellent, you’re more likely to be declined rather than simply offered a higher rate. If unsecured quotes are unaffordable or unavailable, some borrowers consider secured loans. However, that introduces property risk and potentially heavier penalties, so weigh that trade‑off carefully.

Question: How can I compare £25k loan offers without hurting my credit score?

Short answer: Use eligibility tools that run “soft searches.” A hard search from a full application leaves a visible mark on your file for up to 12 months. Having too many in a short time can lower your score. A soft search lets lenders assess you privately and give a provisional quote other lenders can’t see. Safe routine:

- Audit your credit file first and fix any errors.

- Use comparison sites that clearly use soft searches.

- Only proceed to a full application if you’re shown a high likelihood of acceptance.

Question: Why might my rate be higher than the advertised Representative APR, and what does that do to my payments?

Short answer: The Representative APR only has to be given to 51% of successful applicants; nearly half will pay a different, “personalised” rate based on risk. Small APR differences matter a lot at £25,000 over five years. Example: at 6% APR, payments are about £483/month with roughly £4,000 total interest. At 12% APR, payments jump to over £556/month—around £4,300 more interest over the term. Also note tiered pricing. Lenders often offer their best rates on bands like £7,500–£25,000, so the exact amount you request can influence the APR.

Question: Should I choose an unsecured or a secured loan for £25,000?

Short answer: Unsecured loans are usually preferable because your home isn’t at risk and funds can arrive quickly (often within 24 hours). But past £25k, criteria tighten. Secured loans can improve acceptance odds or lower the rate. This is by using your property as collateral, at the cost of increased risk. Missed payments can lead to repossession, and secured products often carry stricter terms (including heavier early repayment penalties). Compare not just the rate, but also asset risk, speed, and fees before deciding.

Question: Is a 10‑year term better than 5 years for a £25,000 loan?

Short answer: Longer terms cut monthly outgoings but raise the total interest dramatically. At 7% APR, five years costs roughly £4,700 in interest; stretching to ten years drives that to nearly £10,000. This equates to about £5,300 extra just for paying more slowly. Use lender calculators to test terms and pick the shortest you can realistically afford.

Question: What protections and early‑repayment rules apply to a £25k personal loan in the UK?

Short answer: FCA‑authorised lenders must follow Consumer Credit Act rules, including a 14‑day cooling‑off period to withdraw after you receive funds. If you repay early, lenders can charge an early repayment fee, typically capped at around 58 days’ interest. Check the fine print for arrangement fees and early repayment charges. Then compare those costs against the interest you’d save by settling sooner.

Related links