£500 Loan Repaid Over 3 Months

- March 9, 2026

- Remy Anderson

Estimated reading time: 13 minutes

Takeaways

- A £500 loan repaid over 3 months allows quick access to cash without draining your savings immediately.

- Fixed monthly payments offer predictability, reducing the risk of spiraling debt compared to credit cards or payday loans.

- Understanding the APR helps compare loan options, as it reflects the annual cost of borrowing and allows for fair comparisons.

- Using a loan repayment calculator ensures your budget can handle monthly payments, while checking for hidden fees is crucial before acceptance.

- Responsible repayment can build your credit if the lender reports to credit bureaus, helping secure better rates in the future.

Table of contents

- £500 Loan Repaid Over 3 Months

- The Math of a 3-Month Term: Why Fixed Monthly Payments Beat Revolving Debt

- Decoding the APR: How to Compare the True Cost of Small Loans

- Using a Loan Repayment Calculator to Predict Your Outgoings

- Turning a £500, Loan Into a Credit-Building Milestone

- Before You Apply: Essential Eligibility Criteria and Quick Approval Steps

- Is the 3-Month Instalment Loan Your Best Option? Comparing 4 Realistic Alternatives

- Your 3-Month Plan to Exit Debt Faster and Smarter

- Frequently Asked Questions

£500 Loan Repaid Over 3 Months

Unexpected expenses, like a sudden £500, mechanic’s bill, rarely wait for payday. If you want a 500 loan repaid over 3 months (for example, a £500 loan paid back in 3 months), you are trying to fill a short-term need without using all your savings straight away. This lending structure requires a large upfront payment. It turns a potential problem into a planned, short-term cost.

To understand how this loan affects you, look at your “budget surplus.” This is the money you have left after paying your important bills. To pay back this amount, you will need to set aside about £170 to £180 each month. This will depend on the lender’s rates.

You need to check if your current income can handle this withdrawal on the first of each month. Make sure that taking this amount now won’t leave you short next month.

When used wisely, these manageable repayment schedules function as a strategic tool rather than a long-term debt trap. By breaking the expense down to a daily cost, you can objectively determine if accessing emergency cash is worth the price of borrowing. Using the exact math below helps you decide if you can afford to cross this bridge safely.

The Math of a 3-Month Term: Why Fixed Monthly Payments Beat Revolving Debt

A credit card balance can stay for a long time, but a 3-month instalment loan has a set end date. When you borrow £500, the lender sets a fixed payment amount. You pay this amount every thirty days. This way, your balance will be zero by the end of the loan term.

This predictability stops the debt from getting bigger and gives you a clear date when your debt will end.

To understand where your money goes, imagine your monthly bill is split into two distinct buckets. One bucket pays back the money you borrowed, called the principal. The other bucket pays the fee for using that money.

With a fixed monthly payment personal loan, part of your income goes to paying off the £500 balance with each payment. This is not the same as minimum payment plans for credit cards. With those plans, most of your payment covers fees instead of reducing the debt.

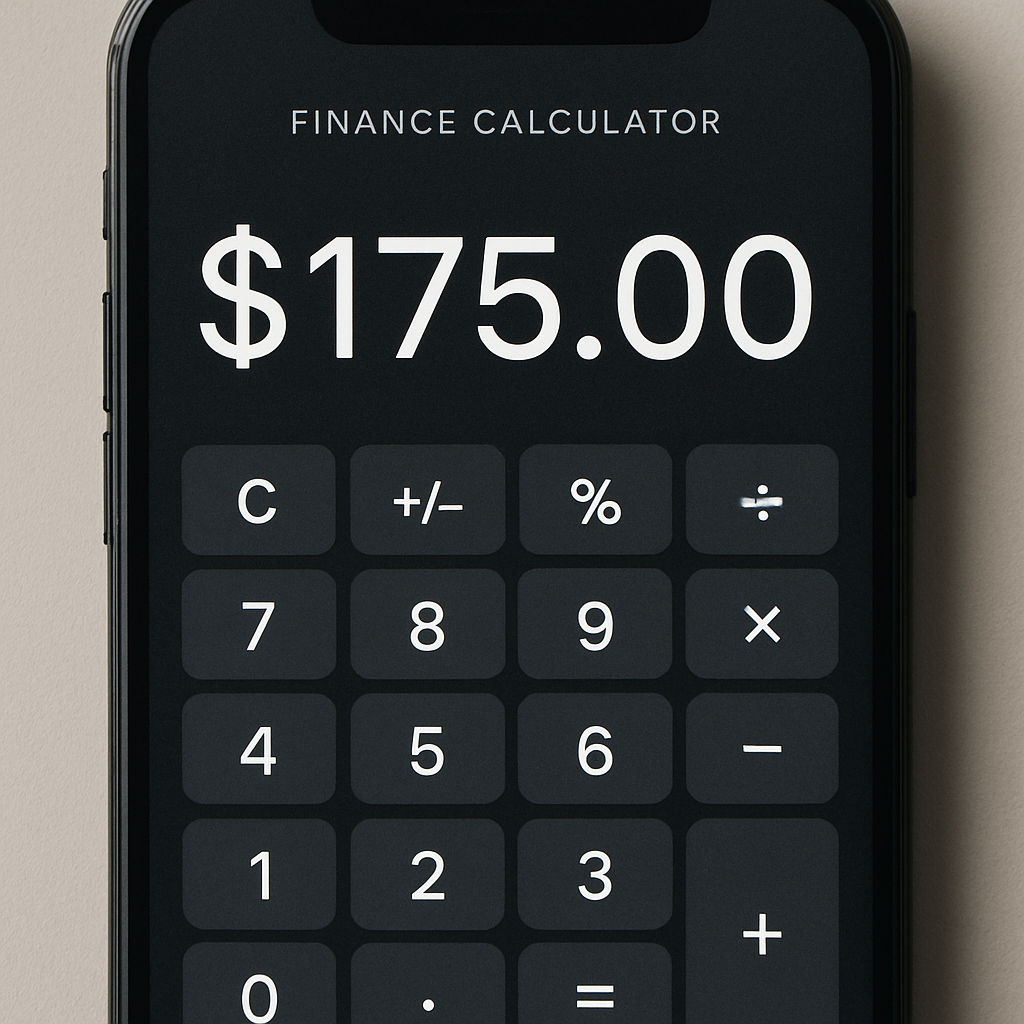

Examining the real numbers for a typical scenario reveals how this affects your wallet. If you take out a $500 loan at a 30% Annual Percentage Rate (APR) to be repaid over three months, your monthly bill would be approximately $175. While the percentage rate sounds high, the short duration keeps the total dollar amount manageable. By the time you make that third and final payment, your total interest cost for short term loans in this range would be roughly $25, meaning you paid $525 total for the convenience of the immediate cash.

This structured approach provides safety against the debt spiral often seen with open-ended borrowing. You know how much you owe and when you will be free from it. This lets you move on with your finances after ninety days.

Seeing a percentage rate like 30% can be confusing when looking at different loan options. This shows why it is important to understand APR, which is the standard cost for loans.

Decoding the APR: How to Compare the True Cost of Small Loans

When you buy groceries, you probably look at the price for each item to compare brands. APR does the same thing for loans. It works like a set price tag. It shows the annual cost of credit. This helps you compare a short-term loan with a credit card or overdraft charge fairly.

Your loan term is just three months. The APR shows what the cost would be if it were for a full year. This helps you compare different loan options fairly.

The percentage helps you compare, but the most important number for your budget is the Total Cost of Borrowing. Since you are paying back the debt quickly—in just 90 days—a higher interest rate usually means you pay less in total interest than with a long-term loan.

To see the real impact, you can run the numbers through a standard finance calculator or an online APR calculator. These tools quickly calculate loans. A £500 loan might cost you only £25 to £40 in fees, even if the interest rate seems high. Many borrowers also consult a loan apr calculator or an apr table calculator to compare quotes side by side.

Before accepting an offer, scrutinise the loan agreement for hidden costs that the headline rate might mask. When using a domestic tool or an apr calculator uk, always look for these four important details in the small print:

- The Annual Percentage Rate (APR): Confirms the annualised cost including mandatory fees.

- Total Repayment Amount: The exact dollar sum you will pay back (Principal + Interest).

- Late Fee Schedule: Specific charges added if a payment is missed.

- Prepayment Penalties: Costs associated with paying off the debt before the 3-month term ends.

With these figures confirmed, the next step is plugging them into a simulation to map out your cash flow. If you’re shopping multiple lenders, a loan comparison calculator helps you view total cost and monthly outgoings across quotes.

Using a Loan Repayment Calculator to Predict Your Outgoings

Visualising your cash flow starts by plugging your specific numbers into a loan repayment calculator. You simply need three key inputs: the loan amount (£500,), the term length (3 months), and the quoted interest rate. This tool instantly converts abstract percentages into a concrete monthly obligation, allowing you to see exactly how much money will leave your current account every thirty days rather than guessing at the math. This quick loan computation also clarifies whether the structure fits your budget.

These same tools—whether a finance calculator, finance calc, or monthly payment calculator—translate rates into a plan you can follow.

Accuracy depends on accounting for hidden variables that a basic finance calculator might miss, specifically origination fees. Some lenders deduct an administrative fee from the principal before depositing the cash, meaning you might need to request slightly more than £500, to actually walk away with the full amount you need. To correctly estimate loan repayments, you must ask the lender if the APR includes these upfront costs or if they are charged separately, as this nuance significantly alters your final total cost.

Relying on a monthly payment calculator ensures your budget can actually handle the commitment before you sign any paperwork. If the tool shows a payment of £175 but you only have $150 in disposable income, adjusting the term length now is safer than missing a payment later. The same process works whether you’re modeling a 3 500 loan, a loan for 7000, loans for 6000, a 6k loan, a 40k loan, or even a 60k loan—just change the inputs to estimate loan repayments precisely.

Turning a £500, Loan Into a Credit-Building Milestone

Successfully paying back £500, over three months proves you are reliable, but this helps your score only if the lender actually shares that data. One often overlooked detail in direct lender requirements for small cash advances is whether they report to the major bureaus (Equifax, Experian, and TransUnion). If your lender keeps your payment history private, your on-time payments remain invisible to future creditors, effectively wasting a prime opportunity to improve your financial profile.

The application process also requires strategy. Submitting multiple full applications creates “hard inquiries” that can lower your score, so prioritise lenders offering a “soft pull” pre-qualification to check rates safely. To ensure a positive impact of small loans on credit history, follow these best practices during your 3-month term:

- Enable Autopay: Automatically deduct payments on the due date to prevent accidental late fees.

- Verify Reporting: Confirm the lender sends data to at least one major credit bureau.

- Pause New Applications: Avoid applying for other credit cards or loans until this balance is cleared.

Building credit through small instalment borrowing turns a temporary cash need into a permanent financial asset. By managing this short-term debt responsibly, you position yourself for better rates on larger purchases in the future. Before you can start this process, however, you must ensure you meet the basic income and documentation standards required for approval.

Before You Apply: Essential Eligibility Criteria and Quick Approval Steps

Securing £500, quickly relies less on credit scores and more on current income stability. Most providers require you to be 18, hold a valid ID, and possess an active current account for deposits and repayment. To expedite the process, prepare a digital folder with a recent payslip and ID photo before you begin. Having these items ready ensures you meet the basic small dollar loan eligibility criteria guide without scrambling for paperwork.

You must also distinguish between direct lenders and brokers. A direct lender funds the loan themselves, offering a single point of contact, while brokers share your data with multiple third parties. For the clearest terms and reduced email spam, choose online lenders with fast approval times who handle their own funding. This direct relationship simplifies communication and often speeds up the deposit since there is no middleman.

Modern approvals often use “instant bank verification,” a secure system where you log into your bank portal to prove income instantly. If you are wondering how to apply for a quick cash advance for same-day funds, submit your request early on a weekday morning. Applications processed during business hours move faster than weekend submissions. Before committing, however, you should confirm if a 3-month loan is actually your most affordable safety net – example: £500 Loan Repaid Over 3 Months

Is the 3-Month Instalment Loan Your Best Option? Comparing 4 Realistic Alternatives

Don’t just grab the first cash offer you see; the structure of the debt matters as much as the amount. While a traditional payday loan demands the full lump sum plus fees within two weeks, a 3-month instalment loan breaks that £500, balance into manageable chunks. This difference is critical: payday lenders often trap borrowers in a cycle of re-borrowing when they can’t pay the full amount immediately, whereas a 90-day term gives you breathing room to pay down the principal gradually.

Before signing, check for alternative financing for unexpected expenses that might already be in your wallet. A standard credit card usually charges 15–25% APR, which is significantly cheaper than the triple-digit rates found on many subprime loans. However, if you lack access to traditional credit, a 3-month £500, loan is generally safer than an unauthorised overdraft, where multiple fees can snowball faster than interest charges. A quick pass with a loan comparison calculator can highlight which option aligns best with your budget.

Cost & Risk Comparison:

- Credit Card: Lowest Cost (approx. $15–$25 interest). Best if you have available limit.

- 3-Month Instalment: Moderate Cost. Fixed payments prevent surprise balloon payments.

- Bank Overdraft: High Risk. Unpredictable fees can exceed loan interest quickly.

- Payday Loan: Highest Risk. Lump-sum repayment requirement often forces rollovers.

Selecting the right financial tool depends entirely on your ability to repay on time. Comparing short term instalment loans vs payday loans reveals that the instalment option usually costs less in the long run simply because you avoid the penalties associated with missed lump-sum deadlines. Once you have selected the most affordable vehicle for your emergency, the next step is structuring your budget to clear that balance early.

Your 3-Month Plan to Exit Debt Faster and Smarter

Navigating a short-term financial gap is no longer a guessing game. By understanding the true cost of a £500, loan repaid over 3 months, you have moved from stress to strategy. You now possess the clarity to handle this commitment without disrupting your wider budget, knowing exactly when the debt will be satisfied.

Take control by running your specific interest rate through a finance calculator before signing to confirm the monthly payments match your expectations. Once the loan is active, prioritize these three payments to ensure the debt is cleared on time, verifying with the lender that the account is fully closed immediately after the final instalment. A loan apr calculator can also help you double-check that the quoted rate and fees align with your expectations.

The real opportunity arrives in month four. Instead of stopping that monthly expense, redirect the same payment amount into your own savings account. This transition builds a personal emergency fund and aids in building credit for the future, ensuring you are ready for life’s next surprise without needing to borrow.

Frequently Asked Questions

Question: How much will a £500, loan repaid over 3 months actually cost me each month and in total? Short answer: In the example given, a £500, loan at 30% APR over three months comes to roughly 175 per month, with total interest of about £25—so around £525 all-in. Depending on the lender’s exact rate and fees, you’ll likely see a monthly deduction in the £170–£180 range. Before committing, make sure your budget surplus (what’s left after essential bills) can comfortably handle that fixed payment every month for £500 Loan Repaid Over 3 Months

Question: Why does the APR look high if the total interest paid is relatively small? Short answer: APR is an annualized “price tag” for borrowing that lets you compare different credit products on equal footing. Even if the APR is 30% (or higher), the short 3‑month term limits how many dollars you actually pay—often about $25–$40 on a £500, loan, assuming typical small-loan rates and fees. Use a loan or APR calculator to translate the percentage into total repayment and monthly cost, which matter most for your budget.

Question: What fine‑print details should I confirm before accepting a 3‑month £500, loan? Short answer: Verify these essentials in the agreement:

- Annual Percentage Rate (APR): The standardized, annualized cost (including mandatory fees).

- Total Repayment Amount: Principal plus all interest/fees.

- Late Fee Schedule: Exact charges if you miss a payment.

- Prepayment Penalties: Any cost for paying off early. Also ask about origination fees. Some lenders deduct them from your payout, so you might need to borrow slightly more to net the full $500 you need.

Question: Can a small £500 Loan Repaid Over 3 Months / 3‑month loan help build my credit, and how do I make sure it does? Short answer: Yes—if your lender reports to at least one major bureau (Equifax, Experian, TransUnion). To maximize the benefit:

- Verify reporting before you accept the offer.

- Enable autopay to avoid accidental late payments.

- Use soft‑pull prequalification to check rates without a hard inquiry.

- Avoid applying for other credit until the loan is closed. On-time payments over the 90 days can become a positive tradeline, helping future borrowing.

Question: Is a 3‑month installment loan my best option compared with credit cards, overdrafts, or payday loans? Short answer: Often, yes—but it depends on what you can repay on time.

- Credit card: Usually the lowest cost (about $15–$25 interest if repaid quickly), best if you have available limit.

- 3‑month installment: Moderate cost with fixed payments and a clear end date—lower rollover risk than payday loans.

- Bank overdraft: High risk; multiple fees can add up unpredictably.

- Payday loan: Highest risk; lump‑sum repayment often triggers costly rollovers. Choose the option that fits your budget and timeline; fixed installments generally provide safer, more predictable payoff than lump-sum payday structures.

Related links